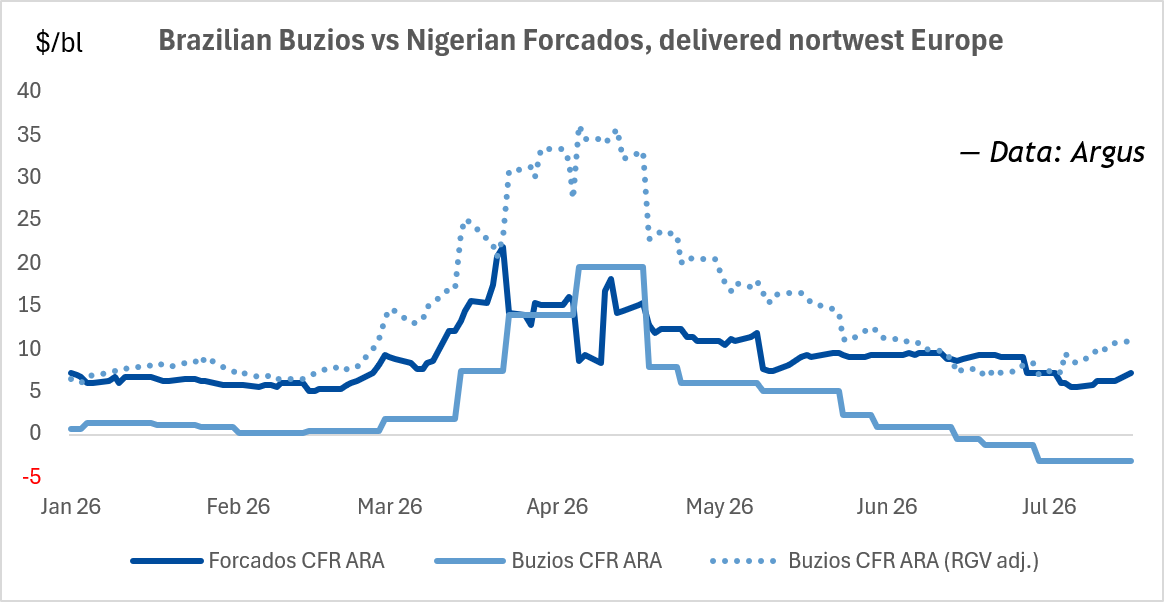

If the bullish tone continues over the weekend, traders should easily overcome last month’s high at $4.881, setting up a test of the long-term retracement zone at $4.953 to $5.198. Hedge sellers are likely to re-emerge on a test of this area, so it will be up to the speculators to continue to drive prices beyond this resistance.

On the downside, short-term support is the retracement zone at $4.397 to $4.283.

Are Shrinking Storage Levels Signaling a Tighter Winter Market?

The EIA reported an 11 Bcf withdrawal for the week ending November 21, marking the second consecutive weekly draw. Storage now stands at 3,935 Bcf—32 Bcf below last year but still 160 Bcf above the five-year average. While inventories remain healthy overall, the pace of draws is picking up. The East and Midwest regions led this week’s pull, while the South Central saw an unusual 13 Bcf injection, underscoring how regional weather and demand are starting to drive divergence in balances.

How Much More Can LNG Demand Grow From Here?

LNG exports remain the central demand driver. November shipments hit a record 10.7 million tons, a 40% increase year-over-year. Feedgas deliveries averaged 17.8 Bcf/d, up from October’s 16.7 Bcf/d record. Additional upside remains as Venture Global’s Plaquemines terminal and Cheniere’s Corpus Christi plant continue to ramp up. With international pricing still supportive, LNG demand is becoming less seasonal and more embedded, lifting baseline U.S. gas demand.

Is Winter Weather Finally Delivering on Heating Demand?

A deepening cold pattern across the central and eastern U.S. is providing the first real boost to residential and commercial heating demand. The National Weather Service is reporting widespread below-normal temperatures, with highs in the teens across the northern tier and multiple storm systems expected through the week. This active setup is precisely the kind of weather that starts drawing down inventories more aggressively in early winter.

Can Record Production Keep Pace With Demand Growth?

Output in the Lower 48 remains strong, averaging 109.3 Bcf/d in November—higher than October’s 107.0 Bcf/d and surpassing the prior monthly record. Efficiency gains in key basins are sustaining elevated production levels despite lower rig counts, but that supply strength is being increasingly offset by demand-side pressure from both LNG and heating load.