The Big Development

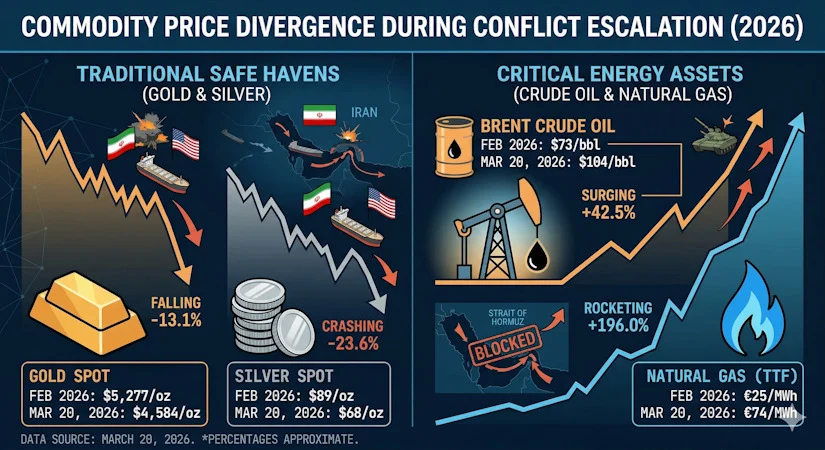

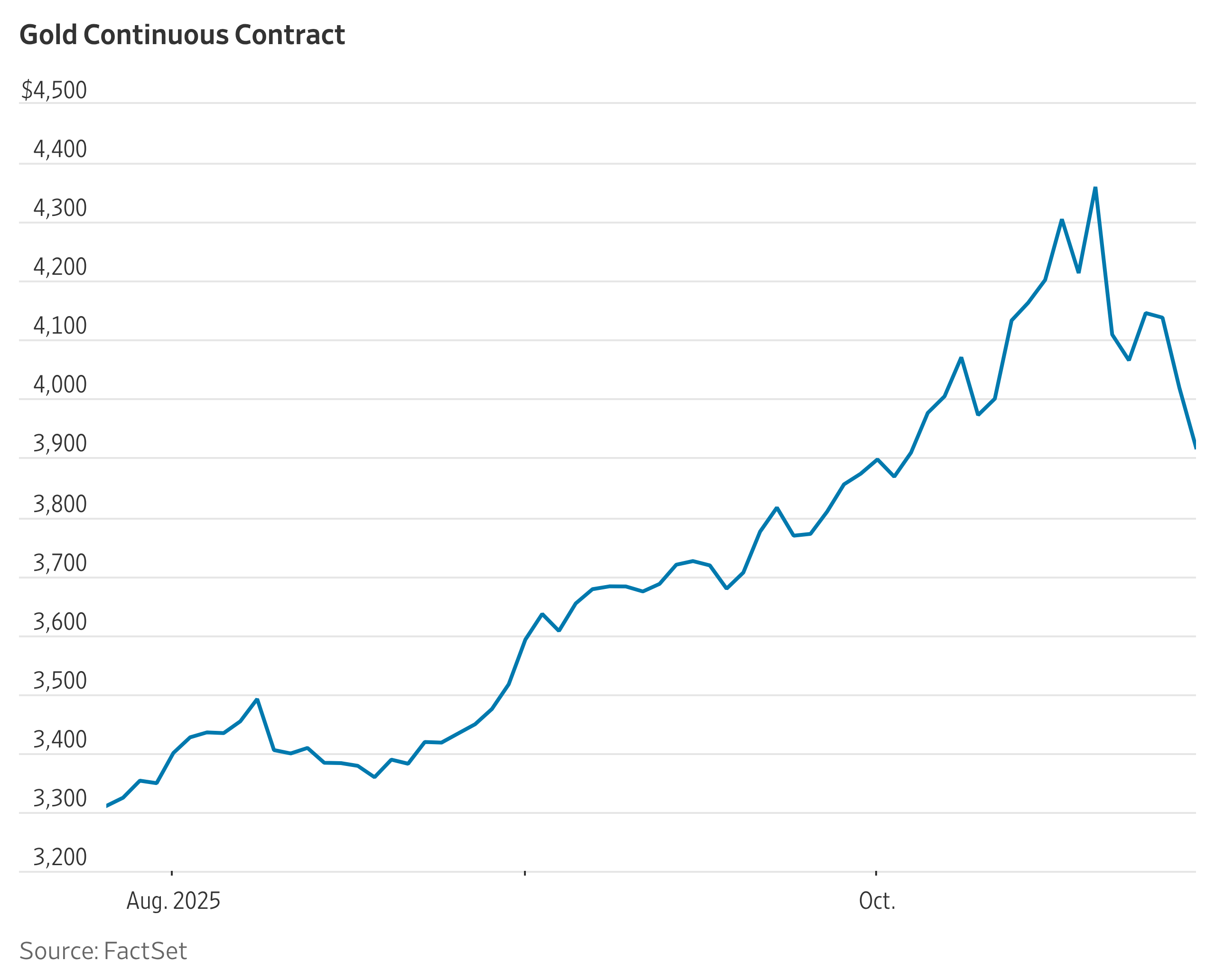

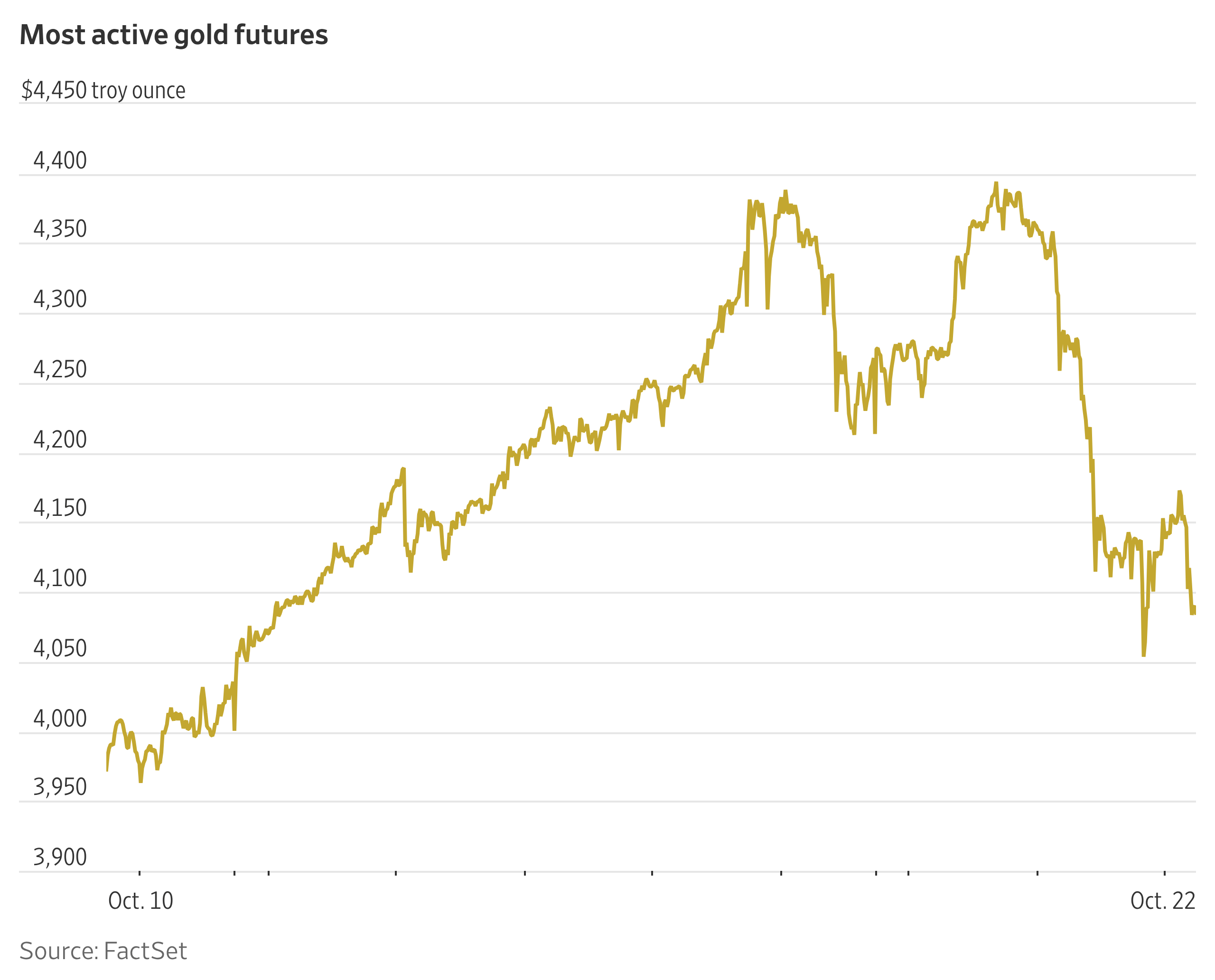

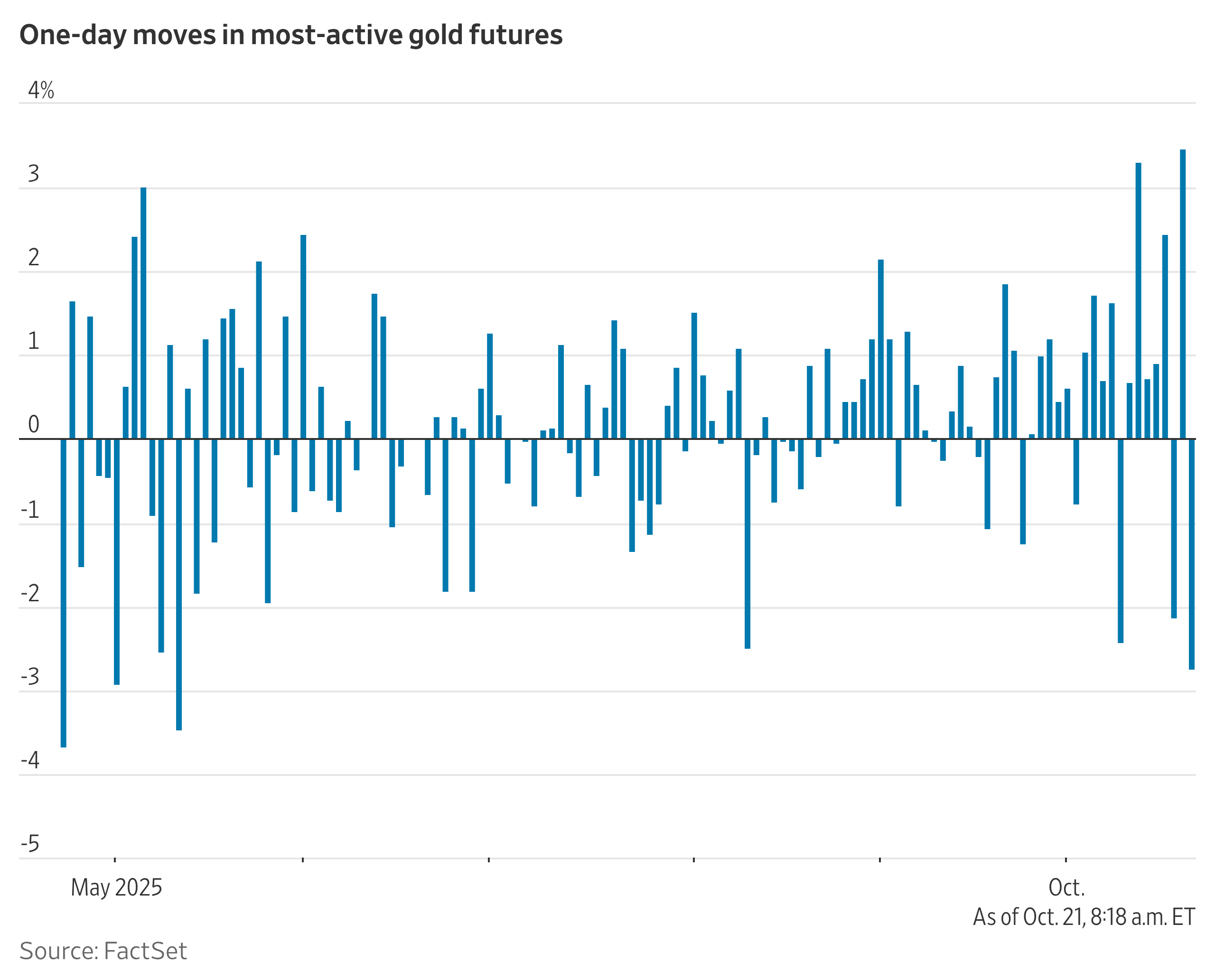

Gold is supposed to shine when the world looks unsettled; instead, it’s suddenly losing its luster at the very moment geopolitical risk is rising. Spot prices have tumbled roughly 4% to about $4,650 an ounce after an intraday plunge of as much as 7%, marking one of the sharpest single-day reversals in years even as the war in Iran continues to roil energy markets. For investors who had grown accustomed to gold’s relentless climb, the speed and scale of the sell-off feel less like a routine correction and more like a stress test of the metal’s safe-haven status.

The immediate trigger sits squarely in Washington, not in the Middle East. After holding rates steady, Federal Reserve Chair Jerome Powell openly acknowledged that surging oil prices could rekindle inflation and confirmed that