Precious metals stocks took a beating last week as hopes of a resolution to the Iran war and the reopening of the Strait of Hormuz receded once again – repeating a pattern witnessed numerous times over the last six weeks.

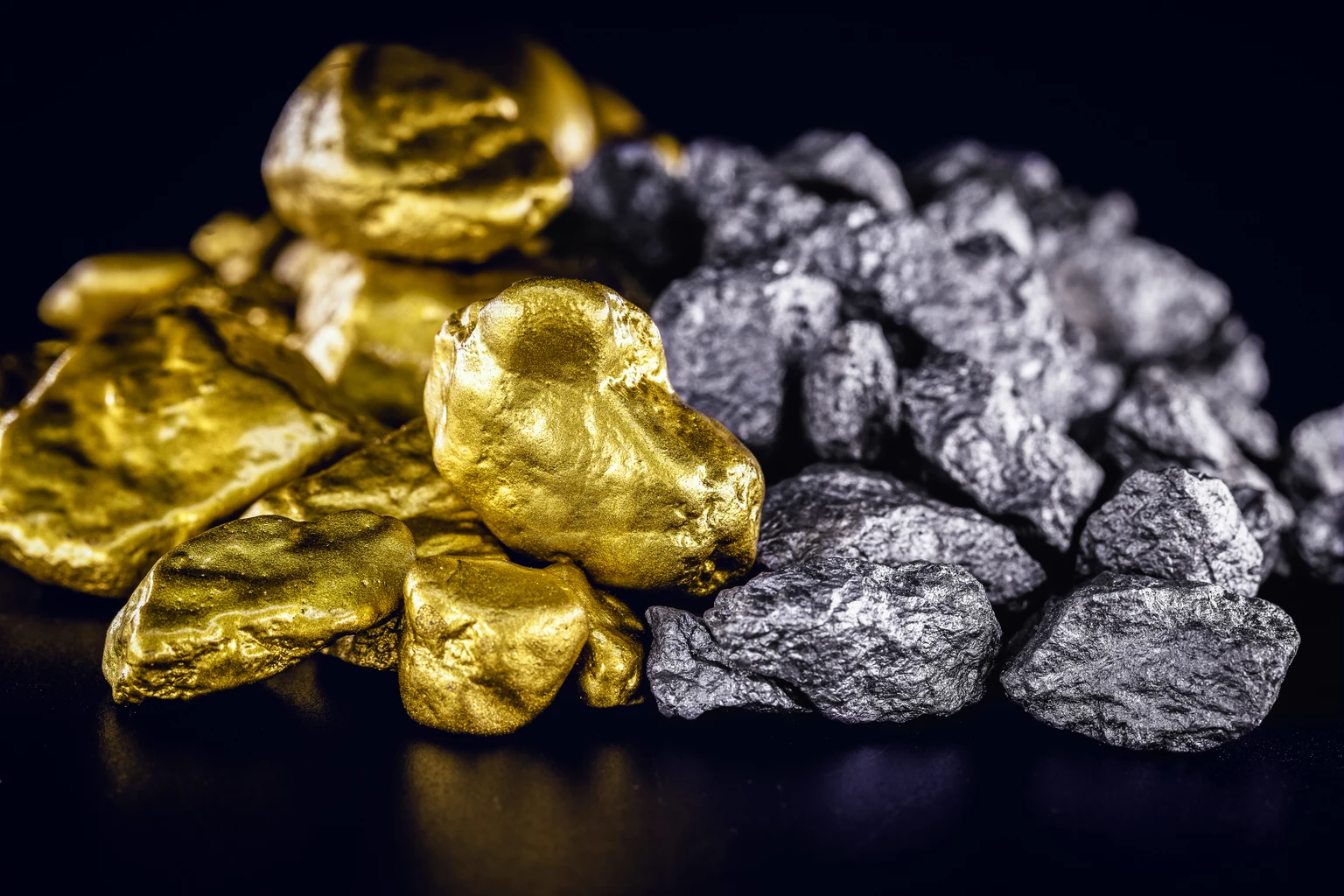

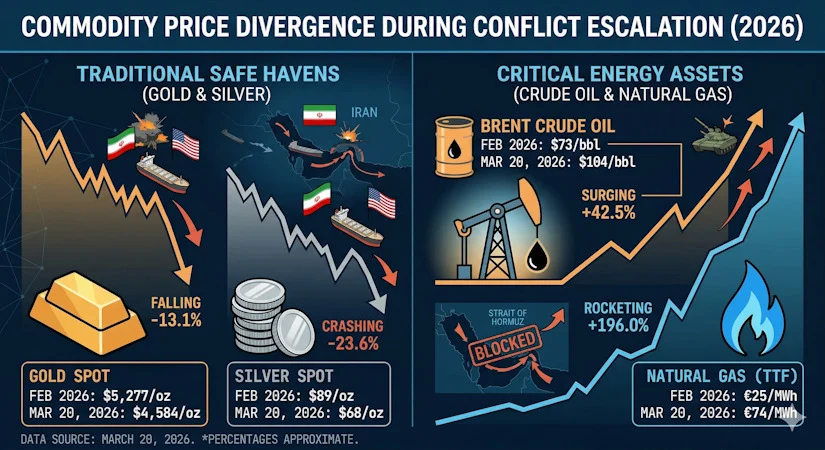

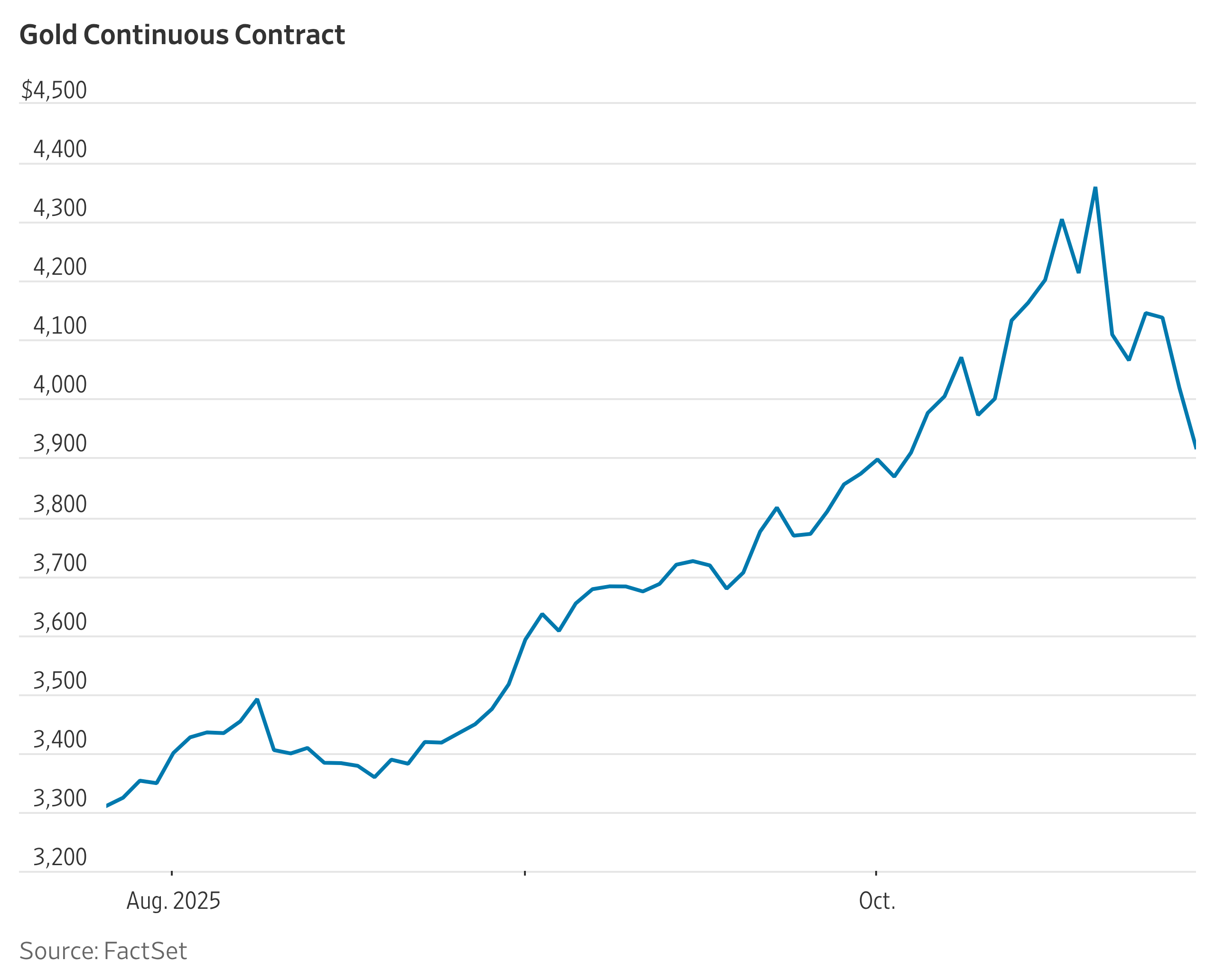

