At the Hubbis Independent Wealth Management Forum – Singapore 2026, Lakhwinder Singh, Manager at J. Rotbart & Co., set out a case for viewing precious metals not only as a portfolio diversifier, but as a tool for liquidity, ownership, geopolitical resilience and cross-border wealth protection.

His presentation moved beyond the familiar discussion of gold and silver performance. Instead, Singh focused on why physical precious metals, held across multiple global locations, are becoming more relevant for UHNW clients in an environment shaped by geopolitical instability, currency risk, central bank demand, industrial demand and rising concern around single-location exposure.

The message was not that precious metals should be viewed as a speculative asset class. It was that gold and silver can play a strategic role in portfolio construction, wealth preservation and estate planning when ownership, storage, access, insurance and jurisdictional diversification are properly considered.

For Singh, the core issue is optionality. Clients want the ability to hold physical assets in their own name, store them in secure private vaults, relocate them across jurisdictions, borrow against them where appropriate, and move between traditional assets, precious metals and newer digital asset solutions when needed.

Key Takeaways

- Precious Metals Are A Geopolitical Diversification Tool: Singh argued that gold and silver should be considered not only for portfolio diversification, but also for jurisdictional resilience.

- Single-Location Storage Is Increasingly Risky: Ongoing geopolitical uncertainty means clients should not assume any one location can provide complete security.

- Location Optionality Matters: J. Rotbart & Co. encourages clients to store metals across multiple hubs, with Hong Kong, Singapore and Zurich described as the firm’s most discussed “trifecta”.

- Physical Ownership Is Different From Paper Exposure: Singh argued that ETFs and paper holdings may provide price exposure, but do not offer the same level of direct ownership, access or control as physical metals.

- Private Vaults Offer A Different Value Proposition: Private vaulting was presented as offering regular audits, access, full liability coverage and assets held in the client’s own name.

- Gold Remains A Long-Term Wealth Preservation Asset: Singh positioned gold as liquid, stable over long periods and the preferred reserve asset of central banks.

- Silver Has A Strong Industrial Demand Case: Silver was presented as increasingly difficult to source, with demand supported by electronics, EVs, medical applications and other industrial uses.

- Central Bank Demand Remains A Key Long-Term Driver: Singh said sustained central bank gold accumulation continues to support the long-term outlook for precious metals.

- Liquidity Can Be Created Without Selling: Clients with long-term physical holdings may be able to borrow against precious metals rather than liquidating them.

- Clients Want Options Across Assets And Locations: Singh emphasised the importance of being able to buy, store, move, finance and diversify across multiple jurisdictions and asset categories.

Singh opened by noting that his presentation would take a slightly different direction from a standard precious metals outlook.

Rather than focusing only on price performance, he said the more important topic was diversification and liquidity. That diversification, in his view, is not only about reducing portfolio risk or improving performance. It is increasingly about geopolitical diversification.

The distinction matters. Gold and silver have long been discussed as portfolio stabilisers, particularly in periods of crisis. But Singh argued that the question of where those assets are held has become just as important as whether they are held at all.

“Precious metals are essential to the portfolio,” he said. “But in today’s environment, where they are stored can matter almost as much as owning them.”

He pointed to geopolitical uncertainty across the Middle East, the Russia-Ukraine war, tensions in APAC and wider instability around the world. For Singh, these developments show that there is no single location that can provide a one-stop answer to security.

The implication for UHNW clients is clear. Precious metals may help diversify a portfolio, but if the assets are concentrated in one jurisdiction, the client may still carry location risk.

The Case For Geographic Diversification

Singh then turned to the practical importance of storing precious metals across multiple jurisdictions.

He described a recent client example involving multibillion-worth gold and silver holdings in a private vault in Dubai. When war broke out, the Middle East no longer felt as safe as it once had. The client needed to reduce exposure to that location and move assets elsewhere.

J. Rotbart & Co., Singh said, was able to facilitate a door-to-door relocation of assets from Dubai to Singapore, with full liability coverage. He noted that logistics during war are particularly difficult, with war insurance and transport arrangements becoming more complex.

“The point is not that one location is always safe and another is not,” he said. “The point is that clients need the ability to move when circumstances change.”

For Singh, this example reinforces why clients should avoid relying on a single storage jurisdiction. The firm encourages clients to hold precious metals across multiple locations, with Hong Kong, Singapore and Zurich described as the three most popular hubs among its clients.