the possibility of another rate hike had been discussed inside the policy committee. That subtle but unmistakable hawkish shift sent equity markets lower, pushed bond yields higher, and hit precious metals hard as traders repriced the path of U.S. monetary policy.

In this environment, investors are being forced to reassess a core assumption: that gold can rally indefinitely on geopolitical fear alone. A Fed that is willing to keep real rates elevated—or even raise them—changes the calculus for capital allocation, particularly for sophisticated investors sitting on large, leveraged gains in the metal. That’s where the real shift begins.

Why This Moment Matters

This inflection point for gold arrives at a paradoxical time. On one hand, the macro backdrop seems tailor‑made for safe-haven assets: a grinding conflict in Iran, oil prices pushing higher, and a global economy still adjusting to years of inflation and tightening. On the other hand, the Fed’s concern that higher energy costs could entrench inflation means rate cuts are no longer a given, and the door to further tightening has been nudged open.

That combination is toxic for non‑yielding assets. Rising or higher-for-longer policy rates increase the opportunity cost of holding gold, especially relative to U.S. Treasuries that now offer meaningfully positive real yields. As yields climb, the dollar tends to strengthen, further pressuring dollar‑denominated gold prices and amplifying the downside for international investors. The result is a market where fear is no longer enough to guarantee upside for traditional hedges.

For executives, asset managers, and family offices, this moment underscores a broader truth: safe havens are not static. Their performance is highly sensitive to the interplay of central bank policy, real yields, and investor positioning—not just headline risk.

“The assets that protected portfolios yesterday may be the ones forcing the hardest decisions today.”

The Strategy Behind the Move

The sell-off is not just about macro headlines; it is also about strategy. After a year in which gold surged to a string of record highs and remains roughly 60% higher over the past 12 months, many investors are simply sitting on substantial gains. When a crowded trade meets a policy shock, profit‑taking is almost inevitable.

Several strategic forces appear to be converging:

- Rebalancing after outsized gains: Institutional and private investors who rode the rally are locking in profits, particularly those with strict risk budgets or volatility limits.

- Rotation into yielding assets: As yields rise, capital naturally migrates toward bonds and cash-like instruments offering attractive, low‑risk income.

- Currency positioning: With the dollar strengthening on expectations of a more hawkish Fed, some investors—particularly in the Middle East—may be selling gold to rebuild dollar exposure, even though both are traditionally seen as safe havens.