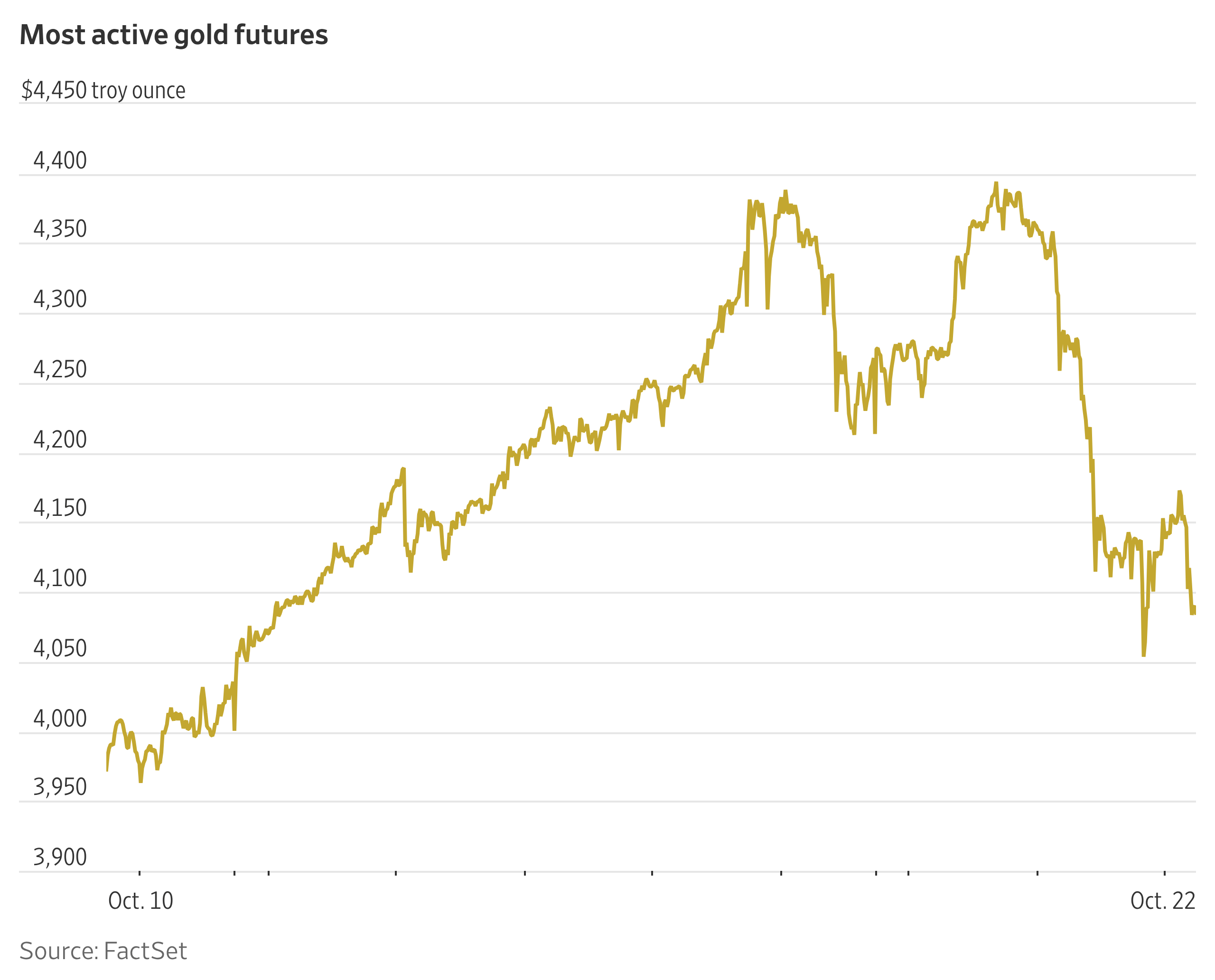

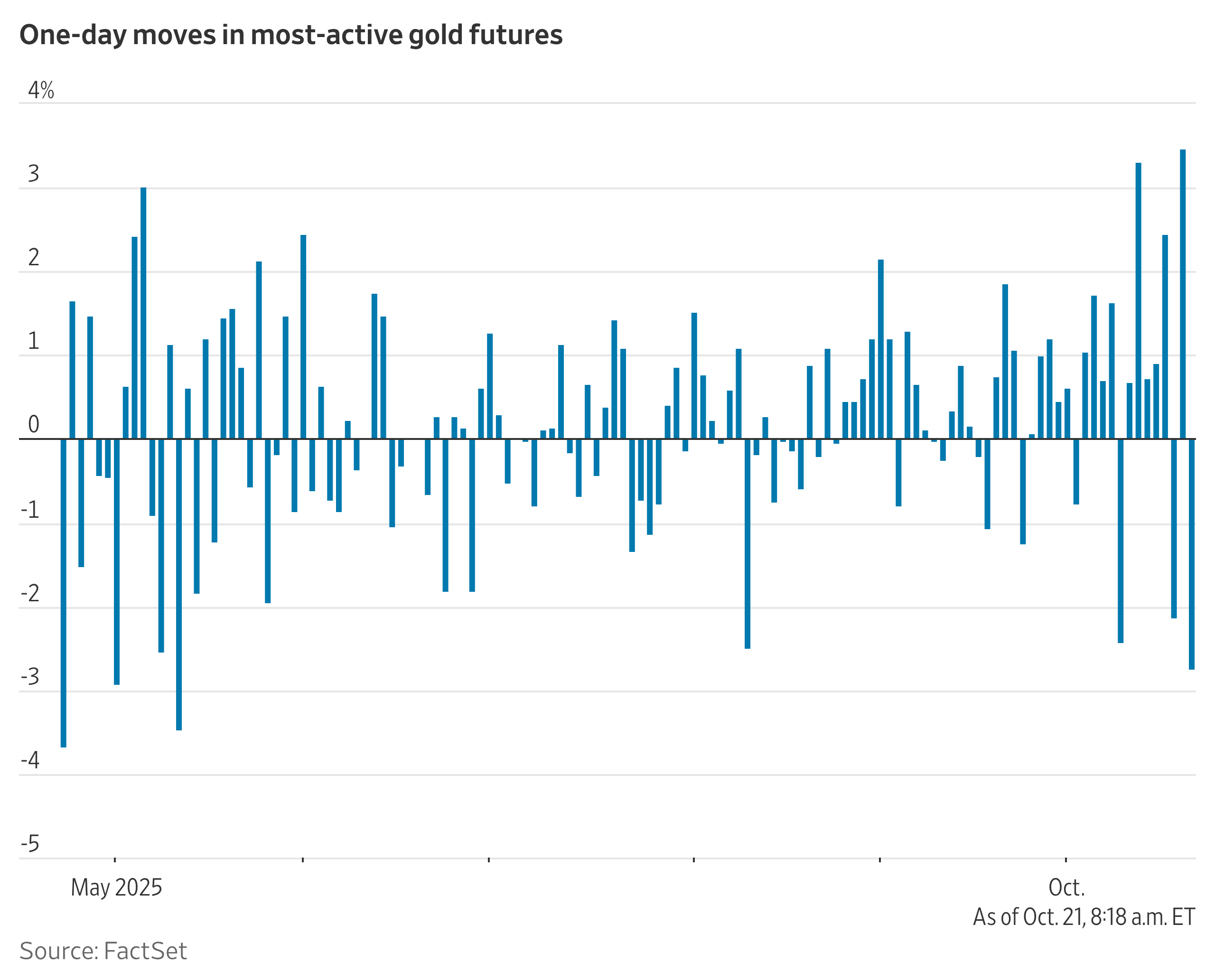

The FTSE/JSE Resource 10 index ended the week nearly 7% down, dragged lower by weaker lower precious metals prices. Spot gold traded at $4 540 an ounce (oz) on Friday, down more than 4% for the week. Platinum prices receded 3.5% last week, with palladium losing nearly 7%.

