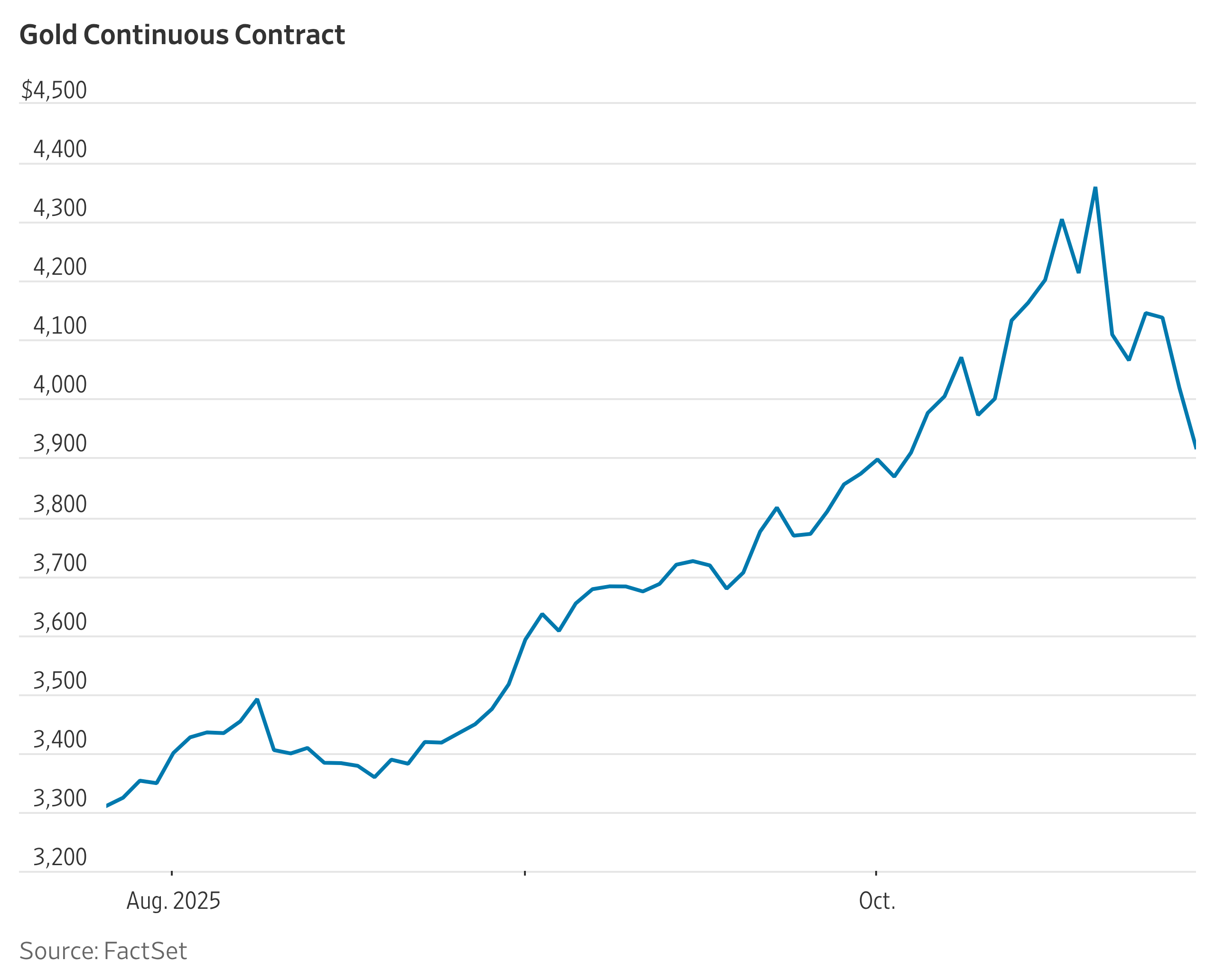

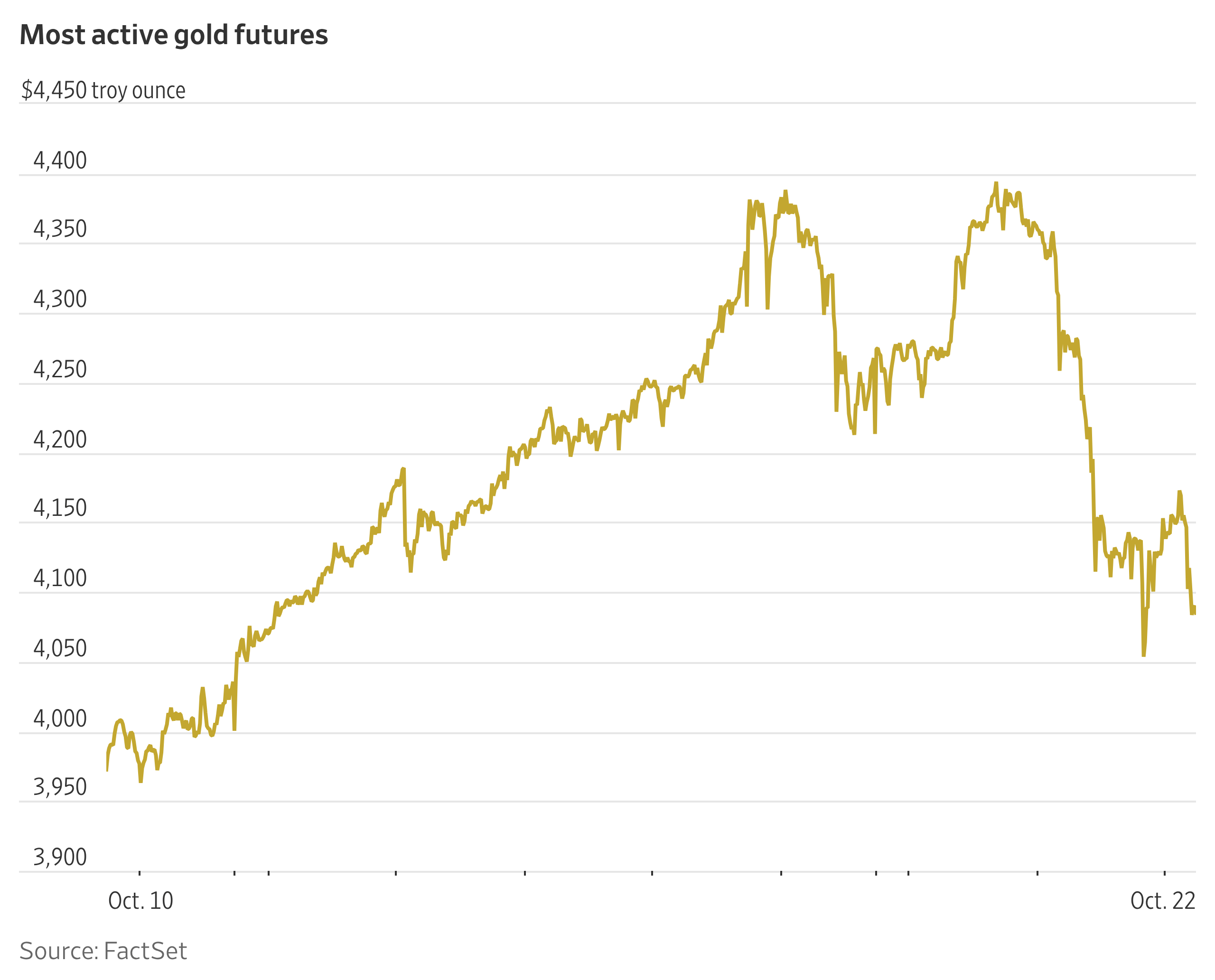

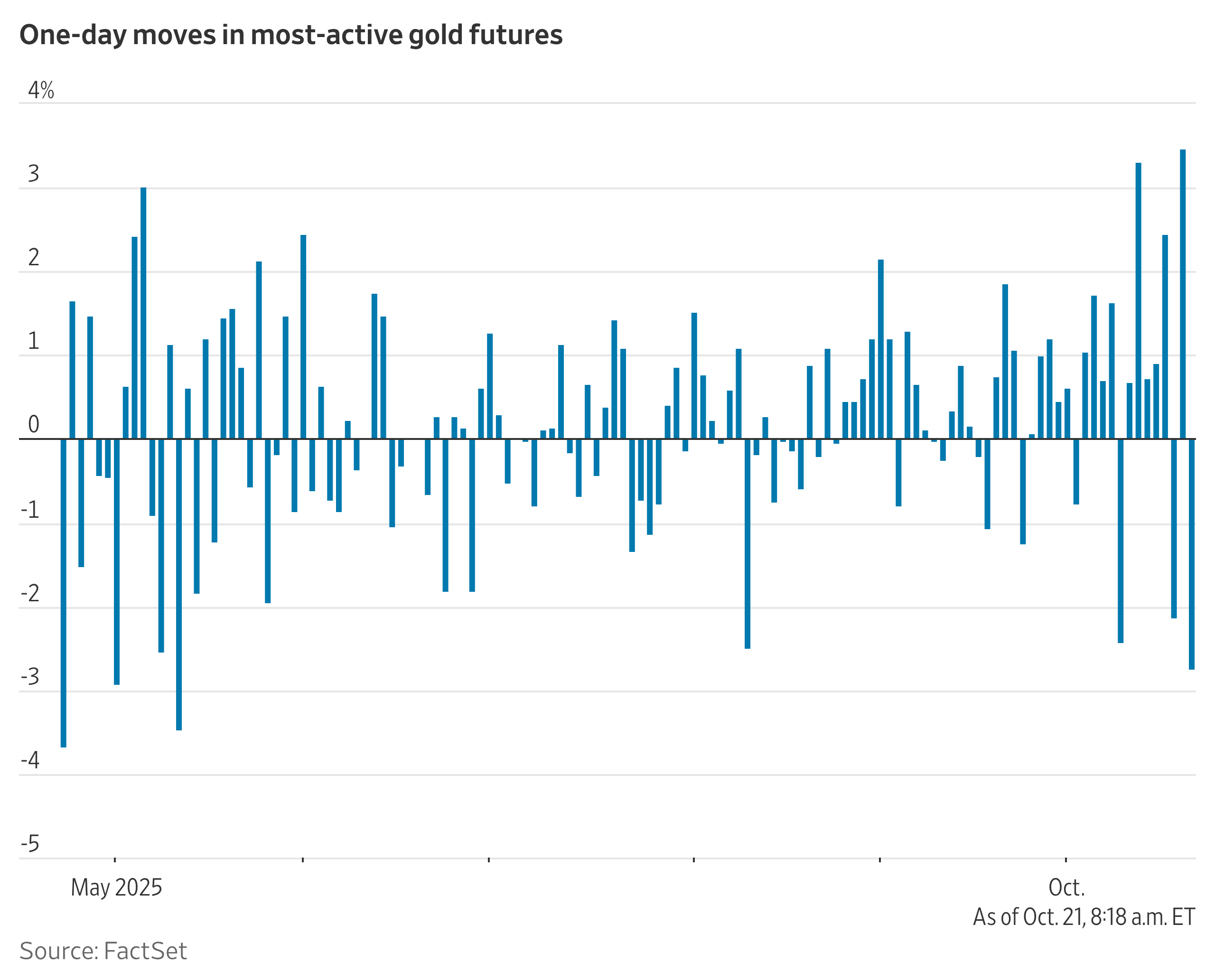

Gold prices are currently under pressure, down 4% year-to-date after delivering a remarkable 65% return in 2025. However, despite this near-term weakness, sentiment within the central banking community remains decidedly upbeat. Expectations point to continued gold buying over the next 12 months, reflecting sustained confidence in gold’s strategic role amid evolving geopolitical and macroeconomic dynamics.

Why Is Gold Under Pressure Right Now?

The geopolitical and economic landscape poses significant challenges, and gold prices are unlikely to rebound in the near future without substantial changes in fundamental factors.

