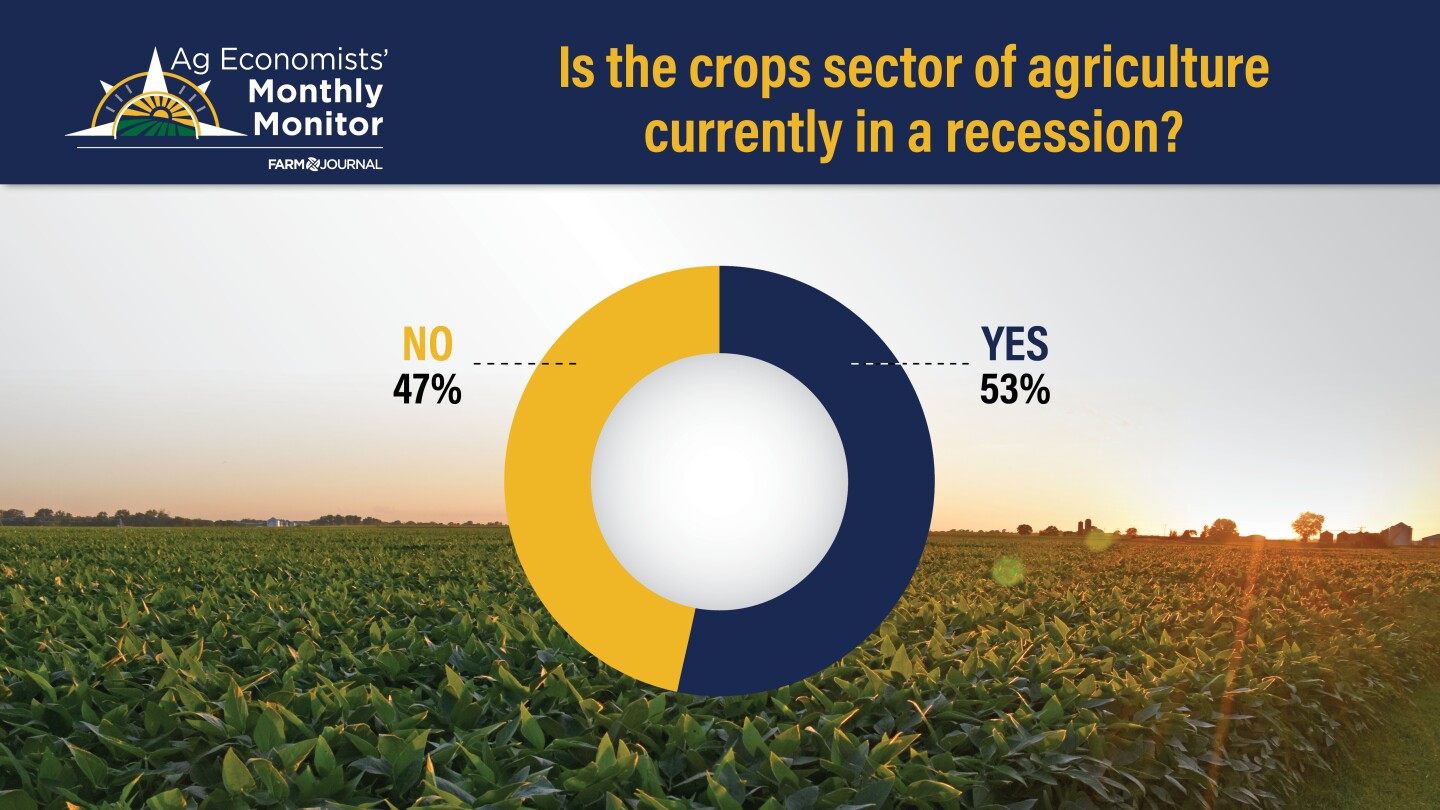

For IT service providers operating in Germany, business has become more complicated. The sector, often spoiled by high growth rates in previous years, is now facing weak business development in the face of a sputtering economy. After a historically weak year in 2024, 2025 brought hardly any growth impulses. Last year, IT service providers in this country achieved an average revenue growth of 2.9 percent organically instead of the hoped-for 7.1 percent. If mergers and acquisitions-related revenues are included, the increase is a bit more favorable at 3.6 percent.

