There is nothing good about the energy price shock that Donald Trump’s military action has launched at Europe’s economy. For oil and gas-importing countries, it raises the cost of essential goods, leaving less for everything else. Governments are left with the difficult task of distributing the losses as best they can.

So when UK chancellor Rachel Reeves gave her Mais lecture yesterday, promising higher growth via stability, investment and reform, the conflict in the Gulf undermined all prongs of her strategy. The war hits the stability crucial for private investment and for realising the benefits of reform. The longer the war lasts, the more the economic outlook for Europe and the UK will deteriorate. That is obvious.

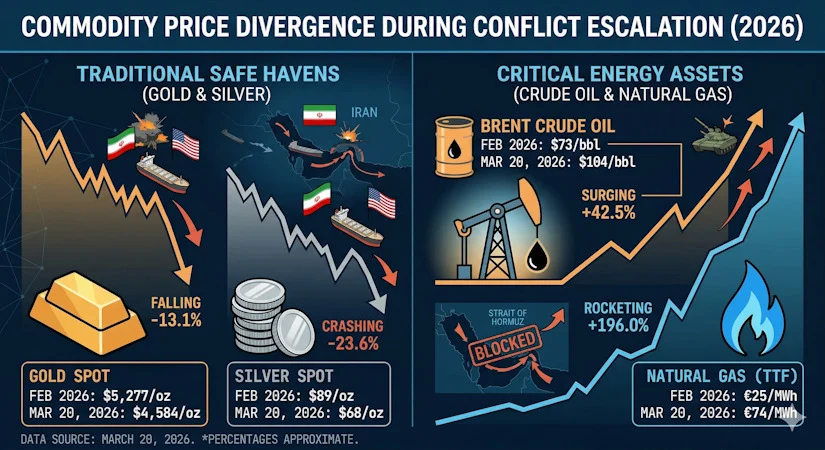

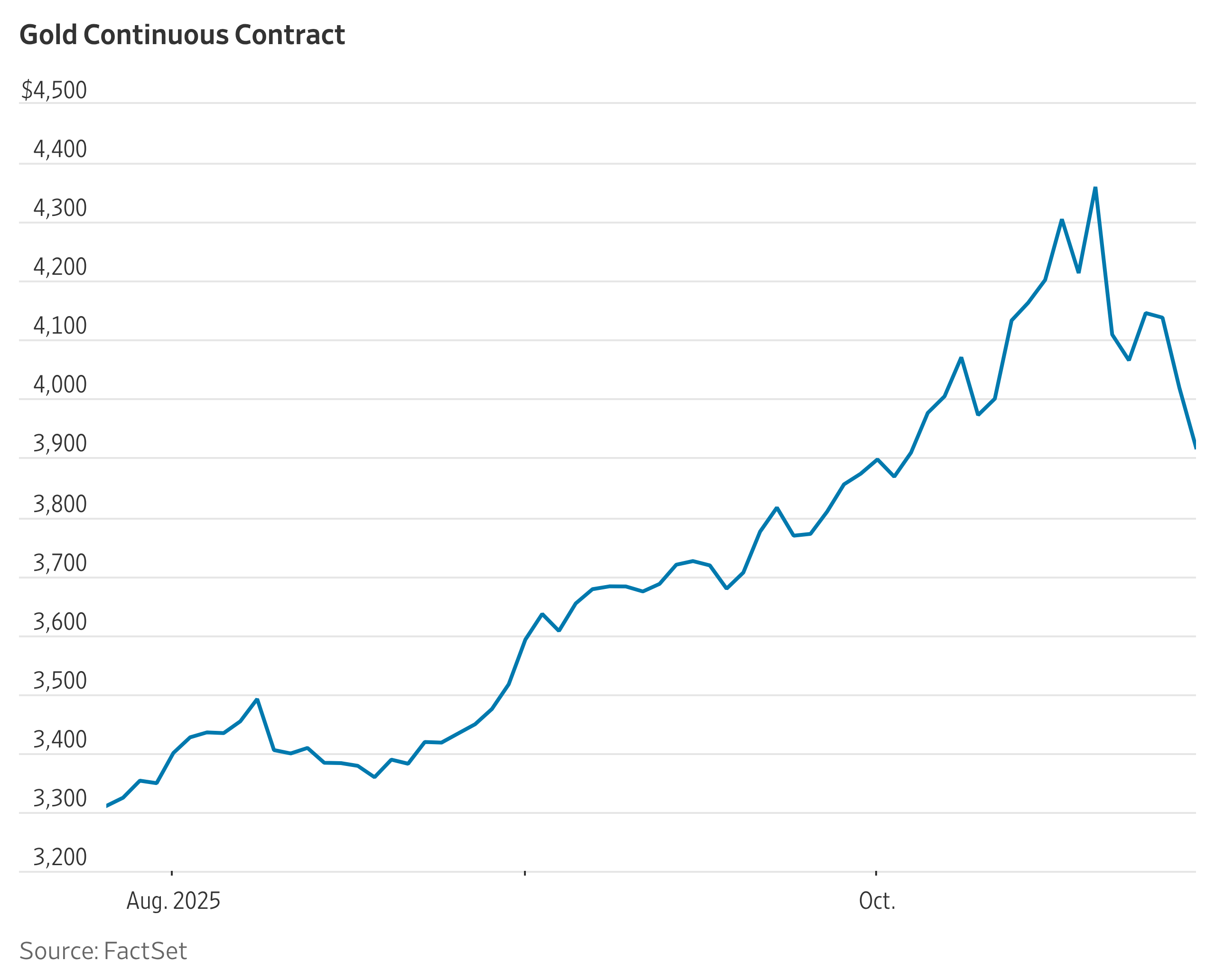

Brent crude prices were trading at $108 a barrel after Iran threatened Gulf oil and gas facilities on Wednesday — the price was just under $70 a month ago. European wholesale natural gas prices have risen roughly 70 per cent, from €29/MWh to €50/MWh. These increases are large and will hurt, but the gas price rise in particular is far smaller than those in 2021 and 2022.

Clearly, taking comfort from this comparison might soon feel misplaced if the Strait of Hormuz remains persistently blocked. But there are other, more durable reasons to think European economies learned something from their experience after Russia’s invasion of Ukraine and are now more resilient to high energy prices.

Top of the list is the fact that Europe’s natural gas consumption has fallen as GDP expanded, given a contraction in the output of energy-intensive industries. Compared with the five-year average between 2017 and 2021, EU gas consumption was down 16 per cent in 2025. UK imports of gas were 17 per cent down in 2025 compared with 2021.