That “trifecta” reflects the broader logic of geopolitical diversification. Clients are not simply choosing vaults. They are building resilience into the physical location of their wealth.

Performance, Correction And The Long-Term Role Of Metals

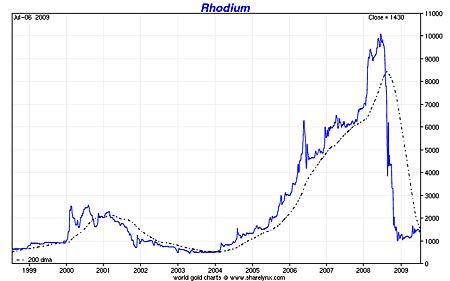

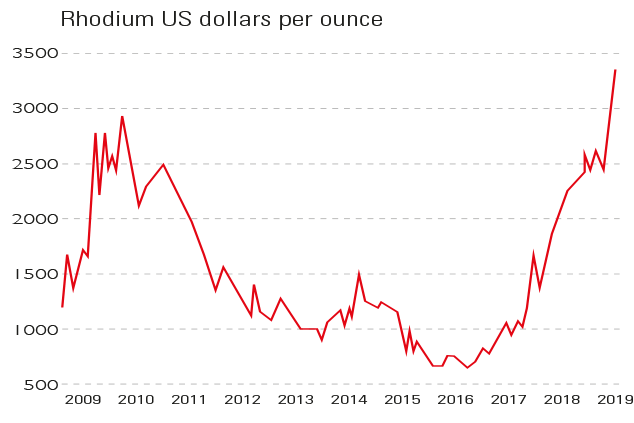

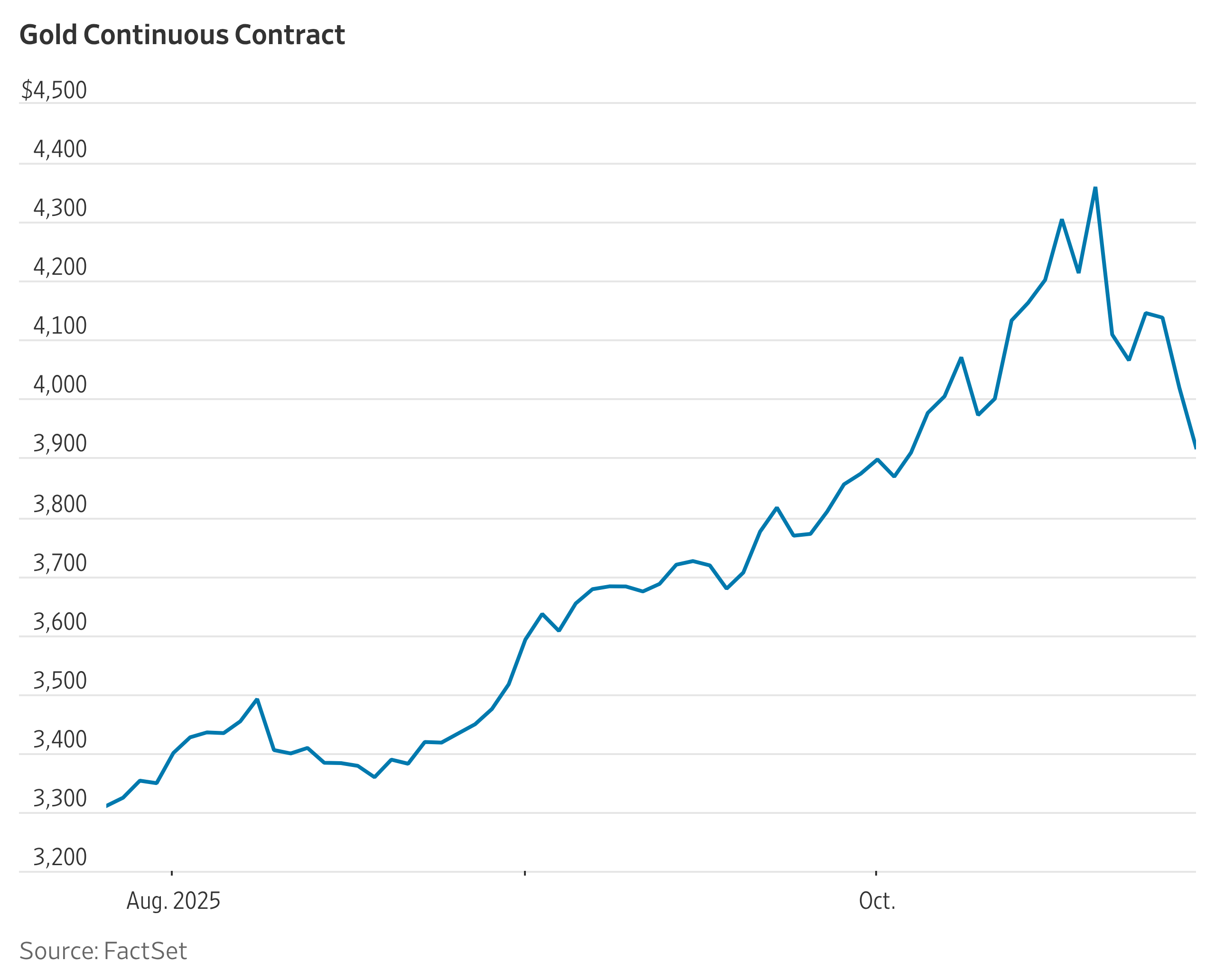

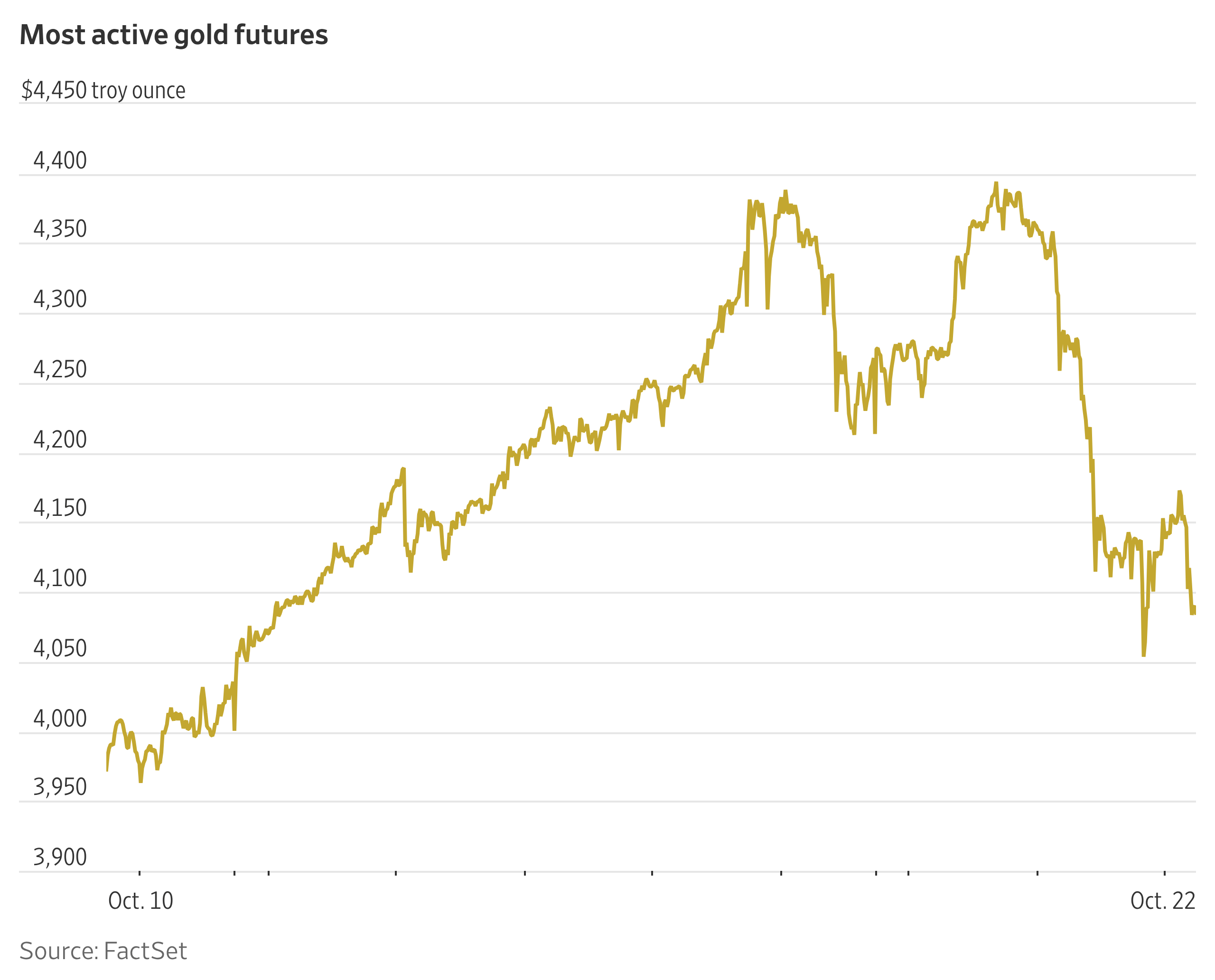

Singh acknowledged that precious metals have delivered strong portfolio performance over the past three years.

However, he cautioned against viewing gold and silver as assets that should be expected to generate 3x or 5x returns. Their role, in his framing, is not to behave like speculative growth assets. Instead, they are intended to provide stable long-term returns and diversification benefits over time.

He noted that recent returns had been strong, citing gold and silver as having delivered significant gains, while also acknowledging that a correction was overdue.

“Gold and silver are not meant to be lottery-ticket assets,” he said. “They are meant to provide resilience, liquidity and long-term stability.”

Singh said profit-taking has been one factor behind recent correction dynamics. He also pointed to liquidity rotation between physical and paper markets, a strong US Dollar during the Trump administration, Middle East dynamics, and rising real yields as factors that can weigh against precious metals performance.

Yet his longer-term view remains constructive. The reason, he argued, is that the structural drivers have not disappeared.

Central Bank Demand As A Core Driver

For Singh, central bank demand remains one of the most important long-term supports for precious metals, particularly gold.

