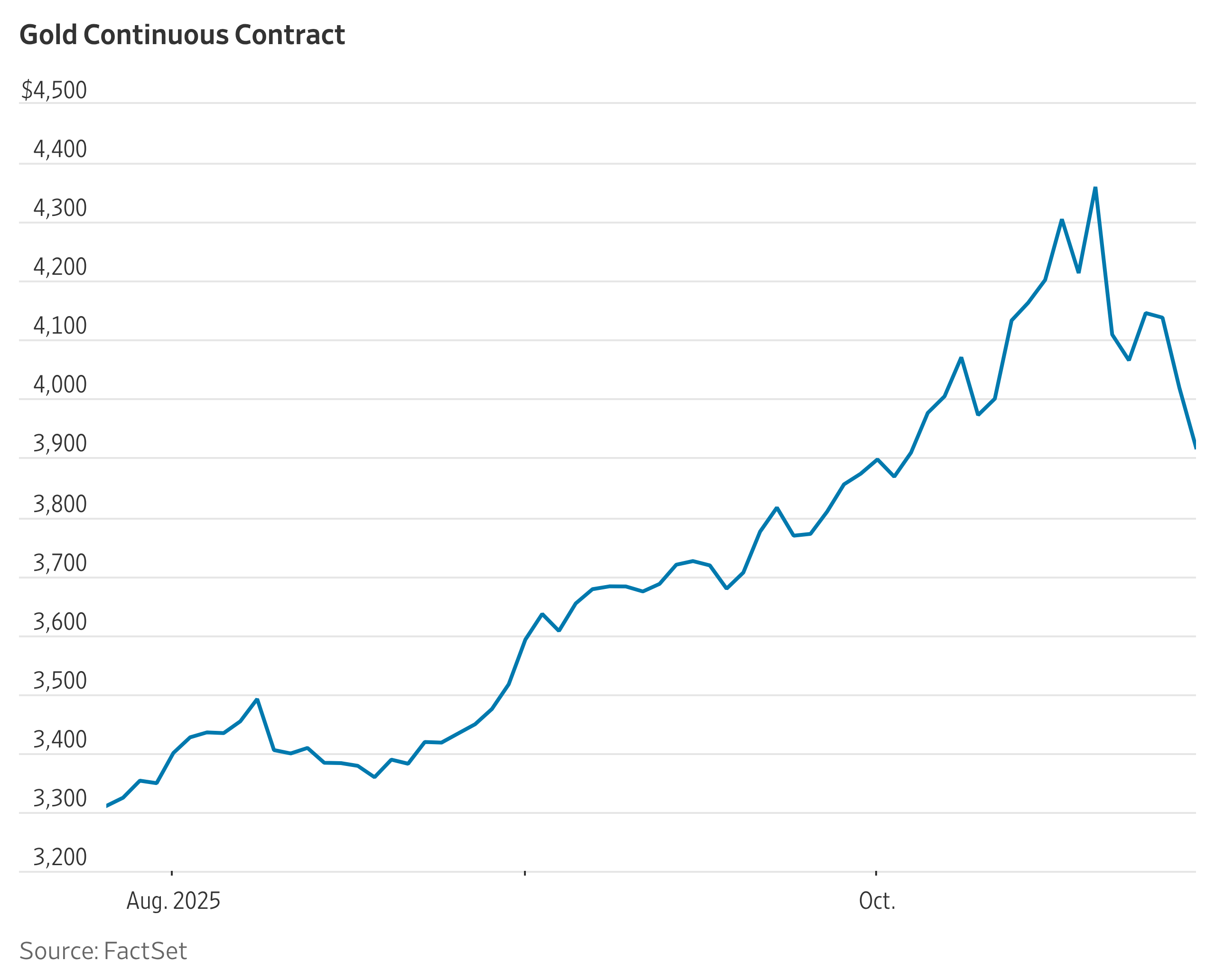

Following the latest hostilities in the US war with Iran, precious metals prices dropped across the board, with the gold price falling back below $4 100/oz and silver below $60/oz.

In its latest ‘Precious Appraisal’, precious metals and technology company Heraeus Precious Metals notes that, along with this, oil rallied, with Brent Crude and the West Texas Intermediate (WTI) topping $80/bbl and $75/bbl, respectively, on July 8, prompting a resurfacing of fears that the conflict could have an impact on price stability and, ultimately, monetary policy.

Since then, oil prices have fallen slightly and precious metals prices have rebounded.