Higher wholesale gas prices will still feed through to industry and heating bills. But in the electricity market, a reduction in relying on gas generation is steadily limiting the time during which the spot price will be determined solely by fossil fuels. The UK Energy Research Centre, an academic consortium, estimates that the proportion of time that gas prices set the electricity price will fall from 90 per cent to 60 per cent over the next three years.

Low marginal cost renewables are pushing the most expensive gas generators out of the market more often, gradually delinking power prices from those of fossil fuels. Spain is furthest along this path. Customers do not pay the close-to-zero marginal cost of renewables, because capital costs must be funded, but the greater stability of electricity prices is something to applaud.

Central banks need to ensure that they will not allow price rises to generate persistent inflation. And they have some assistance in this task: weaker labour markets than in 2022, lower global demand for goods and fewer supply chain bottlenecks than in the immediate post-Covid period.

If these forces limit inflationary pressure, the demand for governments to rescue society from an energy price shock, pushing the burden on to future generations, is also reduced.

In the UK, the last government’s 2022 energy windfall taxes — the energy profits levy and the electricity generator levy — are still in place. They were withering on the vine as energy prices fell below their thresholds, but will fund limited support for the most vulnerable households. Don’t expect too much, however, because the UK and other European countries are energy importers, so windfall gains are never remotely sufficient to compensate losers.

All the mitigations will help governments to offer only temporary, targeted support to companies and households, rather than the very expensive, ill-targeted programmes of 2022. The silver lining to today’s economic cloud is that Europe is collectively stronger than four years ago. But an energy price shock is still overwhelmingly bad news.