Retirees now have more flexibility, but that does not make the decision any less critical. Even a small portion locked into the wrong annuity plan can shape your income for decades. For example, the annuity rates—and hence the regular payout—vary by the life insurance provider.

Depending on the insurer you choose, the gap between the payouts issued by two companies could be over Rs.50,000 a year, while all other components remain the same. Hence, comparing the options is crucial. But before doing that, retirees need to figure out how much annuity they need to purchase. Is it advisable to go beyond 20%? That depends on multiple factors.

Post-retirement, an annuity acts as a substitute for salary. “The annuity should ideally be aligned with essential monthly expenses to ensure a stable inflow irrespective of market conditions,” says Sriram Iyer, MD and CEO, HDFC Pension.

If your monthly needs are Rs.20,000 but your annuity generates only Rs.10,000, you are effectively depending on markets for the rest. That may work in good years, but markets are not designed to meet fixed expenses.

Lovaii Navlakhi, MD of financial planning firm IMMPL and a certified financial planner, says, “It depends on the cash flow requirements and also the discipline of the client.” If investors are likely to chase returns or react to market swings, “it’s better to lock into a larger portion through annuity,” he adds. Annuity is not just about rates, but behaviour too.

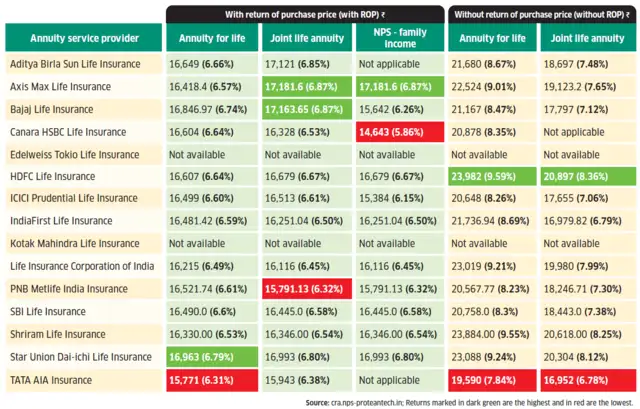

Rates with different annuity service providers

Monthly income on an annuity purchase of Rs.30 lakh by a male aged 64, with spouse aged 63.

Annuity vs SWP

However, many retirees and even financial advisors prefer systematic withdrawal plan (SWP) over increasing the annuity and in most cases SWP is superior to annuities. From a returns perspective, the difference may not be dramatic.

When SWPs are structured using low-risk instruments like short-term debt funds, returns are broadly similar to annuities, says Shilpa Bhaskar Gole, Partner & Principal Officer at NerdyBird Wealth Advisory. However, the real difference emerges after tax and in flexibility.

“Annuity payouts are fully taxable at slab rates, whereas in an SWP only the gains component is taxed,” she points out.

SWPs also offer liquidity and flexibility. Sumeet Hemkar, Partner, Deloitte India, observes, “SWP offers investors flexibility to vary withdrawal amounts and timing and therefore, is more tax efficient over the investment horizon.”

But the biggest drawback of annuities, Gole notes, is inflation. Fixed payouts lose purchasing power over time. Even increasing annuities typically grow at around 3%, which may not keep pace with real-world expenses such as healthcare or lifestyle costs.

However, SWPs require discipline. Investors must be willing to stick to conservative asset allocation and not chase higher returns during market upcycles, Navlakhi cautions.

If you can’t follow a plan, it’s better to move to annuities above 20%.

Choose the right option

Once you’ve figured out how much guaranteed income you need, the next step is to figure out what trade-off you are willing to make. The monthly payout difference between a life annuity without return of purchase price (highest) and a joint-life annuity with return of purchase price (lowest) can be 25–30%. That gap is the price of coverage protection for your spouse and return of capital for your nominee.

If your priority is a higher monthly payout, the basic life annuity is more appealing. It pays the most, but the income stops after your lifetime, with nothing left for your family. Options that return the purchase price ensure your nominee gets the original corpus back, but the monthly income drops noticeably.

If your spouse depends on your income, joint-life options make sense because the payouts continue even after one partner passes away. This is less about rates and more about avoiding a sudden income shock for the surviving spouse.

When retirees tend to regret

The problem with annuity decisions is that they don’t feel wrong immediately. The gaps only show up years later.

For instance, a fixed-period annuity for 10–15 years can look neat on paper. But retirement doesn’t work on a fixed timeline. If you outlive that period, the income stops, even though your expenses don’t.

On the other hand, chasing a higher payout can create a different problem. Options that maximise income often do so by giving up any return of capital. If the annuitant passes away early, the total amount received can end up being much lower than what was invested.

Moreover, annuity rates depend on interest rates at the time of purchase. Once locked in, they don’t change. So if rates move up later, there’s no way to benefit from that. At the same time, going too light on annuity isn’t always ideal either.

The way to avoid these pitfalls, make an informed decision. Use annuity to cover essential, non-negotiable expenses, and avoid relying on uncertain returns for those needs. Once that base is secured, the remaining corpus can be used more flexibly for growth, inflation and discretionary spending.