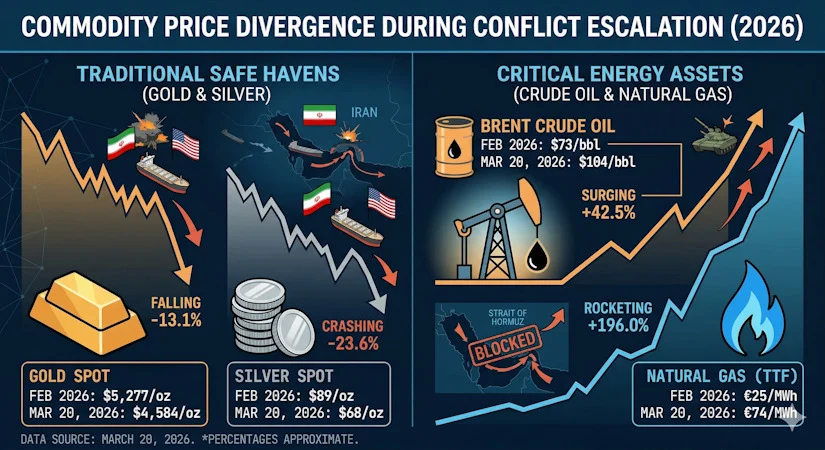

He added that gold demand in India and China remains strong, supported by currency depreciation trends over the past year.