From a portfolio‑construction standpoint, the decision is rational. Gold, which yields nothing, competes with instruments that not only offer income but also benefit directly from tighter policy. In that world, even long‑term gold bulls may choose to trim exposure tactically.

Market and Economic Impact

The repricing in gold is already rippling through listed markets. Major mining names such as Newmont and Freeport-McMoRan have been among the weakest performers in the S&P 500, while the VanEck Gold Miners ETF has dropped around 7% in a single session. For producers whose margins are highly sensitive to spot prices and whose valuations had baked in a sustained high‑price regime, this is a painful reset.

Beyond equity screens, the macro signalling is just as important:

- A sustained drop in gold may temper perceived wealth effects in markets where physical holdings are significant, from Asia to the Middle East.

- Central banks, which have been major buyers of bullion in recent years, will be closely watched for any sign that they are moderating purchases—or viewing this as an attractive dip to add reserves.

- Higher real yields and a firmer dollar can tighten financial conditions globally, affecting emerging‑market funding costs and cross‑border capital flows.

In other words, gold’s correction is not just a story for commodity desks. It is another data point in a broader tightening of global financial conditions that executives and policymakers ignore at their peril.

The Industry Ripple Effect

The sell-off is quickly reshaping behavior across the broader precious-metals ecosystem. Exchange‑traded products are seeing notable outflows, with the SPDR Gold Shares ETF, the world’s largest gold fund, experiencing multi‑million‑dollar redemptions within hours of the market open—on track for its heaviest net selling day since late February. That kind of flow is both symptom and accelerant: redemptions pressure prices, which in turn trigger more selling from momentum‑sensitive strategies.

For competitors and adjacent sectors, several dynamics stand out:

- Silver and other precious metals tend to move directionally with gold, meaning volatility in one can spill quickly into others.

- Mining‑equipment suppliers and service providers may see capital‑expenditure plans postponed or resized if miners reassess the durability of high price decks.

- Alternative gold strategies—funds combining bullion with miners or using derivatives overlays—may gain traction among investors who still want exposure but prefer more actively managed risk.

This is how a price move becomes an industry moment: behaviors change, capital is redirected, and business plans are rewritten.

Risks and Challenges Ahead

Even for those inclined to buy the dip, the road ahead is hardly straightforward. A more hawkish Fed is only one facet of a complex risk matrix that gold investors must navigate.

Key challenges include:

- Policy uncertainty: If inflation remains sticky due to high oil prices, the Fed could raise rates rather than cut them, extending pressure on non‑yielding assets.

- Geopolitical fog: The Iran conflict and its impact on energy markets could either deepen or de‑escalate, with very different implications for both growth and inflation.

- Market technicals: After a parabolic run, positioning and leverage in the gold complex may still be elevated, leaving the market vulnerable to additional forced selling.

For corporate treasurers, wealth managers, and CIOs, the immediate challenge is less about calling the exact bottom than about avoiding pro‑cyclical decisions driven purely by fear or FOMO.

What Happens Next

The next phase for gold will hinge on three interlocking variables: the path of inflation, the Fed’s reaction function, and the trajectory of the Iran conflict. If oil‑driven inflation forces the Fed to keep rates elevated—or even raise them—the headwinds for gold could persist despite any intermittent safe‑haven bids. Conversely, a credible path back toward easing, especially if growth slows, could revive the metal’s appeal quickly.

Executives and investors should watch:

- Fed communications: Any shift in tone around inflation risks, growth concerns, or balance‑sheet policy.

- Real yields: The interplay between nominal yields and inflation expectations, which strongly influences gold valuations.

- ETF and futures positioning: Whether current outflows deepen into a broader liquidation or stabilize as tactical selling exhausts itself.

If history is a guide, the turn—when it comes—will likely be fast and uncomfortable for those on the wrong side of the trade.

The Bigger Business Trend

Step back from the day‑to‑day volatility and a larger pattern comes into focus. The gold sell‑off is one chapter in a wider story: the repricing of risk assets after a multi‑year regime of ultra‑low rates, aggressive liquidity, and repeated geopolitical shocks. Today, central banks are less willing to underwrite markets, and investors are relearning how to live with genuine two‑way risk in both bonds and commodities.

