Gold is at a record high above $4000 an ounce, and reader, we have a quandary.

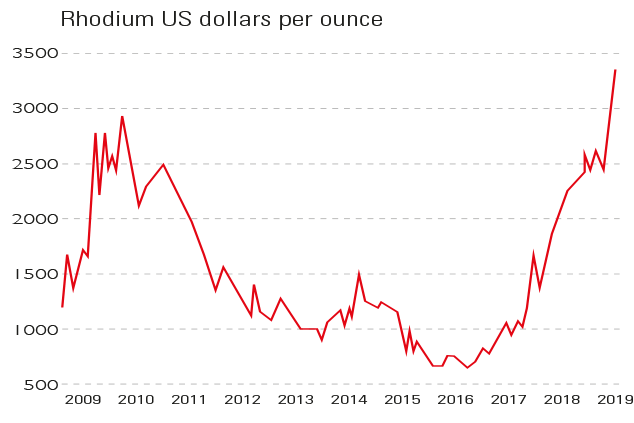

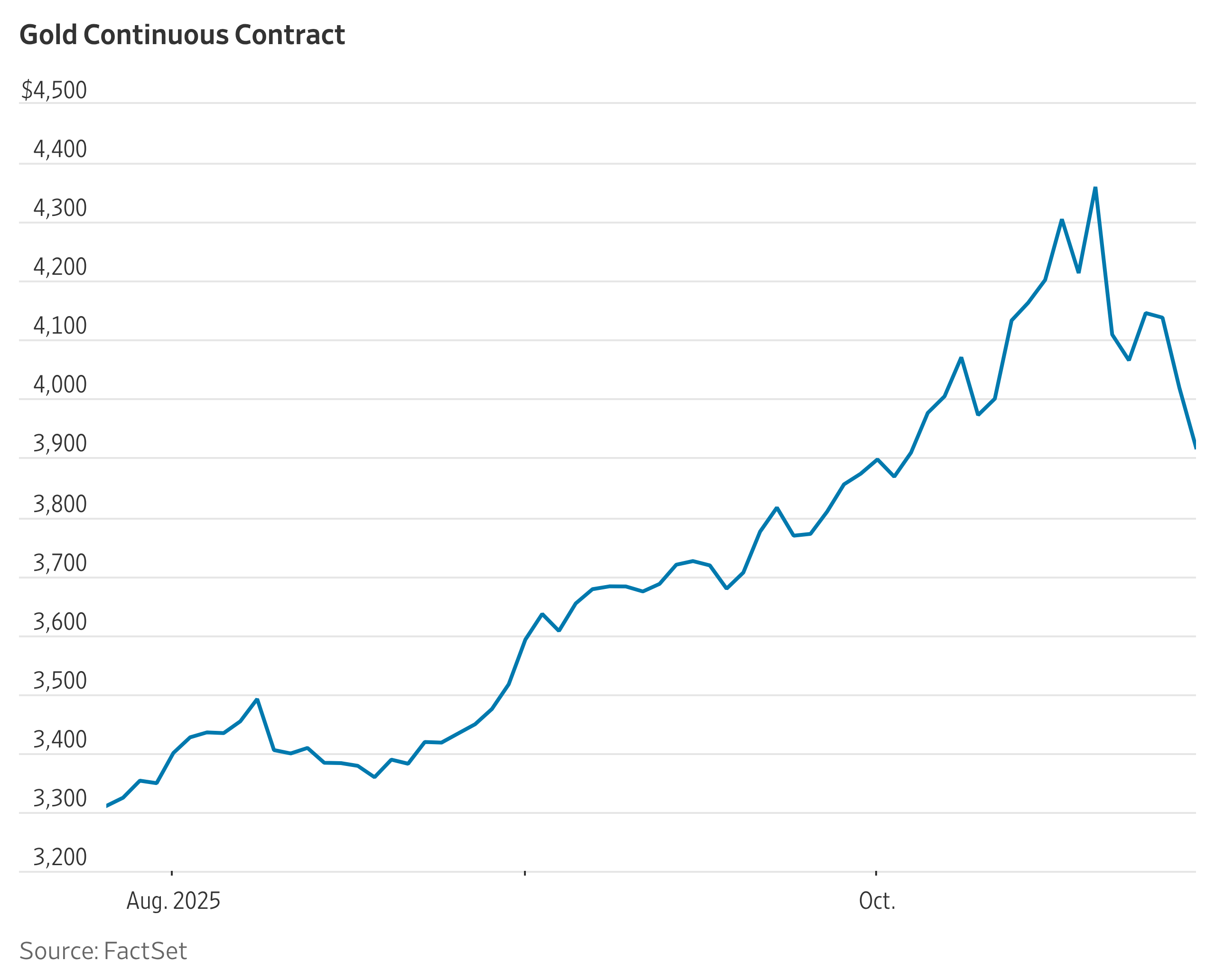

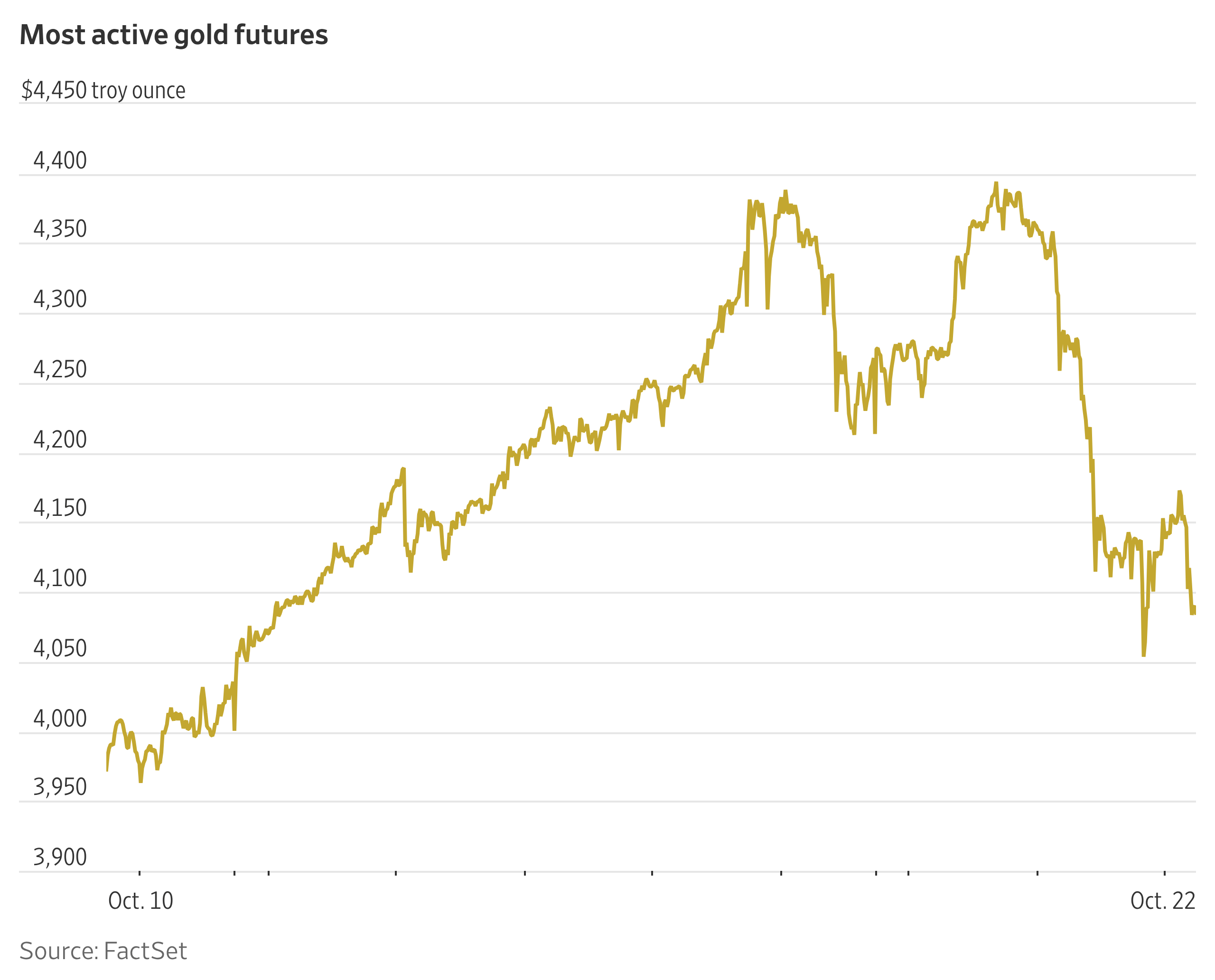

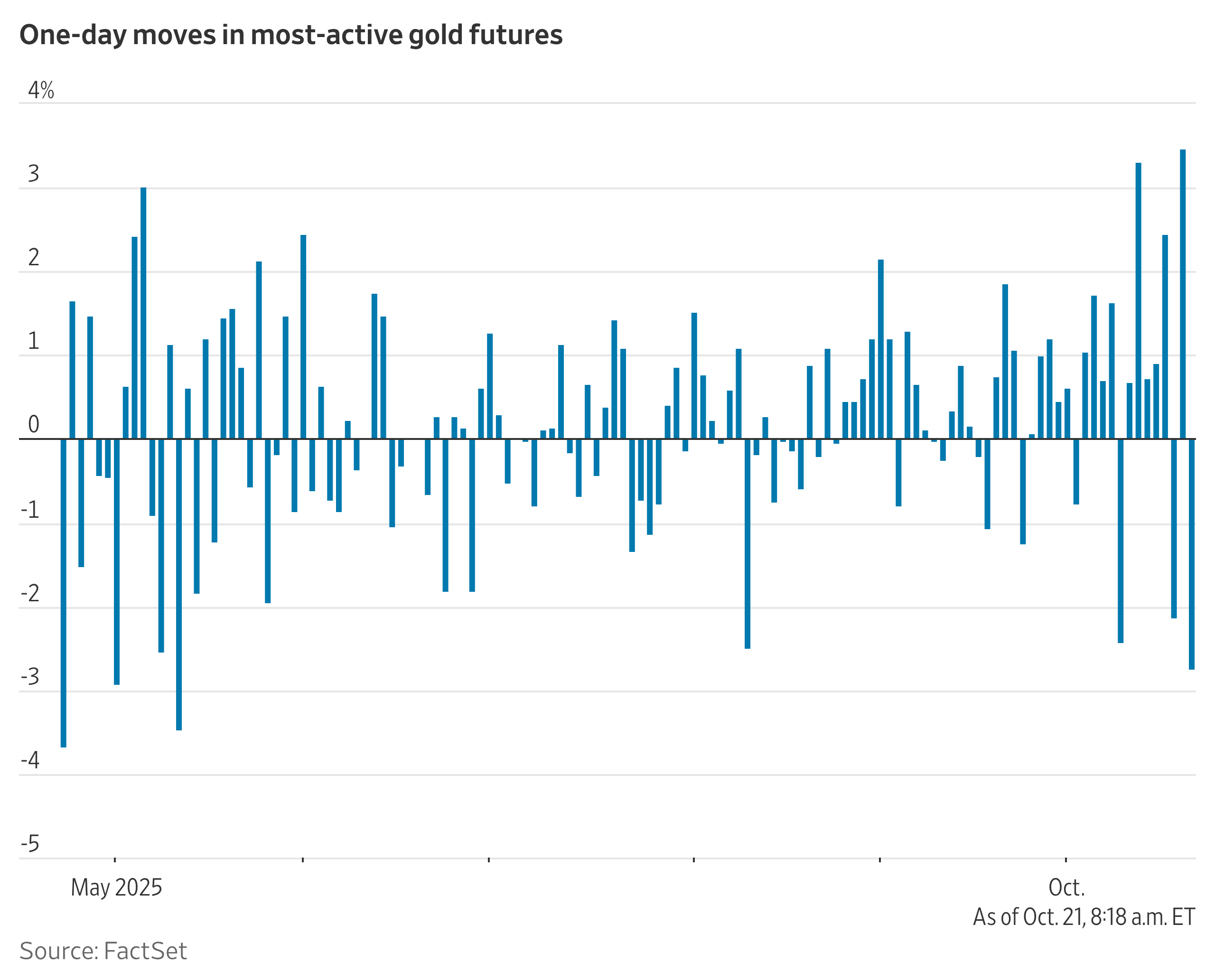

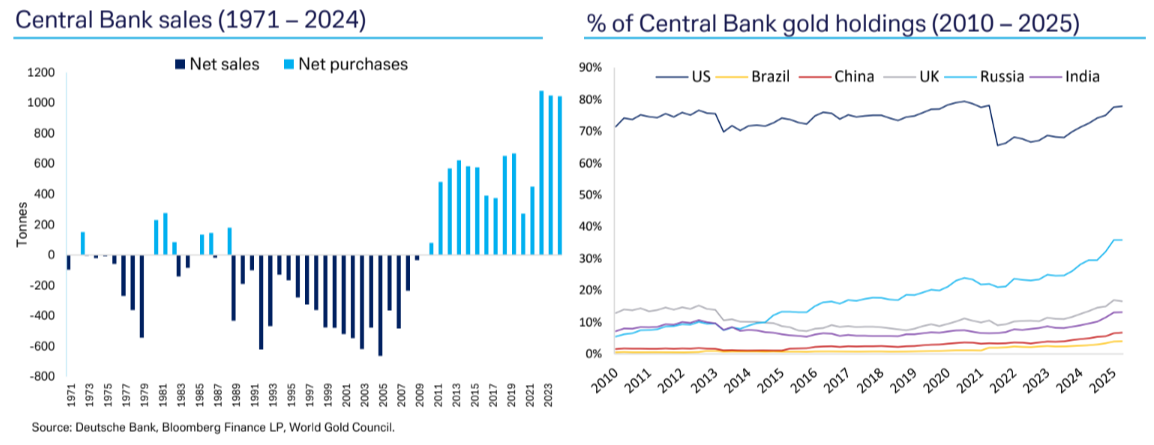

As a blog about markets and finance, FT Alphaville is obliged to note gold’s milestone. The traditional way to do this would be with some charts that illustrate a point, such as these:

We’d follow the charts with some pithy expert quote we found on Substack, like this one from Brookings Institution’s Robin J Brooks:

The latest rally in gold isn’t about a flight out of the dollar. It looks more like it’s a flight out of all G10 currencies, as fears of inflation and currency debasement grow.

And a more specific quote that adds valuable context to the first chart, such as this one from SocGen’s Albert Edwards:

We have long stressed that Japan is a bellwether for western markets, in large part because its credit/equities/macro bubbles burst in the late 1980s well ahead of their western counterparts in the 2008 GFC. Japan has been a trailblazer ever since, beating a policy path for others to follow through the post-bubble fiscal jungle. [ . . . ]

[T]he talk [is] of further fiscal stimulus and pressure on the BoJ to step up QE to finance the deficit. Politicians everywhere have fallen into a fiscal trap of their own making; increasingly hostile electorates will surely not tolerate the pain necessary to avoid government debt spiralling out of control. [ . . . ]

Under PM [Sanae] Takaichi, Japan is likely to return to the economics of her mentor, former PM Abe who pursued a currency debasement policy camouflaged as a side effect of super‑aggressive QE from 2013. That spells fiscal easing accompanied by ever more aggressive QE (remember Japan never stopped QE, merely tapered it). The precious metals complex is already responding to the fiscal dominance, which means more currency debasement and more inflation.

And while commentators get excited as gold breaks above $4,000, just consider that the equivalent in yen is now above $5,500. