Drive west out of Abilene, Texas, and the future of the technology industry announces itself the way heavy industry always has: earthworks, transmission lines and steel going up faster than seems entirely plausible. On more than 980 acres, Crusoe Inc. — a company that began its life burning waste natural gas to mine bitcoin — is building what may be the largest concentration of computing power ever assembled.

The first phase is live, serving Oracle Corp.’s and OpenAI Group PBC’s Stargate program. The expansion underway takes the campus to 1.2 gigawatts. In March, Crusoe announced a second, adjacent 900-megawatt campus dedicated to Microsoft. Full buildout points toward 2.1 gigawatts on a single site — roughly the output of two nuclear reactors, feeding on the order of 400,000 top-shelf GPUs.

It is worth pausing on what that is. Not a data center in the old sense — a beige building humming politely at the edge of a suburb — but a factory, in the literal sense the industry has now adopted without irony. Energy goes in one end; intelligence, metered in tokens, comes out the other. Crusoe raised $1.375 billion in late 2025 at a valuation north of $10 billion, with more reportedly coming, and secured 4.5 gigawatts of natural gas through a joint venture to keep the production lines fed. The company’s founding insight — put compute where energy is cheap and stranded, because moving electrons is harder than moving data — has gone from a crypto-era arbitrage to the organizing principle of a global buildout.

This is a report on the state of that economy: where the money is going, what the machines are actually doing, and the three questions that will decide whether mid-2026 is remembered as the moment the industry matured — or the moment it peaked.

Energy goes in one end; intelligence, metered in tokens, comes out the other.

Crusoe’s trajectory illustrates the whole category. Its founders — a quant trader and an energy scion — began by capturing flared gas at oil wells, an environmental fix that doubled as cheap power. When AI demand detonated, the same logic scaled: Don’t bring energy to the compute, bring compute to the energy. The result is that the biggest names in software — OpenAI, Oracle, Microsoft Corp. — now anchor their most ambitious infrastructure on a company that was, five years ago, a clever footnote in the bitcoin story. Hyperscalers with hundreds of billions in capital spending budgets still cannot build fast enough, and speed, not capital, has become the scarce resource.

The factory age has a price beyond capital, and it is measured in megawatts and methane. Crusoe’s 4.5-gigawatt gas joint venture sits awkwardly beside its climate-aligned origin story, and the company is hardly alone: Across the industry, the power hunger of AI has quietly rewritten the sustainability commitments of nearly everyone involved. The honest framing — one the industry is only beginning to say out loud — is that the buildout is being financed on the assumption that intelligence is worth more than the externalities of producing it. That assumption may be right. It has not been demonstrated.

And behind it lurks the bear case that every infrastructure veteran carries like a scar: the fiber glut of 2000, when a genuine technological revolution nonetheless incinerated the capital of the companies that built its plumbing. The skeptic’s syllogism is simple. Demand projections are stacked on demand projections; some financing is circular, with chipmakers investing in the clouds that buy their chips and model labs committing to capacity they will pay for with money raised against the value of those very commitments. If token demand merely grows very fast — rather than absurdly fast — a meaningful share of the gigawatts under construction will open into a glut.

The counterargument is the rest of this report: Unlike fiber in 1999, the capacity being built in 2026 is sold out before it is energized, by customers with revenue. Which makes the real question not whether the factories will be used, but whether the businesses using them make money. For that, you have to follow the tokens.

