Howard Dvorkin is a Personal Finance Expert, CPA, Author & Chairman of Debt.com.

Even if you’ve never heard the term “vibe economy,” you probably know what it is. You’re living in it.

Coined by economist Kyla Scanlon, the vibe economy is all about public perception. If we all think the economy is going strong, then dire economic reports don’t matter. We’ll keep spending.

We’ve been enjoying a vibe economy for the past couple of years. While inflation, tariffs and war have confounded even renowned economists, most Americans are still spending. Overspending, in fact.

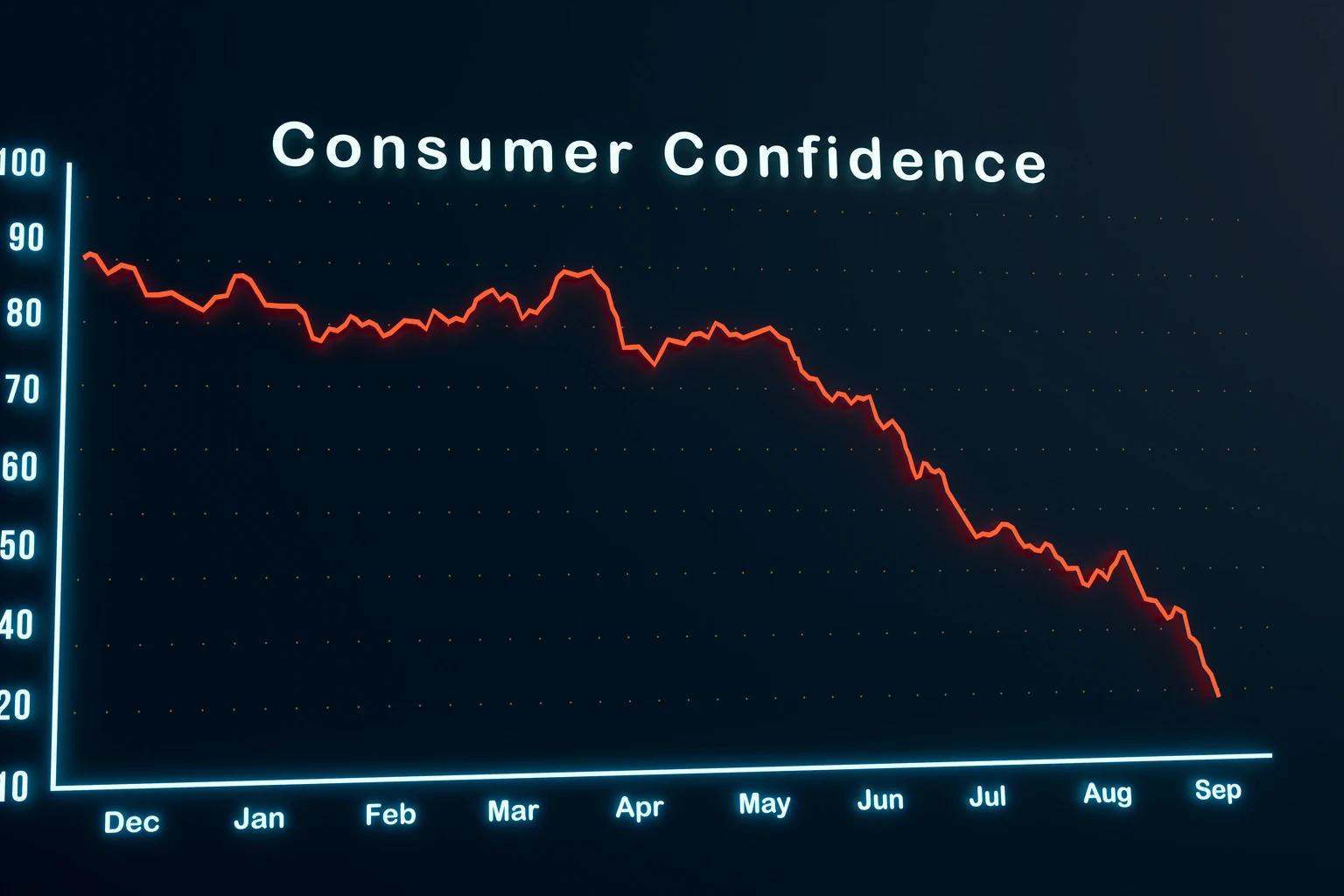

Shaky Economy, Solid Confidence

Here’s the headline of a recent Northwestern Mutual study: “Americans Say They’re Feeling Prosperous, Defying Economic, Market, and Political Pessimism.” The topline result: “More than 8 in 10 Americans say they’re feeling the same or more prosperous than six months ago.”

That might explain why credit card debt is at an all-time high but delinquencies aren’t. In other words, the crash hasn’t happened yet.

The Federal Reserve reports that revolving credit—which is mostly credit cards—grew 3.1% in 2025 and is still rising in 2026, despite the economic uncertainty.

The most logical explanation is that more cardholders need their plastic just to stay afloat. In a survey by my organization, more than half of respondents (55%) said they now use credit cards simply to make ends meet.

Yet that same survey asked how concerned respondents were about their personal debt. Only a quarter were very or extremely concerned. More were only slightly concerned (21%) or not concerned at all (19%).

A few weeks later, a survey by The Harris Poll backed that up. The polling service asked if Americans had postponed anything—including travel, home buying, higher education, marriage or retirement—for financial reasons over the past year.

The perplexing result: 45% reported not putting off anything for financial reasons in the past year, a 6% increase over the same statistic from 2025.

Confidence Lags Reality

If you’re wondering why so many Americans are feeling good about their finances even as the facts indicate otherwise, I have a theory in three parts. I’ve developed it over three decades of launching and operating consumer debt programs.

First, there’s groupthink. I’m reminded of a cartoon I saw decades ago that featured a herd of buffalo about to run over a cliff. From the middle of the herd, one buffalo remarks to another, “Wow, we’re going really fast! We must be heading somewhere awesome!”

In my career, sometimes it’s been difficult to help people who know they have too much debt, but they see all their friends, co-workers and family members continuing to spend. It’s like a mother telling a child, “If everyone else jumped off a bridge, would you, too?” In this case, the answer is often yes.

Second, there’s a time lag. Ever play Jenga? That’s the tabletop game where you set up a wooden tower with 54 wooden blocks, and each player removes one. The tower soon gets wobbly, and eventually, removing one more piece sends the whole thing crashing down.

Our economy often resembles a game of Jenga. It gets wobbly, but we keep removing pieces because, hey, it hasn’t collapsed yet. Perversely, constant media reports of a dire economy can have the opposite effect, because people see and hear all this bad news, and nothing bad has happened yet.

Third, there’s a work ethic. In the United States, we tend to believe in hard work. Unlike in some other countries, in the U.S. your success isn’t determined by your caste, class or royal lineage. The idea is that if you study hard and work hard, you can be successful. Unfortunately, that wonderful attitude can backfire when it comes to personal debt.

Over the past three decades, many clients have told me they refused to seek debt help for months because they honestly believed “If I hustle a little harder, I can get out of this mess.” Today, I see that same attitude being used as an excuse: If the economy indeed goes south, “I can put in more hours and even get a side gig.” That usually admirable trait rarely succeeds against a suffering national economy. It’s akin to jumping from a sinking ship. No matter how well you can swim, the weight of that ship will suck you down and drown you.

The Vapor Economy

In this millennium, recessions have had clear causes. There was the dot-com bubble bursting in 2000, the subprime housing crisis in 2007 and the Covid-19 pandemic in 2020. The next recession will likely be different. It will have many causes.

I lump them all under the term “vapor economy.” Essentially, our finances will be running on fumes. It will likely be a general collapse of many things, from supply chain disruptions caused by war to lingering inflation to tariffs to student loans that no administration has correctly confronted. Connecting it all will be American consumers who listened a little too late.

While we’re living in the vibe economy right now, we still have a chance to avoid a vapor economy.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

Forbes Finance Council is an invitation-only organization for executives in successful accounting, financial planning and wealth management firms. Do I qualify?