He said he has been discussing this factor with clients since 2017, describing central bank demand as a major reason to expect precious metals to continue rising over the coming years. According to Singh, central banks have been accumulating gold reserves at record levels since 2016 and continue to add to those reserves.

The meaning behind this demand is important. In his view, central banks are buying gold because uncertainty remains high and because there is still a lack of full trust in traditional financial assets.

“When central banks keep adding gold, they are sending a message,” he said. “They are preparing for uncertainty, and private clients should understand why that matters.”

Singh argued that as long as central banks continue buying and adding to reserves, the outlook for precious metals remains positive.

He also said that long-term data supports the inclusion of gold in portfolios, arguing that portfolios with precious metals exposure have historically delivered better outcomes than portfolios without that diversification allocation.

Gold: Liquidity, Stability And Wealth Planning

Singh then addressed the role of gold within a precious metals portfolio.

Gold remains one of the most popular and widely recognised precious metals assets. Singh positioned it as a long-term store of value, a highly liquid asset and the reserve asset of choice for central banks seeking to support confidence in their economies.

For private clients, the appeal is not only performance. It is also ownership, access and continuity.

Physical gold can support long-term wealth planning because it is a tangible asset that can be held directly and passed to the next generation. This is different from exposure through paper instruments or financial platforms, where clients may not have the same practical ability to take delivery, transfer ownership or access the asset outside the financial system.