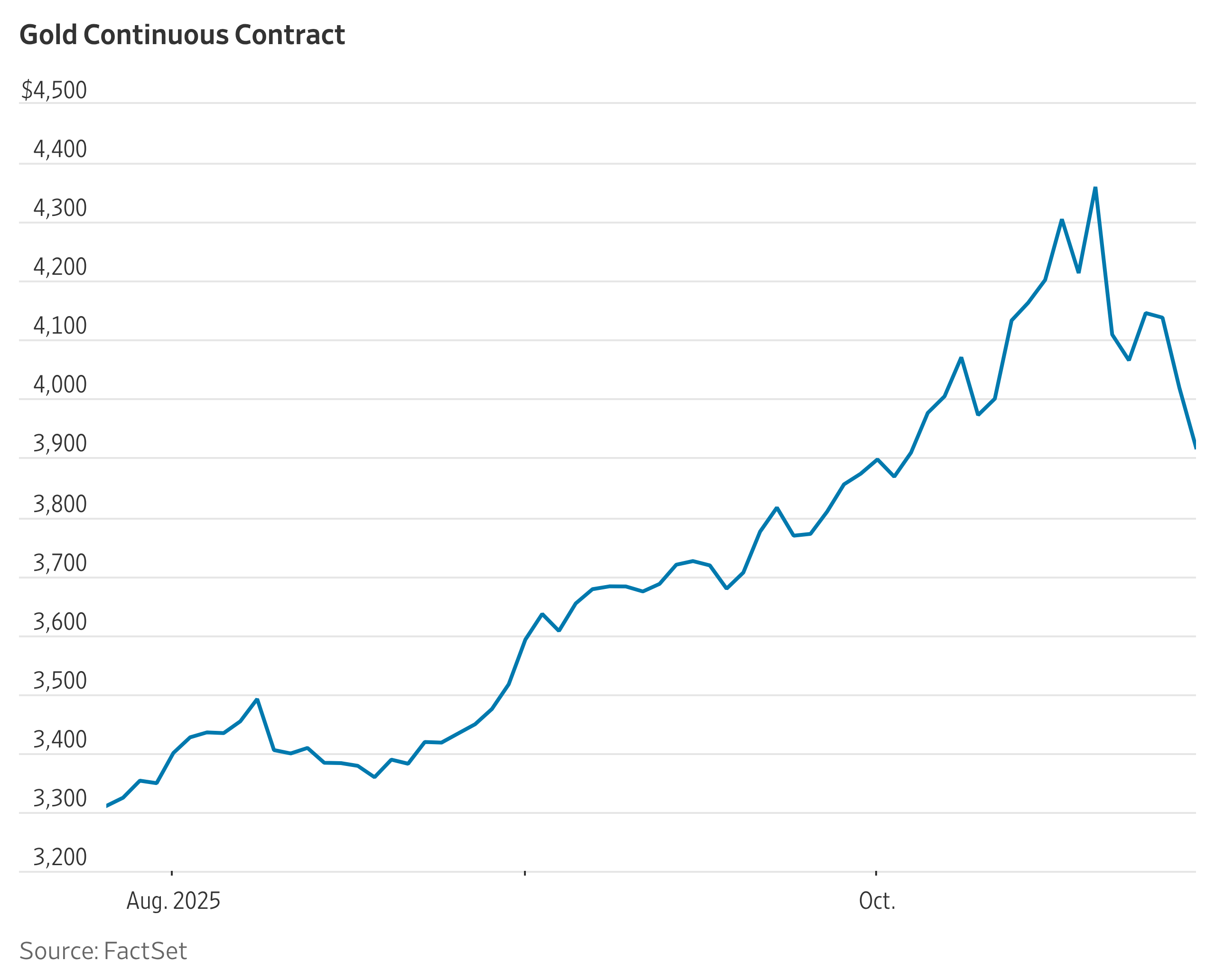

However, a recent appreciation in the Indian rupee has contributed to downward price adjustments on the MCX. Kumar also flagged that a sharp rise in oil prices–estimated at around 75 per cent–could push global inflation higher, reinforcing gold’s traditional role as a hedge, even as near-term pressures persist. A sustained break above USD 4,800 could open the path toward USD 5,100, he said.

Dinesh Somani, Founder, Intellitrade, highlighted that the ongoing Middle East conflict has, unusually, had a negative impact on bullion prices.

