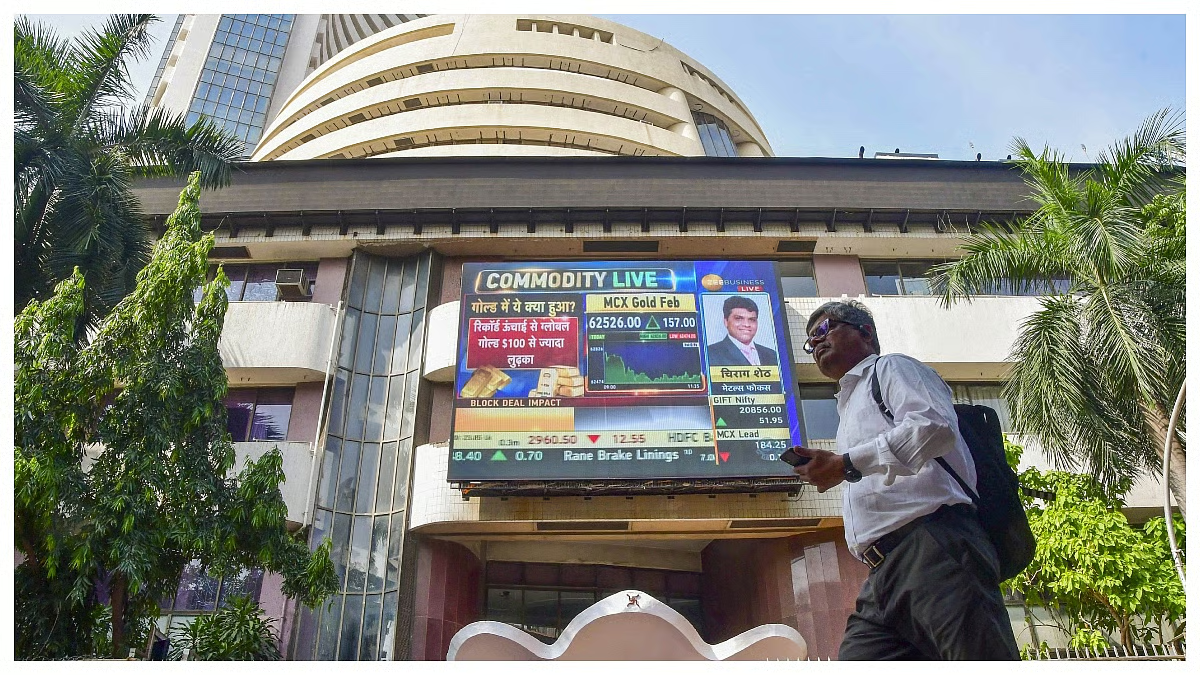

Wall Street’s biggest banks are telling investors to treat Friday’s brutal gold crash as a gift, not a catastrophe. The precious metal plummeted over 11 per cent in a single day after President Trump nominated Kevin Warsh to lead the Federal Reserve — but rather than capitulate, JPMorgan and Deutsche Bank are doubling down with even more bullish forecasts.

Gold futures tumbled from their all-time highs near $5,600 to settle around $4,745 per ounce on 30 January, marking the worst single day for the metal in more than a decade. The trigger was investor relief over Warsh’s appointment: his track record suggests a more hawkish, independent Fed chief, threatening the ‘debasement trade’ that has driven gold’s remarkable 70 per cent surge over the past year.

As dollars strengthened and inflation worries eased, gold lost its inflation hedge appeal — but strategists argue the underlying case for ownership remains rock solid.

Major Banks Signal Buying Opportunity After 11% Crash

Monday brought modest recovery, with gold futures hovering around 0.5 per cent down from their overnight lows. JPMorgan’s Gregory Shearer wasted no time publishing a bullish research note, raising his year-end 2026 target from $5,055 to $6,300 per ounce — a staggering 34 per cent above early Monday prices.

‘Even with the recent near-term volatility, we believe longer-term rally momentum will remain intact,’ Shearer wrote, stressing that demand from central banks and investors continues to outpace supply.

The JPMorgan team points to robust structural tailwinds: central banks purchased roughly 863 tonnes in 2025 despite prices already climbing above $4,000, signalling reserve diversification with ‘further to run.’ Investor demand has accelerated too, with gold ETF holdings rising, physical bar and coin sales surging, and institutional portfolios seeking portfolio insurance against macro and geopolitical risks.

‘Gold remains a dynamic, multi-faceted portfolio hedge and investor demand has continued to come in stronger than our previous expectations,’ Shearer noted.

Deutsche Bank’s Michael Hsueh struck a similarly defiant tone, reiterating his $6,000 per ounce target — signalling roughly 26 per cent upside — whilst arguing the sell-off overshot its fundamental justification. ‘We argue that the adjustment in precious metal prices overshot the significance of its ostensible catalysts.

Moreover, investor intentions in precious have not likely changed for the worse as of yet,’ Hsueh wrote. He highlighted that China‘s investment flows, reflected in Shanghai Gold Exchange premiums, remain positive, underpinning ongoing demand from emerging markets.

Why The Crash Doesn’t Tell The Whole Story

Both banks dismiss the Warsh appointment as a short-term shock rather than a fundamental reordering of precious metals markets. Whilst the Fed’s independence appeared threatened under previous scenarios — a fear that depressed the dollar and turbocharged gold — Warsh’s proven independence during the 2008 financial crisis suggests stability.

His criticism of the Fed’s bond-buying programmes offers a hawkish counterpoint to Trump’s rate-cutting wishes, hinting at institutional preservation rather than politicisation.

The deeper story is macroeconomic: record government debt, geopolitical uncertainty spanning Ukraine to Taiwan, and persistent inflation concerns make gold’s non-correlated, safe-haven properties invaluable.

Central bank diversification away from dollar reserves is structural, not cyclical, suggesting gold’s ‘further to run,’ as Shearer puts it. Even a modest 0.5 per cent reallocation of foreign US asset holdings into gold would drive prices to $6,000, well within reach given the debasement narrative’s staying power.

For retail investors caught off guard by Friday’s carnage, Wall Street’s message is crystalline: this dip is precisely the moment the sophisticated buyers have been awaiting. Supply remains inelastic — gold mining responds slowly to price signals — meaning any sustained recovery in demand will push prices higher swiftly.

With central banks still accumulating and geopolitical risks undiminished, JPMorgan’s $6,300 target and Deutsche Bank’s $6,000 call look more like floor estimates than pie-in-the-sky optimism.