“Gold is not only a market exposure,” he said. “For many families, it is a physical asset that supports long-term continuity.”

This is where Singh drew a clear distinction between owning gold through ETFs or paper holdings and owning physical gold. Many investors already have some exposure to gold or silver, he suggested, but much of it is through ETFs. In his view, that is not the same as holding a physical asset in the client’s own name.

Silver: Industrial Demand And Constrained Supply

Silver was presented as a different but increasingly important part of the precious metals conversation.

Unlike gold, Singh framed silver more explicitly as an industrial asset. He pointed to strong demand and limited supply, noting that clients have been sourcing silver heavily over the past year and a half.

He said sourcing silver has become one of the most difficult parts of the business in recent months, largely because industrial demand continues to absorb available output.

“Silver is not only a precious metal story,” he said. “It is an industrial demand story.”

Singh highlighted electric and electronic applications as key drivers, including EVs, cars, medical and health-related technologies, and broader electronics use. In his view, anything connected to electrification and electronic infrastructure reinforces silver’s relevance.

This creates a different demand profile from gold. While gold is anchored more heavily in reserve accumulation, wealth preservation and liquidity, silver has a significant industrial demand component that may continue to support its outlook.

Why Physical Metals Matter

Singh then addressed a central question for advisers and clients: why own physical precious metals rather than only paper exposure?

