© Andrei Stanescu / Getty Images

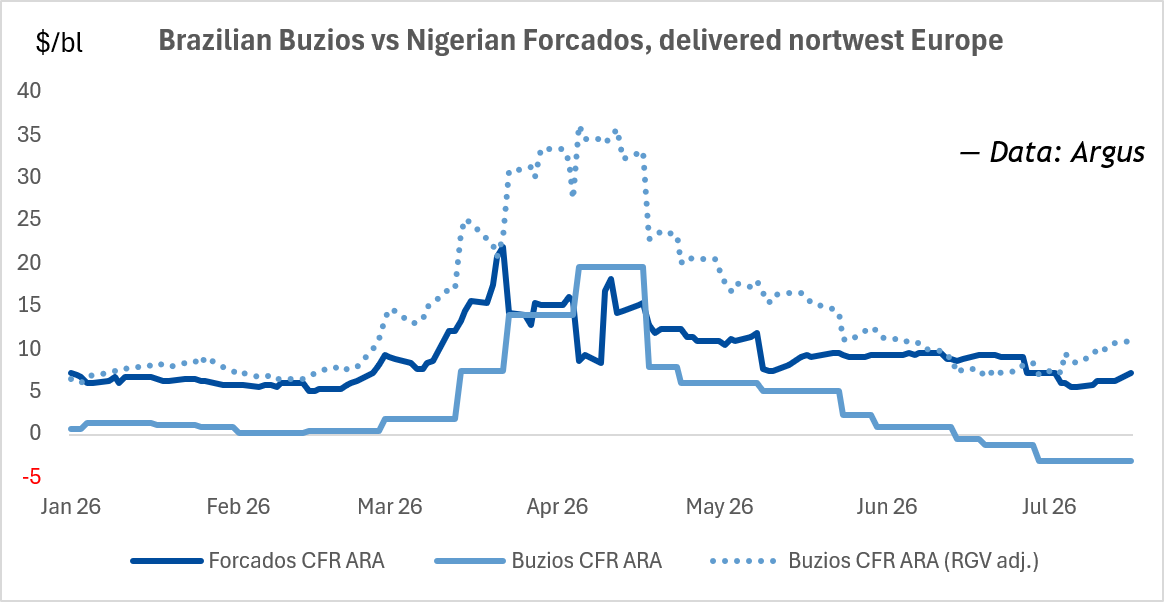

Barclays just turned more constructive on the AI data center power story. Analyst Christine Cho raised her price target on Bloom Energy (NYSE:BE) to $254 from $177, while maintaining an Equal Weight rating. The price target raise reflects a firm that clearly believes the fundamentals have stepped up, even if valuation keeps it from a full bullish call.

The move follows a blowout Q1 2026 report and a meaningful guidance raise that has reframed the multi-year revenue trajectory for Bloom Energy. Bloom Energy stock has been a marquee AI infrastructure name in 2026, and the Barclays revision codifies what the market has already been pricing in.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| BE | Bloom Energy | Barclays | Price target raised | Equal Weight | Equal Weight | $177 | $254 |

The Analyst’s Case

Cho lifted her Bloom Energy estimates to capture the sales and margin beat for the quarter, the guidance raise for 2026, and management commentary about the longer-term outlook. That last point is the most telling: when analysts flag long-term framing, it usually means Bloom Energy has repositioned its multi-year story.

The Q1 2026 numbers gave Barclays plenty to work with. Bloom Energy posted non-GAAP EPS of $0.44 versus $0.1285 consensus and revenue of $751.05M, with product revenue up 208% year over year. FY2026 guidance was lifted to $3.4B–$3.8B in revenue, implying roughly 80% growth at the midpoint.

Company Snapshot

Bloom Energy makes solid oxide fuel cell Energy Servers that generate electricity on-site from natural gas, hydrogen, or biogas. That behind-the-meter capability matters for AI hyperscalers facing multi-year grid interconnection queues, a dynamic CEO KR Sridhar describes as “bring-your-own-power” becoming a business necessity.

The customer momentum is concrete. Bloom Energy has a $5 billion AI infrastructure partnership with Brookfield Asset Management, an Oracle collaboration to power AI data centers, and a $20B total backlog exiting Q4 2025.

Why the Move Matters Now

Bloom Energy stock trades at around $273 after a 214% year-to-date rally and a 1,342% one-year gain. The valuation is rich, with a forward P/E ratio of 128x and price-to-sales ratio of 33x.

That backdrop explains the Equal Weight stance. Barclays is acknowledging fundamental momentum, yet the new $254 target sits below the recent market price, signaling caution on multiple expansion after the move.

What It Means for Your Portfolio

The bull case is straightforward: AI capex remains relentless, hyperscalers need on-site megawatts now, and Bloom Energy’s product backlog and capacity doubling to 2GW by end of 2026 point to durable growth. Each new hyperscaler deal could add gigawatts of long-duration revenue visibility.

The bear case for Bloom Energy centers on execution and valuation. Manufacturing ramp risk, financing dependency, tax-credit reliance, and any cooling in AI capex sentiment could pressure the multiple quickly given the rally. A recent director insider sale of 25,000 shares at a weighted average of $266.96 is worth noting, though not necessarily a signal.

For prudent investors, the Barclays revision reinforces that Bloom Energy is a real beneficiary of the AI power wave. Position sizing and entry discipline matter most when a stock has already run this far, this fast.