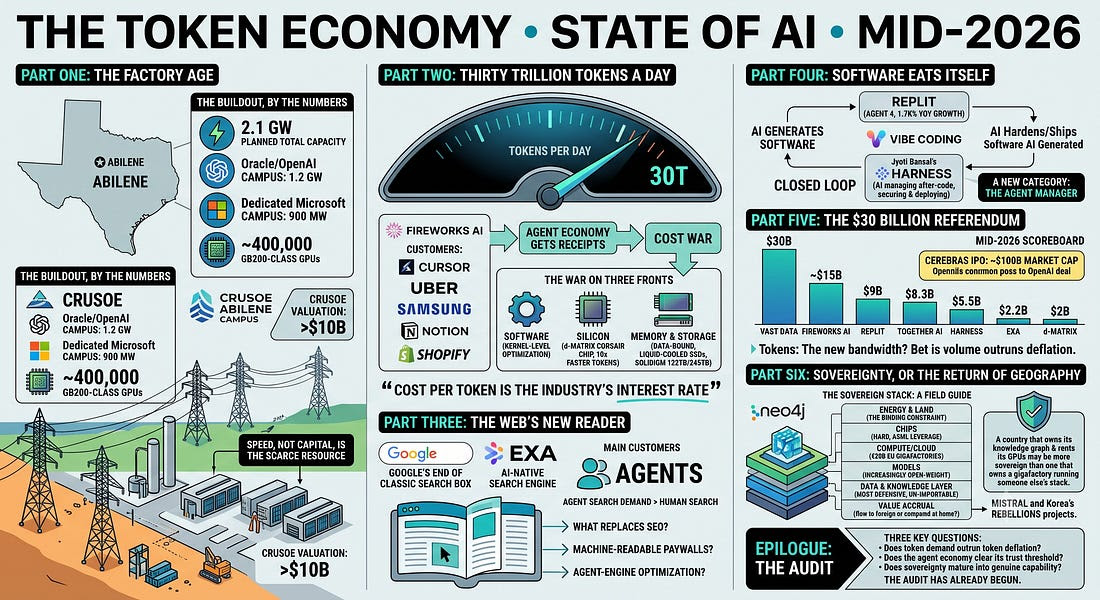

The buildout, by the numbers

• 2.1 GW — planned total capacity of Crusoe’s Abilene site across the Oracle/OpenAI campus (1.2 gigawatts, phase two completing 2026) and the dedicated Microsoft campus (900 megawatts, first building energized mid-2027).

• ~400,000 — GB200-class GPUs the full Abilene build can host across eight buildings on 980+ acres.

• 4.5 GW — natural gas capacity Crusoe secured via joint venture with Engine No. 1.

• $1.375B — Crusoe’s Series E (October 2025), at a valuation above $10 billion.

• ~€20B — the EU’s AI gigafactories initiative via EuroHPC, targeting facilities of ~100,000 processors each.

Thirty trillion tokens is not a chatbot statistic. Numbers like that happen when software calls software: coding agents that decompose a request into hundreds of model calls; support agents that read, reason, retrieve, and write in loops; pipelines where one user click detonates a cascade of inference. 2026 was widely nominated, at last year’s conferences, as the year agents would go from demo to production.

The token data says the nomination was accepted — with an asterisk. Agents went to production where the economics worked, and the economics work only where the cost per task is low enough. That is why the defining competition of this phase of the industry is not a capability race but a cost war.

The war is being fought on three fronts at once. The first is software: kernel-level optimization of the kind Fireworks and its rival Together AI Inc. (which closed an $800 million round at an $8.3 billion valuation on July 1, on annualized bookings above $1.15 billion) treat as core intellectual property.

The second is silicon. Fast growing d-Matrix Inc., a Santa Clara chipmaker founded by networking silicon veterans Sid Sheth and Sudeep Bhoja, spent seven years betting that inference’s villain is the memory wall — the energy and time wasted shuttling data between processor and memory — and moved the math into the memory itself. Its Corsair accelerator entered full production in June, shipping in volume, with rack-level claims of roughly 10 times faster token generation at a third of the cost and a fifth of the energy for latency-sensitive work, and an independently verified demonstration cut a 24-second response to under two. Notably, d-Matrix does not propose replacing the GPU but pairing with it — a coexistence strategy that says something about how mature this market has become: The challengers are no longer storming the castle; they are leasing rooms in it.

The third front is the humblest and, increasingly, the most surprising: memory and storage. Solidigm, the SK hynix Inc. subsidiary shipping 122-terabyte solid-state drives with 245-terabyte models on the 2026 roadmap, has spent the year evangelizing a heresy that is quietly becoming consensus: AI data centers are becoming data-bound, not compute-bound. Agents with million-token contexts generate enormous key-value caches that must live somewhere fast; retrieval pipelines hammer storage in patterns training never did. When the industry’s hottest thermal-engineering project is a liquid-cooled SSD co-designed with Nvidia Corp., the definition of “AI infrastructure” has officially expanded beyond the GPU.

