The case for holding silver as an inflation hedge gets made so often, by so many sources, that most investors absorb the proposition without examining it carefully. The metal preserves purchasing power. The metal is real, unlike paper currency. The metal protects against the slow erosion that fiat systems produce. These statements appear in marketing material from dealers, commentary from precious metals analysts, and casual conversation among stackers. What is harder to find is a careful look at whether the historical data actually supports the claim, and what conditions have to hold for silver to behave the way the inflation-hedge narrative promises. Reading the price of silver, whether on a dealer chart such as SD Bullion’s or on any historical data series, against inflation data across five decades produces a more nuanced picture than the marketing version, and the nuances matter for any investor making allocation decisions based on inflation concerns.

The 1970s as the strongest case for the inflation hedge narrative

The decade most commonly cited in support of silver as an inflation hedge is the 1970s, when US inflation ran above ten percent at multiple points and silver delivered returns that dramatically exceeded the CPI’s cumulative move. Silver started the decade around $1.80 an ounce and ended it near $30 after the Hunt brothers’ famous run-up, producing real returns that no broad equity or fixed income strategy came close to matching. This experience embedded the inflation-hedge story in the collective memory of precious metals communities, and it remains the strongest empirical case available for the proposition. The relevant question is whether the 1970s experience was a reliable template for what silver does during inflationary periods, or whether it was the product of a specific combination of conditions that have not recurred in subsequent decades.

The 1980s and 1990s as the counter-example

After the dramatic 1980 peak, silver entered a long decline that persisted through most of the 1980s and 1990s. Inflation during this period ranged from moderate to low, but the metal’s performance suggests that silver responds to disinflation more aggressively than to the absence of inflation. By the late 1990s silver had fallen to under $5 an ounce, having lost the bulk of its 1970s gains in nominal terms and considerably more in real terms. An investor who bought silver at the 1980 peak believing in the inflation-hedge story spent the next two decades watching the metal lose ground regardless of what happened to consumer prices. This period is rarely invoked by sources promoting the hedge narrative, but it is essential to any honest assessment of when the narrative holds and when it fails.

The 2000s rally and its mixed lessons

The 2000s produced another silver bull market, with the metal rising from under $5 in 2001 to nearly $50 by 2011. The period included both inflationary phases (the late 2000s commodity boom, the post-2008 monetary expansion) and disinflationary phases (the 2008 to 2009 deflationary scare). Silver moved aggressively in both directions across these phases, rising during the early period of monetary easing, falling sharply during the 2008 financial crisis when deflation fears dominated, and then rallying again during the subsequent quantitative easing era. The pattern suggests that silver responds to monetary policy expectations and to inflation expectations, but not always in the simple direct way that the inflation-hedge story implies. The metal can fall during periods of rising actual inflation if disinflation expectations are dominant, and it can rise during periods of low actual inflation if inflation expectations are increasing.

The post-2011 stagnation despite persistent monetary concerns

From 2011 through roughly 2020, silver moved sideways or downward despite continued monetary expansion, persistent low real interest rates, and recurring inflation concerns that briefly flared and then subsided. An investor who held silver through this decade as an inflation hedge experienced returns that lagged most major asset classes, including assets traditionally considered poor inflation hedges. The post-2011 period demonstrates that silver’s responsiveness to inflation depends heavily on whether inflation is actually manifesting in measured price data versus existing only as a concern that does not show up in CPI prints. Silver responds more reliably to realized inflation than to feared inflation, which limits its usefulness as a forward-looking hedge during periods when feared inflation does not arrive.

Federal Reserve research and academic literature on commodity returns during inflationary periods document these patterns in considerable detail, and the literature generally treats the inflation-hedge claim with more scepticism than the popular precious metals commentary suggests.