These are the initial findings of this year’s study, “The Market for IT Services in Germany,” by market research firm Lünendonk & Hossenfelder, which will be published at the end of July. The 91 companies analyzed here represent around 65 percent of the total German IT service market with a domestic revenue of almost 34 billion euros.

More Efficiency with AI?

The figures from the extensive market study, which also include results from a survey of user companies, reveal some fundamental changes in the market environment. In addition to a lack of overall economic growth impulses, AI in particular is fundamentally changing the demand for IT services (Figure 1). Thus, 83 percent of the surveyed IT user companies see enormous efficiency potential in software development in the coming years.

(Image: Lünendonk & Hossenfelder)

Furthermore, 70 percent of IT decision-makers expect the same for IT operations and 52 percent for application modernization. All of this has a direct impact on project volumes, fees, and the personnel structure on the provider side. This is consistent with the fact that 54 percent of the IT service providers surveyed plan for a declining demand for software developers by 2028 and 44 percent for less personnel in application management and IT operations. In the future, they intend to invest primarily in technology rather than increasing their staff, as has been common practice.

Declining Workforce for the First Time

The sluggish economy is already affecting employment, as a 10-year comparison of the sector in the study shows. The number of employees of service providers active in Germany has thus declined for the first time by 0.6 percent in the overall view (including international activities), despite a revenue growth of 3.3 percent.

(Image: Lünendonk & Hossenfelder)

Also striking in this year’s survey is that the 25 largest providers in the market segments IT Consulting & System Integration and IT Services grew their business organically last year significantly slower than the overall market, at 1.5 percent and 1.4 percent, respectively. Even including acquisitions, they performed below average with a 2.8 percent increase each.

However, the business and employee development of the leading service providers is extremely heterogeneous. While some achieved double-digit growth rates, others show significant losses. According to Lünendonk analyst Mario Zillmann, this development was primarily due to the industry mix and less to the service portfolio. A rough rule of thumb: those who, like Porsche subsidiary MHP, are mainly active in the hard-hit industrial sectors such as automotive or mechanical engineering, could hardly hope for growth impulses. In contrast, strong demand from the public sector helped companies like Materna achieve considerable growth.

Little Movement in the Ranking

Regardless of this, the two top 25 lists show little change in terms of ranking and providers compared to the previous year’s ranking. The list of companies that generated more than 60 percent of their revenue in Germany with management and IT consulting, system integration, software development, and implementation continues to be led by Accenture, with an estimated German revenue of 3.6 billion euros (2024: 3.4 billion euros). Capgemini follows in second place with 2.24 billion euros (2024: 2.25 billion euros), and IBM in third place with 2.22 billion euros (2024: 2.2 billion euros).

With 1.23 billion euros (2024: 1.07 billion euros), adesso maintains fourth place, ahead of msg systems with 973.7 million euros in revenue (2024: 968.5 million). Adesso shows the second-strongest revenue growth in 2025 with an increase of 15.3 percent. The highest growth was achieved by conet Holding, ranked 15th, with 15.8 percent to 287.1 million euros.

The top two positions in the ranking of IT service providers that generated more than 50 percent of their revenue with IT operations services such as hosting and managed services are, as in the previous year, occupied by T-Systems with 2.95 billion euros (2024: 2.9 billion euros) and NTT Data with 2.10 billion euros (2024: 2.30 billion euros). In third place is newcomer Infosys with 1.30 billion euros (2024: 1.15 billion euros). The focus of the Indian service provider’s activities, which was previously listed in the IT Consulting & System Integration ranking, is now IT operations in the German market. Atos, whose revenue fell by 12.8 percent to 1.25 billion euros, has dropped to fifth place. DXC is ahead of the French service provider with 1.28 billion euros (2024: 1.32 billion euros).

(mack)