Stitch the three fronts together and the strategic picture clarifies. Cost per token has become the industry’s interest rate — the single variable that decides which agent business models clear. Every percentage point it falls, some previously impossible product becomes viable, and some incumbent’s pricing becomes untenable. The companies profiled here are not competing to make AI smarter. They are competing to make it cheap enough to be everywhere. History suggests that is the more lucrative ambition.

Cost per token has become the industry’s interest rate — the variable that decides which business models clear.

Exa’s thesis, articulated by co-founder Will Bryk, is that as agents proliferate, machine search demand will grow to hundreds or thousands of times human search volume — software researching, comparing, verifying and citing at a scale no population of humans could match. The company’s embeddings-first index already answers queries for Cursor, Cognition, HubSpot and more than 400,000 developers, at speeds (sub-180 milliseconds) tuned for programs that fire dozens of searches per task. Bryk has argued agents will outsearch humans within the year. His valuation — tripled in under 12 months — suggests investors believe him.

The second-order consequences are the interesting part, and nobody in the industry has honest answers yet. The web’s economic engine is a grand bargain: Content is free because humans see ads next to it. An agent does not see ads. If the primary readers of the open web become machines — extracting facts, synthesizing answers, never clicking — the bargain collapses, and with it the funding model for the content the machines are reading.

Publishers already feel the leak; the lawsuits and licensing deals of the past two years were the opening skirmish. What replaces search-engine optimization — agent-engine optimization? machine-readable paywalls? per-crawl micropayments? — will decide who gets paid for knowledge on a web where attention is no longer the currency.

There is a sovereignty subplot here too, easy to miss and hard to unsee: If a handful of American indexes become the memory through which every agent on earth understands the world, that is a concentration of epistemic power that makes the old debates about social-media algorithms look quaint. Europe noticed. It tends to notice these things about a decade before it does anything, but it noticed.

Part 4: Software eats itself

The most visible cultural fact of the 2026 software industry is that the people writing software increasingly aren’t software people. Replit Inc. — the browser-based coding platform that became the flagship of what the industry affectionately calls vibe coding — raised $400 million in March at a $9 billion valuation, triple its price six months earlier, on annualized revenue estimated about $525 million and a public ambition to reach a billion-dollar run rate by year-end.

Users from 85% of the Fortune 500 build on it, most of them far from the information technology department. Its Agent 4 runs multiple coding agents in parallel on a single project; its president and head of AI, Michele Catasta, has framed 2026 as the year of the “agent manager” — the worker whose job is not to make things but to direct, review and orchestrate the fleets of software that do.

It is a genuinely new labor category, and it is arriving faster than the institutions around it. Which is precisely the alarm being rung, from the other end of the software lifecycle, by one of enterprise software’s most credentialed founders. Jyoti Bansal built AppDynamics Inc. and sold it to Cisco Systems Inc. for $3.7 billion; his current company, Harness — freshly funded with $240 million led by Goldman Sachs Alternatives at a $5.5 billion valuation, past $250 million in annual recurring revenue — is built on an inversion of the vibe-coding story.

AI made writing code nearly free, Bansal’s thesis goes, but writing code was never the expensive part. Testing, securing, deploying and governing it — everything after code — consumes some 70% of engineering effort, and the AI code flood is making that bottleneck catastrophically worse. Harness’ answer is to aim AI agents at the after-code lifecycle itself, reasoning over a knowledge graph of the entire delivery system: services, deployments, tests, incidents, policies, costs.

Read together, Replit and Harness describe a single closed loop that may be the most important industrial dynamic of the decade: AI generates the software, and AI must then inspect, harden and ship the software AI generated. Optimists hear compounding productivity. Pessimists hear a system removing its own circuit breakers. Both are describing the same machine.

What is no longer in dispute is the direction: the marginal cost of creating software is collapsing toward the marginal cost of describing it, and every assumption built on software being scarce — org charts, vendor pricing, the profession of programming itself — is now up for renegotiation.