This has several implications for the global business landscape:

- Supply chain hedging is evolving: Companies no longer rely on a single “safe asset” hedge but use more granular strategies across currencies, commodities, and regions.

- Wealth portfolios are becoming more barbell‑shaped: Combining high‑conviction risk assets with genuinely defensive, income‑generating holdings rather than simply adding gold and hoping for the best.

- Economic power is tilting toward policy‑makers who control both rates and resources: The intersection of energy security, monetary policy, and capital flows is more consequential than any single asset’s price.

For CEOWORLD’s audience, the message is clear: gold’s stumble is not an isolated anomaly; it is a signal that the rules of the post‑pandemic financial order are still being written.

Key Takeaways

- Gold has suffered a sharp, roughly double‑digit pullback from recent highs, even as the Iran war and oil prices keep geopolitical risk elevated.

- A more hawkish‑leaning Fed, higher bond yields, and a stronger dollar are undermining the appeal of non‑yielding assets like gold.

- Profit‑taking and tactical rebalancing after a 60% 12‑month rally are amplifying volatility, particularly in gold‑linked ETFs and mining stocks.

- Retail and smaller institutional investors are starting to capitulate, while contrarian signals—from sentiment to positioning—are emerging for long‑term buyers.

- The episode fits into a broader trend of markets adjusting to higher‑for‑longer rates, more volatile inflation, and a less predictable safe‑haven hierarchy.

Frequently Asked Questions

1. Why has the gold price dropped so sharply?

Because the Fed signaled greater concern about inflation risks from higher oil prices and openly discussed the possibility of rate hikes, investors rotated toward yielding assets and took profits after a strong rally.

2. How big is the recent decline in gold?

Gold has fallen about 4% to around $4,650 an ounce after an intraday drop of up to 7%, leaving it roughly 11% below levels seen when the Iran conflict intensified.

3. Is gold still up over the past year?

Yes. Despite the recent correction, gold remains about 60% higher over the last 12 months and is still comfortably above its 200‑day moving average.

4. What role is the Iran war playing in all this?

The war has pushed oil prices higher, creating upside risk to inflation and forcing the Fed to keep policy tight, which ironically undermines gold even as geopolitical risk rises.

5. Why are investors selling gold ETFs like GLD?

Higher yields and a stronger dollar make gold less attractive, prompting redemptions; GLD has seen multi‑million‑dollar outflows in early trading, with the day set to rival prior heavy selling sessions.

6. Are gold mining stocks affected more than bullion?

Yes. Mining shares and sector ETFs such as GDX have dropped around 7% in a single session, reflecting their operating leverage to spot prices and more volatile equity‑market dynamics.

7. Does rising pessimism around gold mean it’s a buy?

Elevated pessimism can be a bullish contrarian signal, especially when long‑term fundamentals remain intact, but timing is tricky and investors must account for policy and geopolitical uncertainty.

8. How should long‑term investors think about gold now?

As part of a broader diversification and risk‑management toolkit rather than a one‑stop safe haven, with sizing and entry points calibrated to the reality of higher‑for‑longer rates and more volatile inflation.

9. What should corporate leaders and CIOs watch next?

Fed guidance, real‑yield dynamics, ETF and futures positioning, and any sign that central banks adjust their gold‑buying behavior will all shape the next leg of the market.

10. Could gold see another leg down from here?

If inflation remains sticky, oil stays elevated, and the Fed leans further toward additional tightening, the metal could face more pressure before any durable base forms—but that is precisely the environment in which long‑term capital quietly starts to position for the next cycle.

Have you read?

Graceful Power: 3 Self-Aware Habits for 2026 Leaders.

The Teammate Multiplier: Why 2026 Valuing Talent Differently.

The Complexity Gap: Are You Outgrowing Your Capacity?

From Stage to Spreadsheet: The CEO Revolutionizing Finance.

4 Leadership Cracks in the Multigenerational Workplace.