He suggested that many people in the room likely already had some exposure to gold or silver, but mainly through ETFs. Paper holdings can provide price exposure, but Singh argued that they do not provide the same degree of ownership, access or flexibility as physical metals.

Clients who have held gold through banks or platforms may find it more difficult to liquidate, transfer or take physical ownership when needed. Physical gold, by contrast, can be held directly, stored privately and integrated into long-term wealth planning.

“If the client wants 100% ownership, paper exposure does not always answer the question,” he said. “Physical ownership gives them control over the asset itself.”

This is particularly relevant for families thinking beyond investment performance. Physical metals can be part of succession planning, intergenerational wealth transfer and emergency liquidity planning.

For Singh, the key issue is that clients should understand the difference between exposure and ownership. They may both have a place, but they are not the same.

The Role Of Private Vaults

Singh also explained why private vaults play an important role in the physical precious metals proposition.

In Singapore, he highlighted Freeport as one of the most popular locations used by clients and described it as one of the most secure locations in the world. The key advantages of private vaulting, in his view, include regular audits, easy access and full liability coverage.

He contrasted this with bank safe deposit boxes, where clients may not receive the same level of liability coverage for assets stored inside them.

“Security is not only about where the metal sits,” he said. “It is about access, auditability, liability coverage and the asset being held in the client’s own name.”

This links back to the broader theme of uncertainty. In a world where clients are increasingly concerned about geopolitics, banks, access and ownership, holding physical metals in a private account under the client’s name becomes more important.

Private vaulting is therefore not only a storage choice. It is part of the broader governance and resilience framework around the asset.

Liquidity Without Forced Selling

Singh then turned to another important function of physical precious metals: the ability to create liquidity without necessarily selling the asset.

He described clients who had stored several million dollars in precious metals since 2021 and had seen the value of those assets increase significantly. Rather than liquidating the holdings, they were able to take loans against the metals and use that capital for external investments.

This creates a different way of thinking about liquidity. Physical gold and silver do not have to be inert assets sitting in storage. With the right infrastructure, they can potentially support borrowing, collateralisation and wider investment planning.

“The asset does not always need to be sold for the client to access liquidity,” he said. “For long-term holders, lending against metals can preserve exposure while releasing capital.”

For UHNW clients, this may be particularly relevant when precious metals are held as part of a long-term wealth preservation strategy. If the client wants to maintain exposure but also deploy capital elsewhere, secured lending can provide another option.

Connecting Precious Metals, Crypto And Client Optionality

Singh said one of J. Rotbart & Co.’s more popular services this year has involved connecting crypto and precious metals solutions.

The presentation positioned this not as a replacement of one asset class by another, but as part of a broader client demand for optionality. Clients increasingly want access to multiple asset categories, including traditional assets, precious metals and crypto-related solutions.

They also want the ability to store, buy and move assets across multiple jurisdictions, including Singapore, Hong Kong, Zurich and the UAE.

“Clients want options,” he said. “They want options across assets, and they want options across locations.”

For Singh, this is consistent with the wider shift in wealth management. Clients are not only seeking performance. They are seeking flexibility, jurisdictional choice, access, security and the ability to move between different forms of value when circumstances change.

This makes infrastructure and execution increasingly important. Advisers and partners need to be able to support not only the purchase of metals, but also trading, storage, logistics, lending and relocation.

A One-Stop Physical Precious Metals Platform

Singh concluded by positioning J. Rotbart & Co. as a one-stop solution for physical precious metals.

He described the firm’s services across trading, logistics, secure shipping, secure storage and lending. He also emphasised the firm’s global footprint, including access to more than 16 private vault locations and more than 60 locations where clients can shift precious metals.

The presentation highlighted strong demand from clients moving assets from North America and Europe towards Asia, reflecting the same geopolitical and jurisdictional diversification themes that ran throughout the session.

For Singh, the firm’s role is to give clients and advisers more options. Those options may involve where metals are stored, how they are transported, how they are financed, how they are accessed, or how they sit alongside other asset categories.

The presentation ended with a clear message for advisers serving UHNW clients. Precious metals should not be viewed only through the lens of price performance. They should be considered as part of a broader resilience framework, covering ownership, liquidity, storage, jurisdictional diversification and long-term wealth planning.

In Singh’s framing, gold and silver remain relevant because they give clients something increasingly valuable in a volatile world: tangible ownership, geographic flexibility and the ability to act when conditions change.