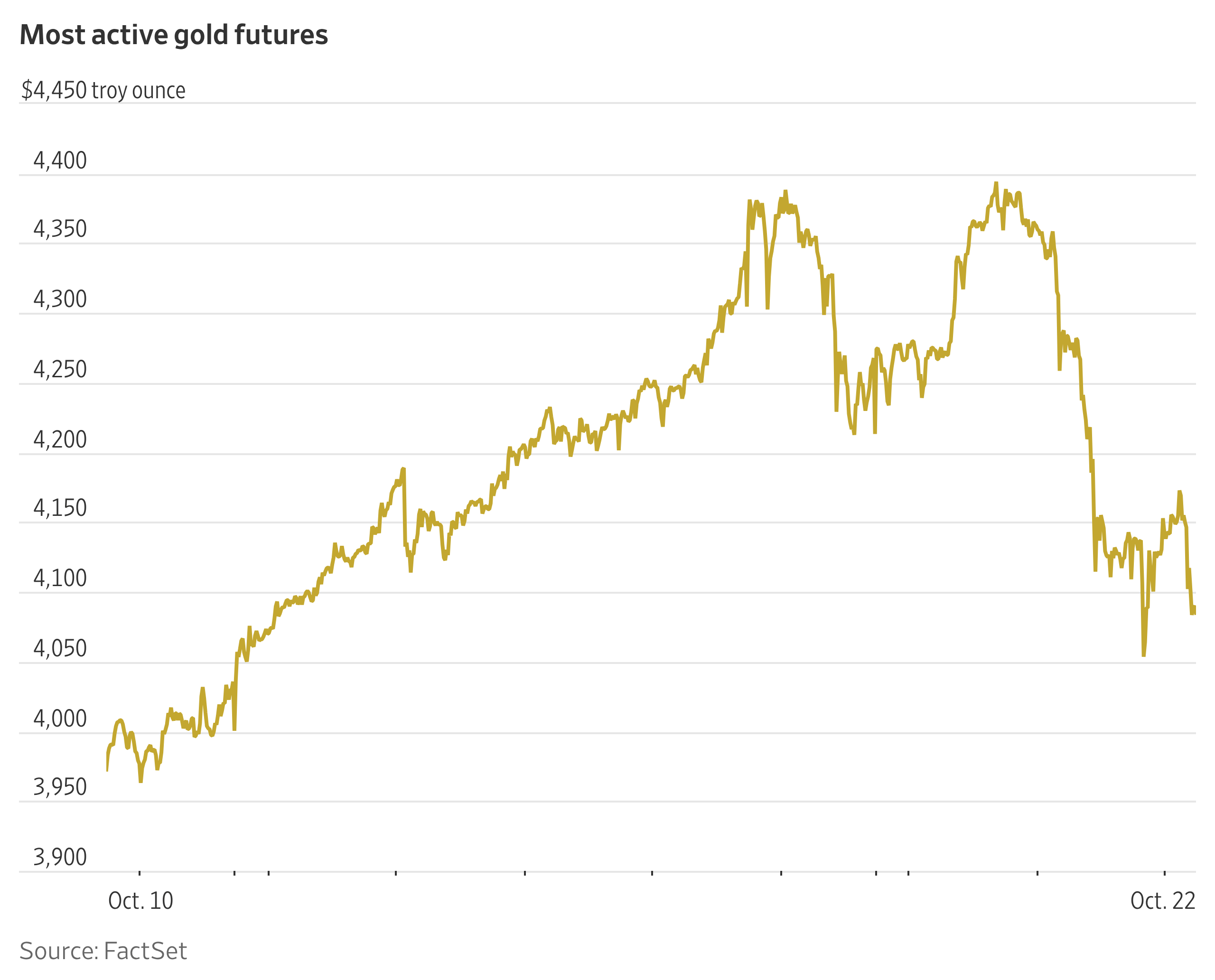

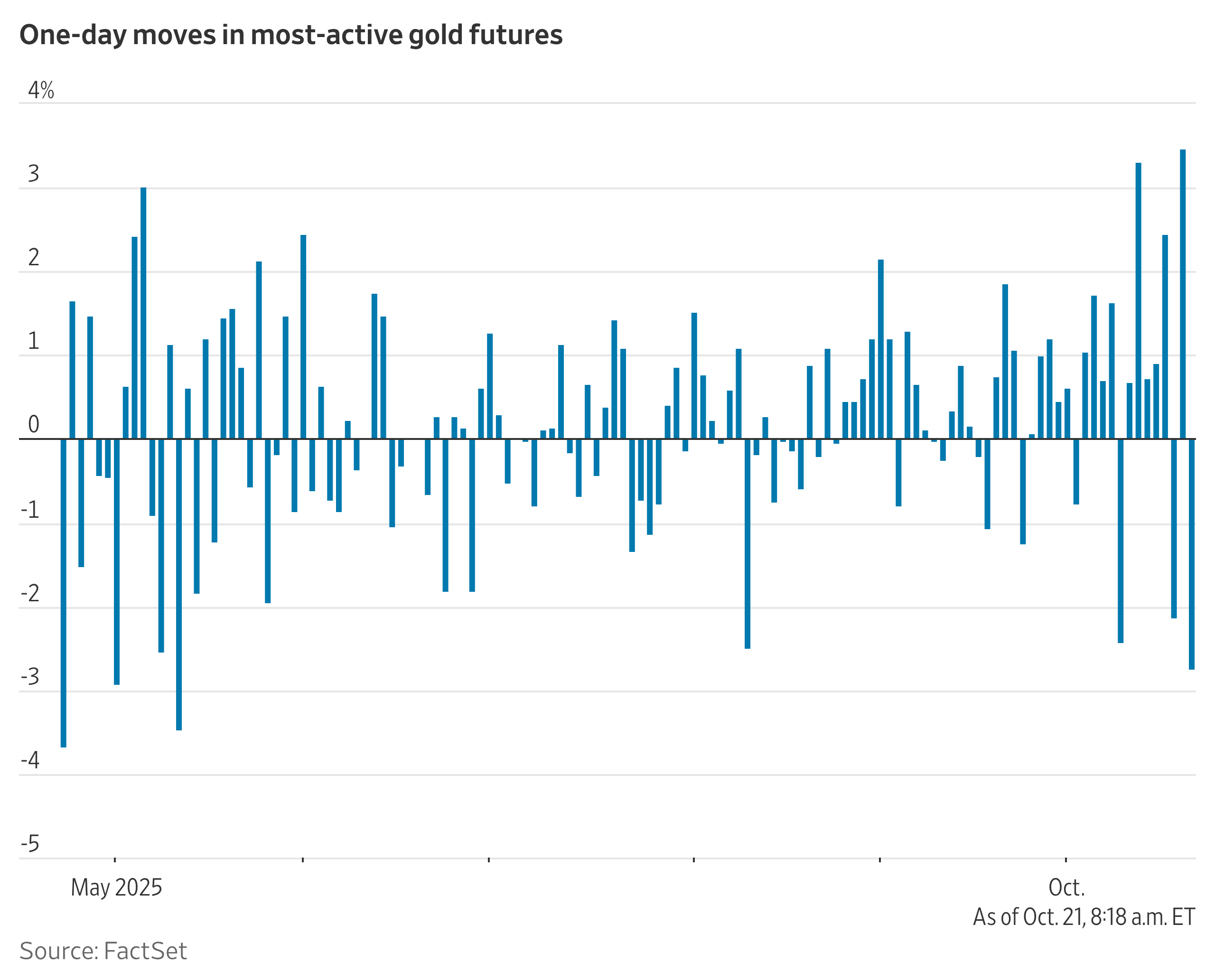

“For the first time, the war has weighed on gold despite its safe-haven status,” he said, noting that prices fell from around USD 5,600 per ounce on COMEX to near USD 4,100 during the recent correction.

Somani attributed the decline to a combination of factors, including fading ETF demand, slower central bank buying and expectations of higher interest rates amid rising crude oil prices. He also pointed out that some central banks have offloaded gold reserves, adding to market pressure.

“In the absence of fresh triggers, gold is likely to remain range-bound,” Somani said, pegging the near-term band between USD 4,100 and USD 4,970 per ounce.

Analysts broadly agree that while geopolitical risks remain, the interplay of inflation, oil prices and monetary policy will be the dominant drivers in the near term, keeping gold in a choppy consolidation phase rather than a decisive trend.