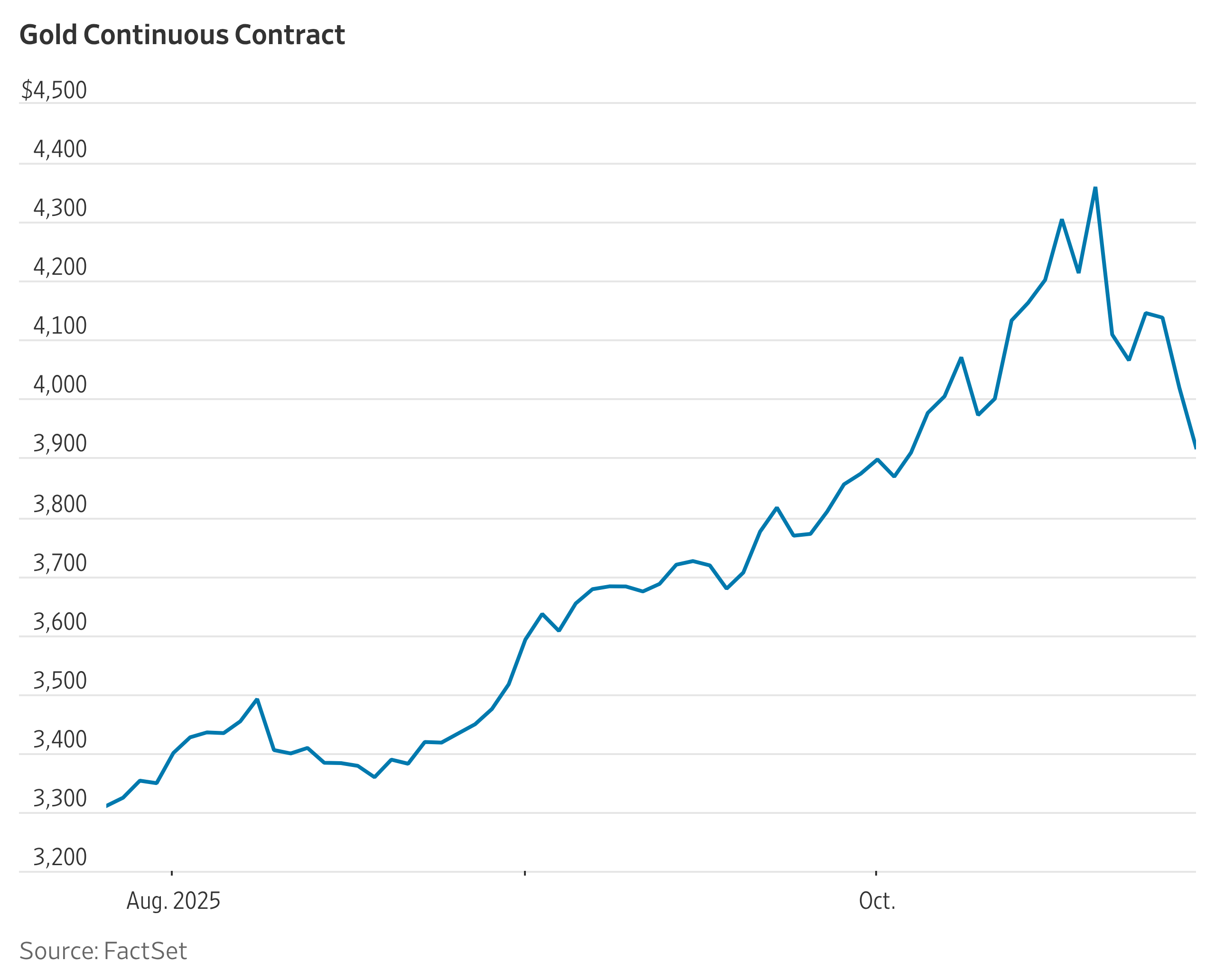

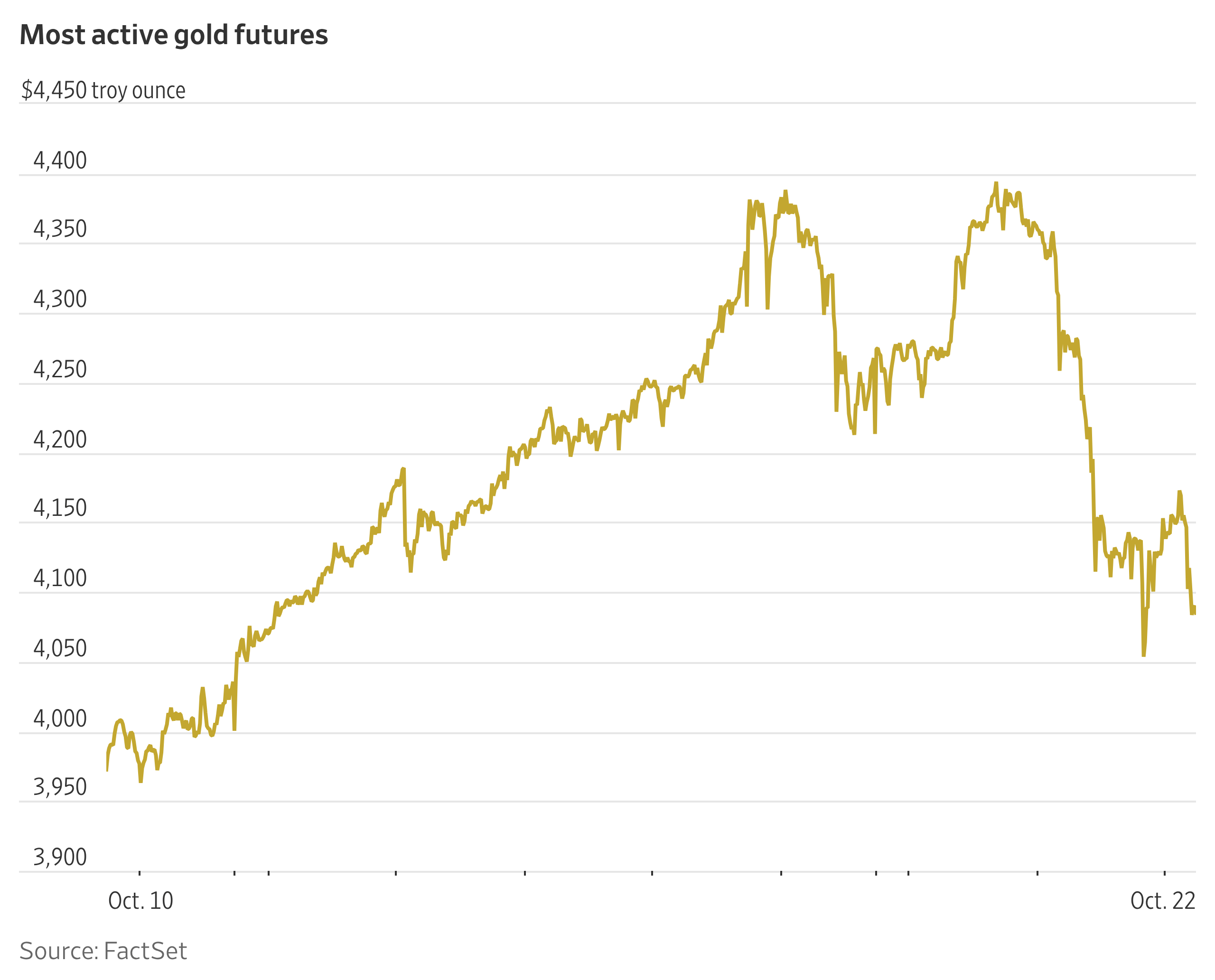

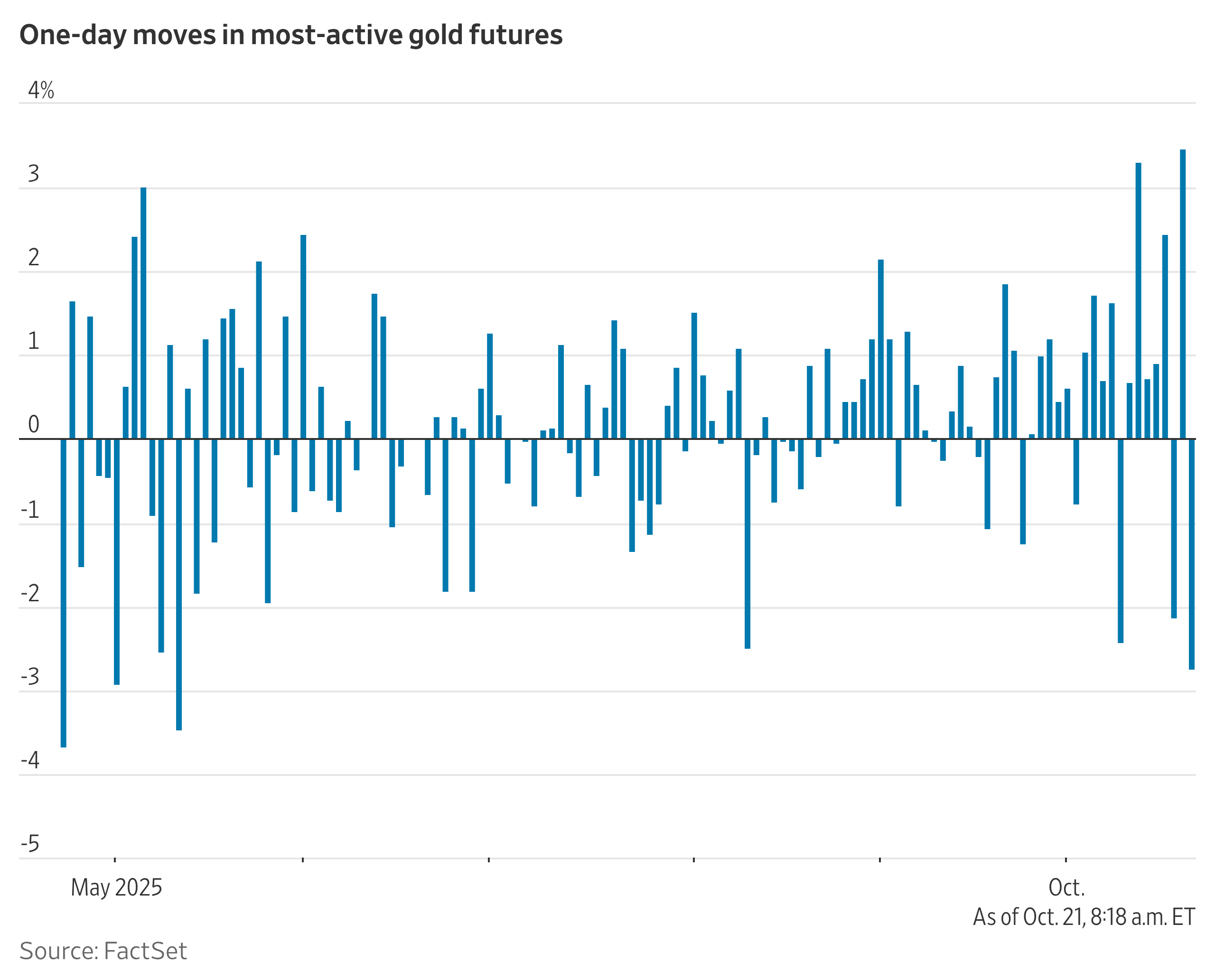

The diverging views left investors uncertain about the Fed’s next move, reinforcing demand for the dollar and reducing appetite for non-yielding assets such as gold and silver.

Risk Appetite Improves Across Global Markets

Equity markets in Asia and Europe stabilized after several sessions of volatility, with investors showing renewed willingness to add risk. Strong corporate earnings, firmer industrial data, and expectations of a gentler policy stance from global central banks all contributed to the shift in sentiment.

This gradual improvement in risk appetite has reduced short-term defensive positioning. As institutional flows rotated back into equities and credit markets, safe-haven metals lost some of the momentum that had supported them earlier this month.

Geopolitical Tensions Offer Only Limited Support

Broader geopolitical tensions continue to linger, but their influence on precious metals remains contained. Market participants have monitored developments in several regions, including ongoing negotiations aimed at de-escalation and energy-related disruptions. While these factors provide a mild floor under gold and silver, they have not been strong enough to counter the pressure created by a firmer dollar and rising equity sentiment.

Focus Shifts to Heavy US Data Calendar

Traders now turn to a data-packed US calendar that includes delayed Producer Price Index figures, retail sales numbers, and the Consumer Confidence Index. Later in the week, preliminary third-quarter GDP and the Fed’s preferred inflation gauge—the PCE Price Index—will offer clearer direction for rate expectations.

With policymakers split and markets searching for confirmation, this week’s economic releases are likely to define the dollar’s trajectory and, in turn, shape near-term movement in precious metals.