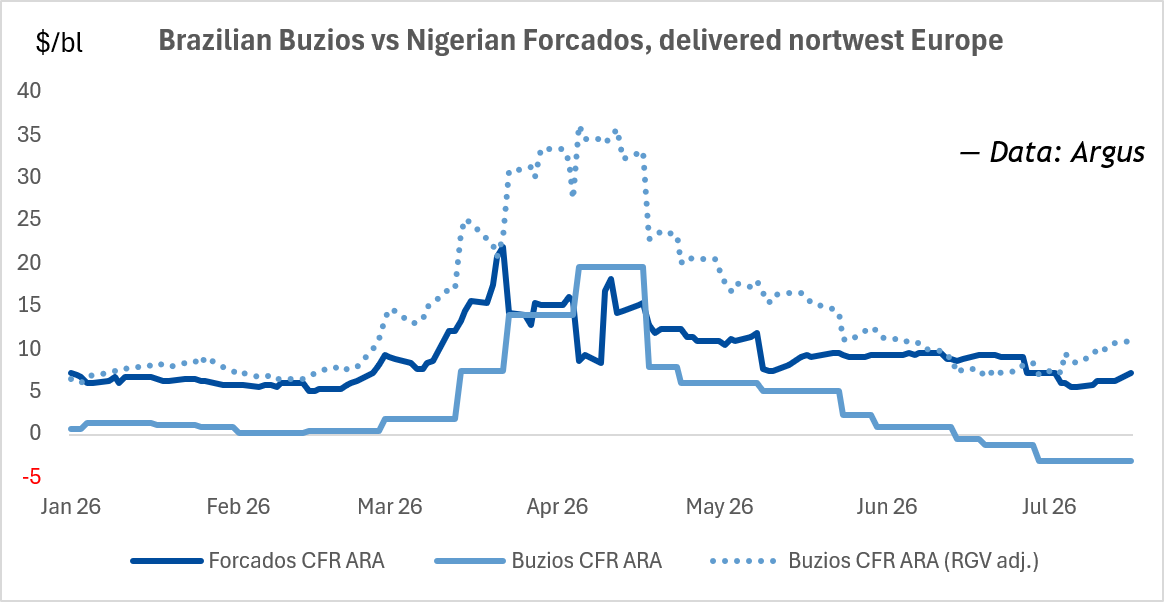

Henry Hub natural gas closed last week at $2.67 per million BTU, a glut-level reading even with the world’s largest LNG exporter still partially offline. That disconnect is exactly why ProShares Ultra Bloomberg Natural Gas (NYSEARCA:BOIL) has bled out this year. BOIL is now trading around $13, down 43% year to date and 80% over the past year. The bull case for BOIL right now is essentially a calendar trade. You are betting that what Qatar took out of global supply in early 2026 will matter again the moment heating season starts.

What the fund actually does

BOIL targets 2x the daily return of the Bloomberg Natural Gas Subindex, which tracks front-month Henry Hub futures. It does not hold physical gas, it does not hold producer equities, and it does not pay a dividend. It rolls futures contracts and resets its leverage every single day. So your return engine is short-term moves in U.S. domestic gas prices, amplified, then compounded back to zero by the math of daily resets.

The catalyst people are circling is the Qatari shortfall. U.S. shale and LNG export capacity are expanding aggressively, which is suppressing domestic Henry Hub prices right now even with a major global supplier dark. But LNG is the transmission mechanism. Every cargo American terminals send to Europe and Asia to backfill Qatar is a cargo that does not stay home, and that pressure tends to show up in winter strip pricing rather than May shoulder-season spot.

Does the setup hold up

The winter just past is the proof of concept. Henry Hub spiked to roughly $31 in late January, the highest level in years, before collapsing back to about $3 by mid-March. BOIL rode that wave hard. One trade publication reported the ETF jumped 65% in a single week during the January cold snap, with Henry Hub front-month contracts posting a 125% rise over four sessions.

So the mechanics work when the underlying moves. The problem is what happens between catalysts. May 2026 spot prices are running below where they were a year ago, despite Qatar still being offline. Shoulder season is brutal for a leveraged long futures product, and BOIL’s five-year decline of more than 99% is the receipt.

The tradeoffs you are actually accepting

- Volatility decay is not theoretical. A Seeking Alpha analysis put BOIL’s annualized return at negative 41% over 10 years, driven by daily leverage resets and roll costs. Hold it through a choppy summer and you can be right on direction and still lose money.

- Contango eats the carry. When winter futures trade above front-month, every monthly roll sells low and buys high. US News documented that BOIL and UNG significantly underperformed the underlying commodity in 2023 due to contango.

- Timing risk is the whole game. Buy too early and decay bleeds you before the catalyst arrives. Buy after the first cold-front headline and you are paying the spike, not catching it.

Who this is for

BOIL is a tactical instrument for traders who want a defined-window bet on a colder-than-normal winter combined with the Qatari supply gap persisting into Q4. A position sized at 1% to 3% of a portfolio, entered in tranches through late summer, and held with a hard exit plan makes sense as an asymmetric bet. Anyone treating BOIL as a multi-year energy holding is fighting the prospectus. The producer equities, or a non-levered fund like UNG, do that job without the daily reset tax.