The big losers on the JSE last week were Impala Platinum, Valterra Platinum (formerly Anglo Platinum), Gold Fields, Sibanye Stillwater and Harmony Gold – all falling between 6% and 12%.

Source: Moneyweb

Peace hopes were dashed last week in the on-again off-again war in Iran, which has choked traffic through the Strait of Hormuz and driven Brent crude oil prices to just under $110 a barrel (as of Sunday night).

The US and Iran appear to be testing who can outlast the other in this high-stakes gamble that has seen the oil price nearly double since January.

Inflation risk

Macro strategist and Novaque CEO Shiven Moodley tells Moneyweb that war escalation and geopolitical risk would normally be bullish for safe-haven assets such as gold.

“However, the current market reaction suggests that inflation risk is overpowering the haven bid.

“Higher energy prices raise the risk of stickier inflation, which keeps bond yields firm and delays the case for easier monetary policy. That is negative for non-yielding assets such as gold and silver, particularly when real yields and the US dollar are moving higher.”

ADVERTISEMENT

CONTINUE READING BELOW

Read: Gold heads for weekly drop as inflation fuels rate-hike bets

Amy Gower, metals and mining commodity strategist at Morgan Stanley Research, says the Iran conflict has triggered an energy supply shock that has reduced hopes for lower US interest rates.

“It is not surprising that gold has struggled to work as a safe haven this time … Gold’s sensitivity to monetary policy has taken over as the key price driver. This has overshadowed its safe-haven status.”

Hopes for a quick end to the war appear to be vanishing, pushing medium-term inflationary fears to the fore of every central bank across the world.

That inflationary pressure is now weighing on the gold price, adds Peter Grant of Zaner Metals.

Silver, platinum and palladium are more closely linked to industrial demand, which remains vulnerable if higher energy prices weaken global growth expectations.

“What stands out is the positioning risk,” says Moodley.

“When a crowded long metals trade meets rising yields and a stronger dollar, the unwind can be more aggressive than normal. This is less about the market dismissing geopolitical risk and more about the rates channel dominating the safe-haven channel.”

US rate cut doubts

Also disappointing was the outcome of the meeting last week between US President Donald Trump and Xi Jinping of China. While it signalled strategic stability between the two superpowers, it did not yield the hoped-for reset in trade and economic growth.

ADVERTISEMENT:

CONTINUE READING BELOW

That leaves several questions unresolved, particularly as major investment banks remain divided on whether the US will cut rates in 2026.

These market dips have been perceived as buying opportunities, but concerns are mounting that precious metals may be facing a deeper drawdown.

Read: Winners and losers from Trump and Xi’s two-day Beijing summit

Analysts Razan Hilal and Fawad Razaqzada of Forex.com warn of bearish momentum now gathering steam as gold, silver and other commodities retreat in the face of hotter US inflation data, which has bounced from 2.4% year-on-year to 3.8% since the start of the Iran conflict.

Kea Nonyana, market analyst at PrimeXBT, comments: “The Iran driven energy shock is causing persistent inflation and preventing Fed rate cuts, making non-interest paying precious metals vulnerable.

“This classic safe haven is acting like a risky asset as investors sell off holdings for the US dollar. This suggests a continued downtrend, not a buying opportunity.”

Read/listen:

Moodley believes equity markets will continue to treat geopolitical drawdowns as corrections rather than the beginning of a broader bear market.

“One reason is that AI-related demand for compute, power, metals, infrastructure, and semiconductors continues to act as a transmission mechanism for capital expenditure and earnings resilience.

“As long as that structural demand remains intact, markets may be more willing to absorb geopolitical shocks without fully repricing into a recessionary bear-market regime.”