“This is a clear sign that the market expects this flare-up to be similar to others in which a couple of days of strikes and heightened rhetoric ultimately dissipate back into cautious and slow-moving negotiations,” says Heraeus.

Central banks remained net buyers in May, underlining the continued demand for gold despite recent price pullbacks. According to the World Gold Council, central banks bought a net 41 t of gold in May, with the largest accumulation happening in Europe and Asia.

The central banks of Poland and China led the way, buying 18 t and 10 t, respectively.

Heraeus adds that the National Bank of Poland’s reserves now stand at 614 t, meaning it has surpassed the Netherlands as the tenth-largest gold reserve holder in the world and is only 86 t short of its 700 t target.

Uzbekistan and Kazakhstan were also significant accumulators in May, increasing their reserves by 9 t and 7 t, respectively. These purchases come mainly from domestic production allowed for by Kazakhstan and Uzbekistan’s priority rights to buy gold produced in their countries.

Further, Hereaus explains that the People’s Bank of China (PBoC) bought 15 t of gold in June, noting that this was the biggest monthly addition since October 2023 when it bought nearly 22 t. The PBoC now holds 2 346 t of gold, which makes up about 9% of the value of its total reserves.

SILVER

Heraeus notes that the Perth Mint announced silver sales of 294 000 oz in June, down 19% from 364 000 oz in May which was itself the lowest monthly total since April 2012.

June’s sales also marked a 37% year-on-year reduction from the 464 000 oz of silver sold in June 2025.

This came as the silver price dropped 22% in June from $75/oz to $58.50/oz.

Gold bar and coin sales fared better though, with 29 700 oz sold, an increase of 53% from 19 400 oz in May.

Additionally, Heraeus notes that the Sierra Gorda joint venture, owned by Polish copper miner KGHM and diversified miner South32, has approved a fourth grinding line to increase processing capacity by about 25%, from about 48-million tonnes a year to 60-million tonnes a year.

The first production from the expansion is expected in 2030 and full production rates in 2031.

Once completed, the project is projected to incrementally lift silver production to about 1.7-million ounces a year, alongside higher copper, molybdenum and gold output.

KGHM is one of the world’s largest silver producers, with the group having produced 43.3-million ounces of silver in 2025.

Heraeus says KGHM’s new long-term strategy reinforces its position as a major global silver producer, noting that KGHM’s 2055 strategy sets out a record investment programme of more than PLN32-billion through to 2030 which is focused on extending the domestic mining base, modernising infrastructure and developing international assets including Sierra Gorda.

Between 2026 and 2030, the group is targeting average silver production of about 41.5-million ounces a year.

“While this is slightly below KGHM’s 2025 silver output, it shows the company expects to sustain one of the world’s largest silver production profiles while investing in new shafts, processing improvements and longer-term projects,” says Heraeus.

PLATINUM & PALLADIUM

Meanwhile, Heraeus says precious metals prices take time to consolidate their gains after significant rallies, noting that platinum’s remarkable rally that took the price from close to $900/oz in April 2025 to over $2 900/oz in January this year is no exception.

The price is now trading at about $1 600/oz. Heraeus says the price would need to push through resistance at about $1 800/oz to give a hint that the current bounce was not just a countertrend rally.

It explains that there would need to be more strength to confirm it though, with significant resistance centred on $1 900/oz the next test.

Additionally, it notes that registered holdings in platinum exchange-traded funds (ETFs) reduced by 16%, from 3.3-million to 2.76-million ounces, over the first half of this year.

The year-to-date high on January 27 of 3.38-million ounces occurred close to the highest year-to-date price of about $2 920/oz, intraday on January 26.

Heraeus explains that platinum ETF holdings were largely consistent in January and February, experiencing inflows during the strong January price rally which dissipated afterwards.

The real decline began in early March, coinciding with the beginning of the US-Iran conflict. Since then, it notes that platinum ETF holdings have reduced by an estimated 500 000 oz and have shown no sustained inflows even during rallies in the platinum price since March.

Stocks in NYMEX vaults have also shrunk this year, falling more than 240 000 oz. This has also resulted in lease rates falling back to more normal levels.

Further, Heraeus also notes that palladium ETFs show consistent drawdowns in the first half of this year.

Registered holdings in palladium ETFs reduced by 15%, from 1.16-million ounces to 990 000 oz, over the first half of this year. The year-to-date high on February 6 of 1.23-million ounces occurred about a week after the highest year-to-date price of about $2 160/oz, intraday on January 26.