AI generates the software — and AI must then inspect, harden, and ship the software AI generated.

Part 5: The $30B referendum

Vast is not an outlier; it is the pattern. Fireworks reportedly heading toward $15 billion. Replit at $9 billion. Harness at $5.5 billion. Exa at $2.2 billion. D-Matrix at $2 billion. Even the grizzled incumbents are being repriced: DataDirect Networks Inc. — the profitable, 25-year-old workhorse that feeds xAI’s hundred-thousand-GPU Colossus — took $300 million from Blackstone at $5 billion and spent 2026 openly courting another strategic investor. DDN’s coming valuation is a referendum, as one industry publication put it, on how the market prices the unglamorous parts of AI.

What makes mid-2026 different from every prior stretch of AI exuberance is that the market now has a public comparison. Cerebras Inc., the wafer-scale chipmaker, went public in May, raised $5.55 billion in the year’s biggest IPO, and watched its market capitalization approach $100 billion. The offering did two things at once: It validated the thesis that inference is a generational market, and it started the clock for everyone still private. Public markets are patient with stories exactly until a comparable company starts reporting quarterly numbers.

The private cohort’s revenue growth — Fireworks nearly tripling in five months, Replit’s 1,700% year-over-year, Together’s 10-figure bookings — is real and extraordinary. So is the gap between those numbers and the valuations built on them. Growing into a 60-times multiple requires nothing to go wrong, in an industry where the price of the underlying commodity — the token — is engineered to collapse.

That is the paradox the whole edifice rests on: Every company in this report is working furiously to make intelligence cheaper, while being valued as if the revenue from selling it will only compound. Both can be true — if volume outruns deflation, as it did for bandwidth, as it did for compute. The bet of 2026 is that tokens are the new bandwidth. The audit arrives when the first of these companies files an S-1.

The private repricing: Mid-2026 scoreboard

• Vast Data — $30B (Series F, April), $500M+ committed ARR, $4B+ cumulative bookings; Nvidia invested.

• Fireworks AI — ~$15B (reported round in progress), ~$800M annualized revenue (est.), ~30T tokens/day.

• Replit — $9B (Series D, March), ~$525M annualized revenue (est.), targeting $1B run-rate by year-end.

• Together AI — $8.3B (Series C, July 1), bookings above $1.15B annualized; Aramco Ventures led.

• Harness — $5.5B (December-announced round led by Goldman Sachs Alternatives), $250M+ ARR at 50%+ growth.

• Exa — $2.2B (Series C, May), 400,000+ developers; a16z led.

• d-Matrix — $2B (Series C), Corsair in full production June 2026; M12 and Temasek on the cap table.

Public comp: Cerebras — $5.55B raised in May’s IPO, market cap approaching $100B, anchored by a reported $20B OpenAI compute deal.

Part 6: Sovereignty, or the return of geography

The checks are getting large. The EU’s AI gigafactories initiative, backed by roughly €20 billion through the EuroHPC joint undertaking, aims at facilities with around 100,000 advanced processors each — a fourfold leap over the current generation. Mistral, Europe’s model champion, raised €1.7 billion in a round led by ASML — the Dutch lithography monopoly investing in the French model lab, about as legible as industrial policy gets. And the Mistral Compute venture is bringing some 18,000 Nvidia GB300s online south of Paris as a sovereign cloud for European workloads, independent of American and Chinese hyperscalers.

The pattern repeats globally: Korea’s National Growth Fund made its first-ever direct investment in the chip startup Rebellions under a program officials call, without embarrassment, the “K-Nvidia project”; Gulf sovereign capital led Together AI’s July round; Temasek sits on d-Matrix’s cap table. Nation-states have become the anchor customers — and anchor investors — of the AI infrastructure market.