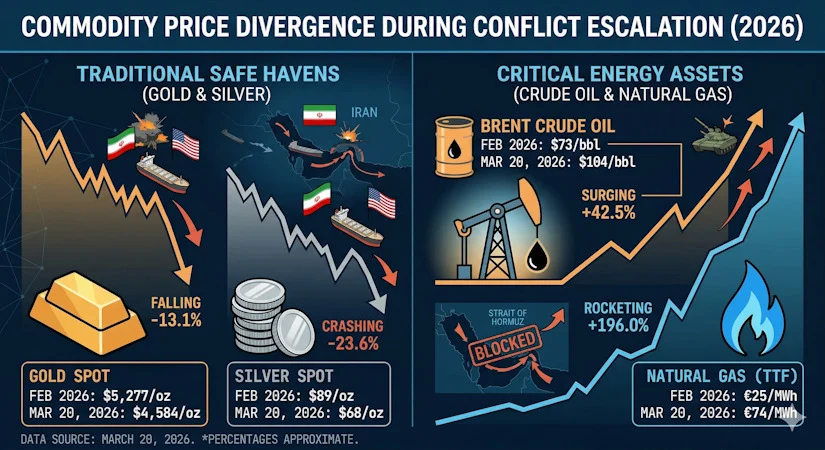

Major challenges ahead include the Iran war pushing oil prices up, a strong dollar, and an inflationary environment — all of which are likely to prompt the US Fed to maintain higher interest rates. Unless the dollar weakens and a Fed rate cut occurs, gold prices are expected to remain under pressure.

There is, however, a potential silver lining. The US-Iran agreement on reopening the Strait of Hormuz marks a significant step towards resolving the Iran war conflict — though the outcome remains uncertain.

But Central Banks Are Not Worried

Despite these near-term headwinds, central banks are not losing confidence in gold’s long-term future. According to the World Gold Council Central Bank Gold Reserves Survey 2026, central banks remain very positive on gold, highlighting its significance amid a volatile geopolitical and economic environment.

With the majority of responses coming in after the start of the Middle East conflict, this year’s survey offers a particularly timely window into how central bankers view gold amid ongoing geopolitical turmoil.

The numbers reflect this confidence clearly: 84% of central banks believe that gold will hold a moderately or significantly higher share of total reserves five years from now — up from 76% last year. 89% of central banks believe that official gold reserves will continue to increase.

However, it is worth noting that not everyone shares this conviction. 11% of central banks believe that gold’s proportion of total reserves would remain unchanged — up from 5% last year.

Responses were fairly consistent across advanced economies, emerging markets, and developing economies (EMDE), with the majority in both groups anticipating that the proportion of total reserves held in gold would be moderately higher in five years.

What Are Central Banks Doing With Their Own Holdings?

Most respondents did not expect their gold reserves to change significantly in the next 12 months. 45% of respondents thought that their own institution’s gold reserves would rise over the next year — broadly in line with last year’s finding of 43%. This marks a new record high in the proportion of central banks expecting to add gold to their own reserves, with EMDE banks continuing to lead their advanced economy counterparts.

Among EMDE respondents, around half thought that their own gold reserves would increase in the next 12 months, while the other half anticipated they would remain unchanged.

Why Do Central Banks Hold Gold?

The survey also dug into the reasoning behind central banks’ continued faith in gold. When asked about relevant factors in their decision to hold gold, 90% of central banks indicated that gold’s performance during times of crisis is highly relevant.

84% of respondents indicated that gold’s role as a store of value was a relevant factor, while 83% pointed to gold’s attribute as a portfolio diversifier. These responses reinforce gold’s appeal as a strategic reserve asset — one that goes well beyond short-term price movements.

How Much Gold Are Central Banks Buying?

The numbers behind this conviction are striking. Central banks have accumulated an average of 1,000 tonnes of gold each year over the past four years — up significantly from the average of 500 tonnes over the preceding decade. That is a doubling of the pace of buying, underscoring just how seriously central banks are treating gold as a strategic asset.

Global central banks have increased their gold holdings, surpassing US Treasuries for the first time since 1996. Gold now represents 20% of foreign exchange reserves, making it the second most significant asset after the USD (46%), and ahead of the euro (16%).

Dedollarization Effect

Interestingly, central banks were far less optimistic about the US dollar. Even though the dollar maintains its position as the dominant global reserve currency, data from the IMF’s Currency Composition of Official Foreign Exchange Reserves shows that its share has been on a gradual decline. And most central banks believe this trend will continue, with 74% expecting the dollar’s share to be lower five years from now.

Disclaimer: This article is for general informational purposes only and does not constitute investment, financial, or trading advice. Gold prices are subject to significant market volatility driven by geopolitical and macroeconomic factors. Past performance is not indicative of future returns. Readers are strongly advised to consult a SEBI-registered investment advisor or qualified financial professional before making any gold-related investment decisions.