Similarly to platinum, palladium ETF holdings were largely consistent in January and February.

Heraeus explains that rises in the palladium price were mirrored with increases in ETF holdings and falls in price were met with outflows. Most of the reduction in palladium ETF holdings happened in March, during the first month of the US-Iran conflict.

During March, over 140 000 oz of palladium left ETFs, accounting for nearly 85% of the total year-to-date drawdown. Since then, palladium ETF holdings have continued to decline slowly.

Unlike platinum, NYMEX vault holdings of palladium are up this year, by 23 000 oz, although they did slip by 14 000 oz in the second quarter.

The company adds that battery electric vehicle (BEV) sales in Europe surged in June following the jump in gasoline prices caused by the war with Iran and the closure of the Strait of Hormuz.

Additionally, Heraeus says initial sales reports for June show BEV sales in Germany and France jumping to a 28% and 30% share of total new car sales respectively, the highest levels yet seen for both countries.

In the first half of the year, overall car sales have gone up in both countries so combustion engine vehicle sales are declining slowly, which is gradually eroding automotive palladium demand.

Heraeus explains that there are regional differences as BEV sales in the US and China are down year-on-year (so far), but those in Europe and the rest of the world (RoW) are up, which can be partly explained by the surge in exports by Chinese automakers as they struggle with lacklustre demand in their domestic market.

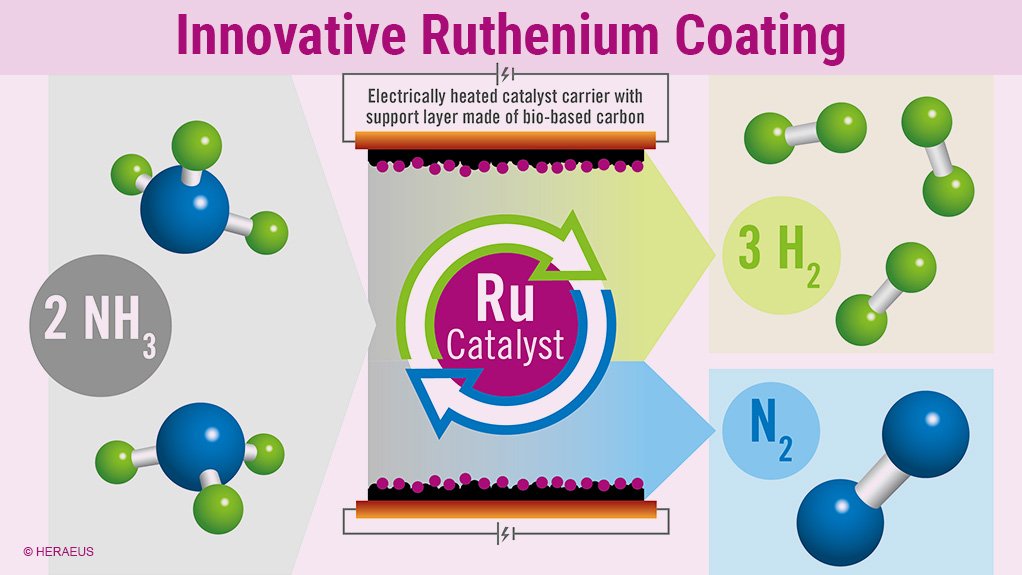

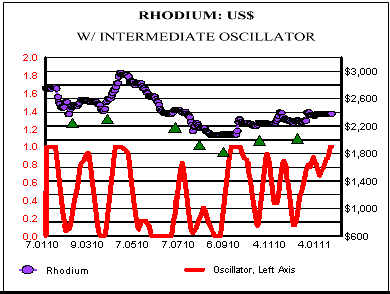

RHODIUM, RUTHENIUM & IRIDIUM

Moreover, Heraeus notes that Australia’s largest renewable hydrogen project is moving into execution, having successfully reached the final investment decision. Plug Power will be supplying the 50 MW Hunter Valley Hydrogen Hub project in New South Wales, Australia, with proton exchange membrane (PEM) electrolysers.

The Hunter Valley project will use renewable electricity to produce renewable hydrogen through PEM electrolysis, progressively replacing natural gas in the production of low-carbon ammonia and ammonium nitrate at Orica’s existing ammonia manufacturing facility.

The facility is expected to produce about 4 700 t/y of renewable hydrogen once at full capacity. The prices of all three small platinum group metals – rhodium, ruthenium and iridium – advanced last week following the announcement.