That vulnerability is exactly what gives Oil its new safe-haven status.

The threat is no longer theoretical. A prolonged disruption through the Strait of Hormuz would trigger a shock the market is still failing to fully price. Yet the physical interruption is only the beginning. The real escalation begins when governments and institutions start hoarding supply at the same time.

“This is where the market is still underestimating the scale of the problem,” Hansen says. “The physical disruption is the trigger, but precautionary hoarding is the multiplier. Once nations start securing supply simultaneously, price escalation becomes far more aggressive than most forecasts imply.”

Protectionism Could Make Everything Worse

One of the greatest risks during any energy crisis is not just war, but policy error. Governments often try to shield domestic consumers through price freezes, fuel controls and export restrictions. In practice, these measures usually worsen the global shortage. Price caps discourage production and encourage consumption. Export bans tighten international markets even further.

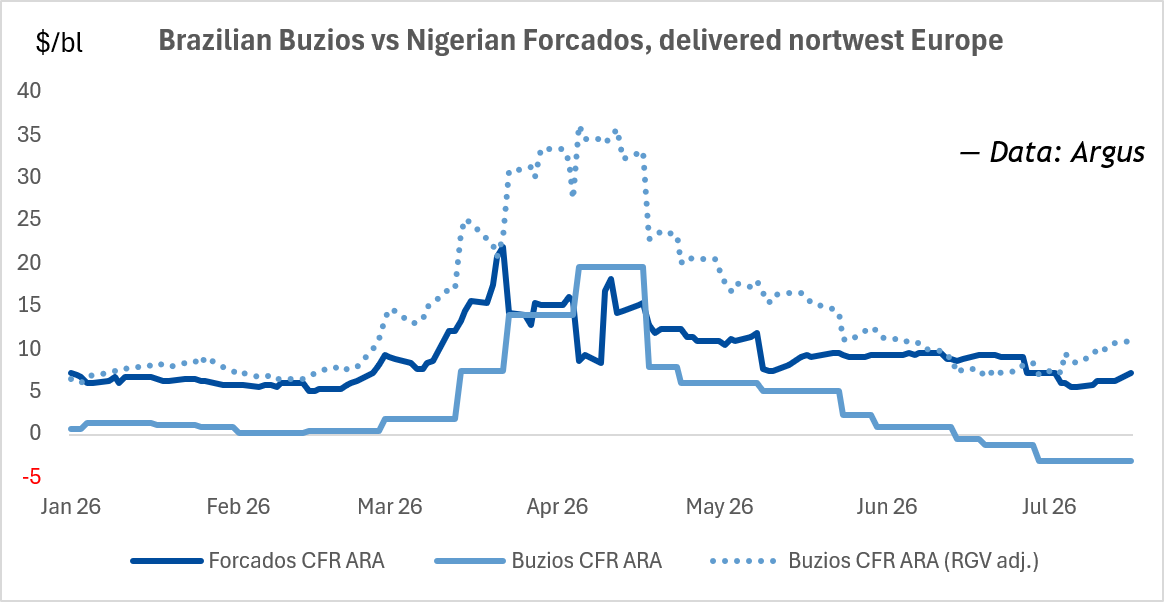

That process is already unfolding. Russia is banning Gasoline exports from April 1, pulling roughly 117,000 barrels per day out of global circulation just as supply stress intensifies. China has also moved to restrict fuel exports, including jet fuel, in a bid to protect domestic demand.

The result has been immediate dislocation across Asia-Pacific energy markets, with jet fuel premiums surging and shortages beginning to affect airline activity. When large economies begin hoarding energy, shortages do not ease. They accelerate.

The Energy Supercycle Is No Longer Theoretical

There is a deeper structural force beneath the headlines. The world is dismantling the old hydrocarbon system before the new one is ready to fully carry the load. AI-driven electricity demand, military requirements, industrial resilience and baseload power needs are all reinforcing the central role of fossil fuels. Meanwhile, energy remains chronically under-owned in global portfolios.

“Oil is under-owned, undervalued and still widely underestimated,” says Hansen. “That is exactly the kind of setup that creates asymmetric upside. In an Energy Supercycle, constrained supply and inelastic demand do not produce polite moves. They produce violent repricing.”

Goldman Sachs now outlines scenarios that see Oil spiking to $120, $140 and even $160 depending on the duration and severity of disruption. Hansen’s view is even more direct: “If disruption persists, $150 is not the ceiling. It is the next milestone.”

The Smart Money Has Already Moved

Over the past 15 years, The Gold & Silver Club has earned a reputation as one of the most accurate forecasters in the Commodities space – earning the firm recognition as a trusted authority among institutional investors and private wealth clients alike.

At the start of the year, The Gold & Silver Club declared 2026 “The Year of Hard Assets.” Three months in, that call is beginning to look less like a bold thesis and more like the defining macro reality of the year.

“The market still thinks Energy is a side story,” Hansen says. “It is not. It is the main story of 2026 and Oil may prove to be the safest place to be when the next global shock hits.”

That repricing is not coming at some distant point in the future. It is happening now.

For investors and traders alike, the message is clear: if you wait for full consensus, you will be paying a far higher price for the same thesis. The smart money is already rotating. The only question is whether you move before the crowd – or after it.