And yet for all the money, sovereignty remains a slogan in search of a definition — which is why the most useful contribution to the debate this year may be a piece of intellectual hygiene rather than hardware. A framework advanced by technologists at Neo4j Inc., the graph-database company whose knowledge-graph technology increasingly serves as the context layer for enterprise AI agents, cuts the fog with two questions. First: sovereignty of what, and to what end? Three concerns dominate — the ability to carry out AI activities unimpeded by any third party; the security and independence of data at rest and in transit; and where the economic value accrues.

Second: sovereignty for whom? Nation-states, enterprises and individuals have genuinely different needs — a bank in Frankfurt worried about vendor lock-in is not the French state worried about strategic autonomy, and neither is a citizen worried about her data — and conflating them produces policy that serves none. From those questions fall the practical corollaries: interoperability, open standards, open source and a clear-eyed view of which layers of the stack — chips, cloud, models, data, the knowledge layer that gives agents their context — must actually be sovereign, and which can be safely rented.

The framework’s quiet radicalism is the suggestion that the layer everyone ignores may matter most. GPUs are fungible; models are increasingly open; but the knowledge layer — the curated, structured, proprietary context that makes an agent trustworthy, auditable and specific to its owner — is the part of the stack that cannot be imported. A country, or a company, that owns its knowledge graph and rents its GPUs may be more sovereign than one that owns a gigafactory running someone else’s stack. If Europe’s €20 billion buys only hardware, it will have purchased the least defensible layer of the pyramid.

The open-source question shadows all of it. Open-weight models are the natural sovereign stack — inspectable, hostable, unencumbered — and the commercial data now backs the intuition: platforms serving open models report usage tripling year over year, with open-source inference crossing the billion-dollar threshold.

But the finest open weights still descend overwhelmingly from American and Chinese labs, which means “sovereignty via open source” is, for now, independence built on another civilization’s foundations. It is better than dependence on their application programming interfaces. It is not yet autonomy. That gap — between what sovereignty rhetoric promises and what the supply chain permits — is the honest state of the sovereign AI project in 2026.

A country that owns its knowledge graph and rents its GPUs may be more sovereign than one that owns a gigafactory running someone else’s stack.

The sovereign stack: A field guide

A working decomposition of what ‘sovereign AI’ has to cover, and how hard each layer is to localize:

• Energy and land — the binding constraint. Europe’s expensive power and slow permitting are a bigger obstacle than any technology gap.

• Chips — hardest to localize; even “European” silicon designs are fabricated at TSMC. ASML’s investment in Mistral shows where Europe’s real chip leverage lives: the tools.

• Compute/cloud — the current spending focus: EU gigafactories (~€20B), Mistral Compute’s ~18,000 GB300s near Paris.

• Models — increasingly open-weight, but frontier weights still originate largely from U.S. and Chinese labs.

• Data & knowledge layer — the most overlooked and arguably most defensible layer: the context, graphs and institutional knowledge that make agents trustworthy — and that cannot be imported.

• Value accrual — the endgame question: whether the economics of AI activity compound at home or flow to foreign platforms.

Epilogue: The audit

Three questions will grade the era. Does token demand outrun token deflation, so the factories fill and the multiples resolve? Does the agent economy clear its trust threshold — the after-code problem, the auditability problem — before its first spectacular public failure? And does sovereignty mature from procurement program into genuine capability, or calcify into expensive symbolism?

The optimistic case notes that every prior computing buildout that looked like madness — mainframes, PCs, fiber, cloud — was eventually absorbed by demand nobody had modeled. The cautionary case notes that “eventually” bankrupted a lot of pioneers on the way.

What distinguishes this moment from the manias it is compared to is the receipts. The revenue is real, growing at rates enterprise software has never seen. The workloads are real; the tokens are countable. The bet is no longer on whether the technology works. It is on how fast an economy can be rebuilt around the assumption that intelligence is cheap — and on who is left owning the pipes, the factories and the knowledge when the price of thinking falls to the price of electricity.

That audit has already begun. The S-1s will be the exam.

Image: SiliconANGLE

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

- 15M+ viewers of theCUBE videos, powering conversations across AI, cloud, cybersecurity and more

- 11.4k+ theCUBE alumni — Connect with more than 11,400 tech and business leaders shaping the future through a unique trusted-based network.

About SiliconANGLE Media

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.