If you don’t work in the precious metals industry you may not even have heard of it.

But over the last couple of years rhodium has been just about the worst-performing commodity.

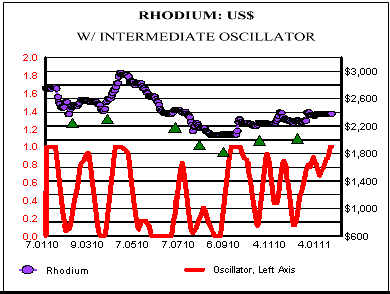

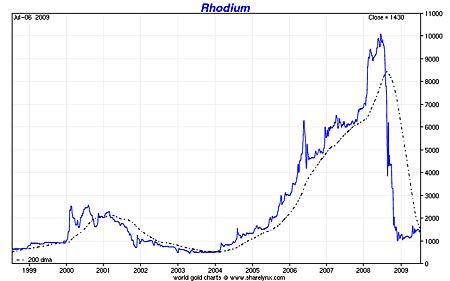

Last year the price of the precious metal tumbled 42 per cent. Since a peak of more than $10,100 an ounce in 2008, it has fallen 87 per cent, this week trading at $1,360.

The collapse in rhodium prices is heaping additional pressure on the beleaguered South African platinum mining industry. At the platinum industry’s annual gathering in London this week, the mining executives – usually an optimistic and cheerful bunch – were notable for their glumness.

The story of rhodium is a classic of a market responding to high prices. After prices rose 20-fold between 2003 and 2008, rhodium consumers – especially the car industry, which uses the metal in catalytic converters – aggressively sought alternatives.

The result, according to Johnson Matthey, the refiner that produces benchmark data on the platinum group metals markets, is that rhodium supply outstripped demand by 139,000 ounces – or a fifth of overall supplies – last year. Annual demand from the auto industry has fallen by a fifth, or 175,000 ounces, since 2007.

Johnson Matthey sees little change for the rhodium market this year.

That is grim news for miners. The challenges of the South African platinum mining industry are well documented. Energy and labour costs are rising, as is nationalism.

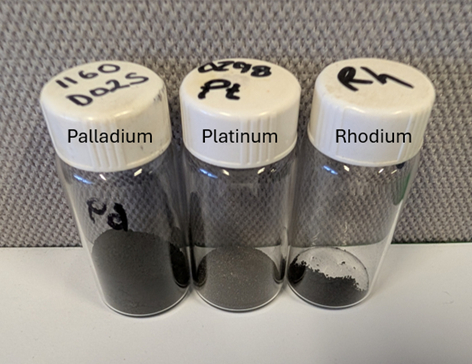

While rhodium production is tiny – global output is about 25 tonnes (800,000 ounces) a year, compared with 200 tonnes each for platinum and palladium, the other “platinum group metals” – it has for years helped miners such as Anglo American, Impala, Lonmin and Aquarius keep their heads above water.

For example, in 2008, rhodium accounted for 27 per cent of Impala’s revenues (though it was only 7 per cent of PGM production by volume). In 2010 that fell to 14 per cent. At current prices, rhodium would account for just 8 per cent.

When miners are making investment decisions, particularly in the UG2 area of South Africa’s Bushveld complex (an increasingly important source of supplies) “rhodium tends to provide the super-profits element”, says Ian Farmer, chief executive of Lonmin.

Indeed, most in the industry model long-term rhodium prices at $2,500-$3,000 an ounce, double today’s prices.

Could the price collapse save the rhodium market, stimulating fresh demand? “Current market values for rhodium should make the metal more attractive to commercial users than it has probably been for several years, possibly limiting price declines from present levels,” says A-1, the world’s top recycler of PGMs.

But others are more sceptical. Some purchasing managers are still smarting after hedging rhodium prices near the top of the market five years ago.

The mining industry may have to come up with its own solutions to its problems: (whisper it softly) production cuts.