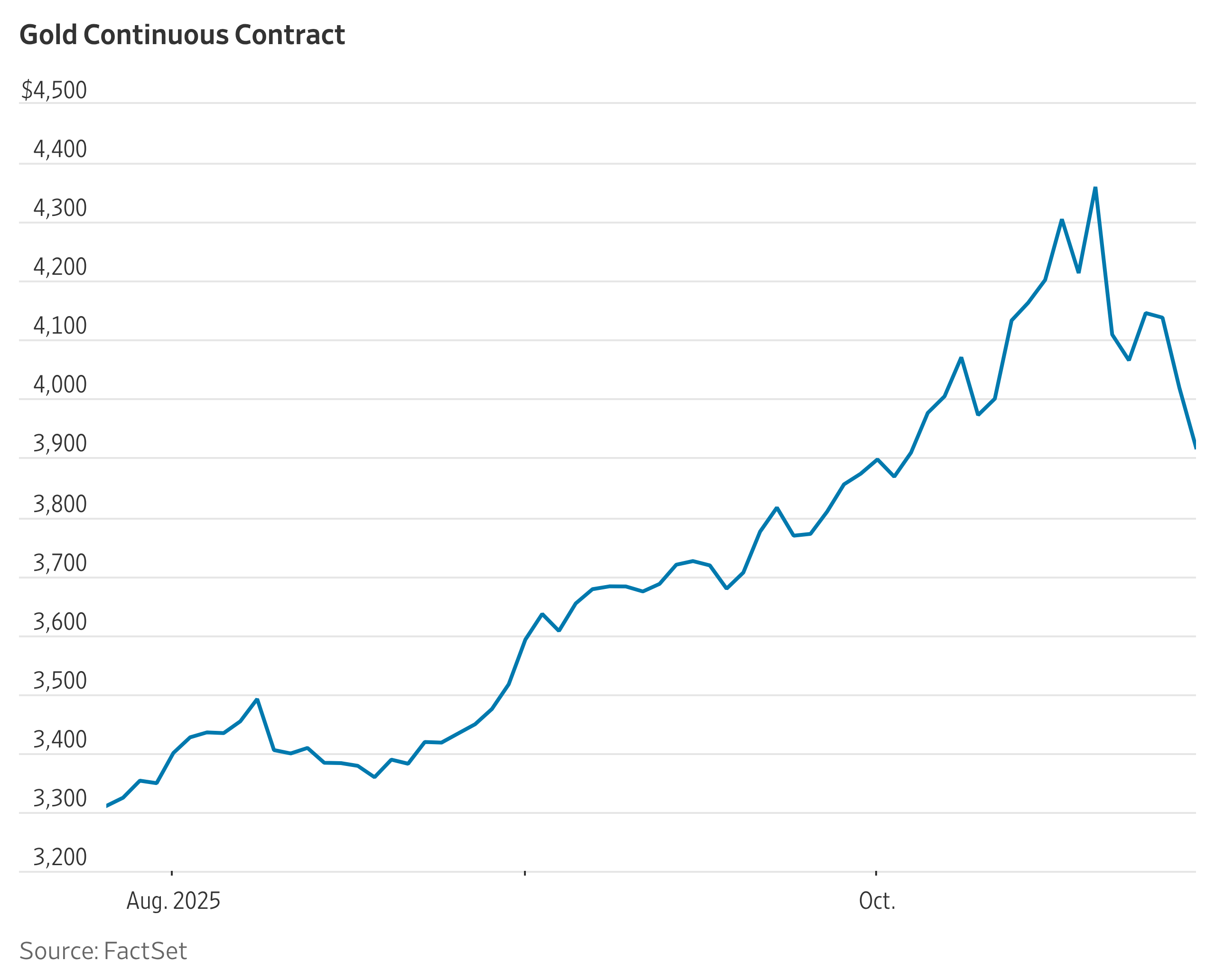

The 2020 to 2026 period and its specific configuration

The most recent period of inflation, with US CPI peaking near nine percent in 2022, produced a silver response that was meaningfully positive but not as dramatic as the inflation-hedge narrative might have predicted. The metal rallied from the low twenty-dollar range during the inflation peak to its eventual highs above one hundred dollars in early 2026, a substantial real-return performance over the period. But the rally also depended heavily on the structural industrial demand story that was developing in parallel, and the metal’s response to inflation alone (separating out the industrial demand component) was harder to isolate. Investors who held silver specifically as an inflation hedge during this period earned returns that vindicated the position, but the attribution between inflation response and industrial demand response is not as clean as the simple hedge narrative implies.

What the gold comparison reveals

A useful test of the inflation-hedge claim is comparison with gold, which carries a similar narrative but with a longer track record. Across most inflationary periods over the past five decades, gold has tracked inflation more reliably than silver, with smaller drawdowns during disinflationary phases and steadier appreciation during sustained inflationary regimes. Silver has occasionally outperformed gold during inflation spikes but has consistently underperformed during inflation reversals. The pattern suggests that silver is the more aggressive inflation play, capturing larger upside during favourable periods but also exposing the holder to larger losses when conditions shift. For an investor whose primary concern is inflation hedging rather than upside capture, gold provides a more reliable expression of the thesis than silver does.

The real rate connection that matters more than CPI

Empirical analysis of precious metals returns consistently finds that the strongest correlation is not with inflation itself but with real interest rates, defined as nominal yields minus inflation expectations. Silver and gold both perform best during periods of negative real rates and worst during periods of positive real rates, regardless of where nominal inflation sits. This relationship explains many of the apparent inconsistencies in the simpler inflation-hedge story. Silver did poorly during the 1980s and 1990s because Volcker’s high nominal rates produced strongly positive real rates even as inflation moderated. Silver did well in the post-2008 period and the post-2020 period because aggressive monetary policy produced negative real rates even as actual inflation moved in various directions. Investors thinking about silver as a hedge would benefit from focusing on real rates rather than headline CPI, which provides a more reliable indicator of when the metal is positioned to perform.

A more honest framing

Silver is not a pure inflation hedge in the simple sense that the popular narrative suggests. It responds to a combination of factors including realized inflation, inflation expectations, real interest rates, monetary policy trajectories, and industrial demand conditions. During periods when most of these factors align in supportive directions, silver delivers strong returns that more than compensate for measured inflation. During periods when the factors diverge or move against the metal, silver can underperform inflation for years at a stretch. An investor who holds silver expecting a reliable annual offset against CPI will be disappointed; an investor who holds it as part of a diversified position that responds to a broader set of monetary and economic conditions has a more defensible thesis. The metal earns its place in many portfolios on those broader grounds, but the simple inflation-hedge story deserves to be treated as a partial truth rather than a complete one.

Related reading on our site: the relationship between real interest rates and precious metals, comparing gold and silver as inflation hedges across decades, and what 1970s monetary history actually teaches about the present.

The above information does not constitute any form of advice or recommendation by London Loves Business and is not intended to be relied upon by users in making (or refraining from making) any finance decisions. Appropriate independent advice should be obtained before making any such decision. London Loves Business bears no responsibility for any gains or losses.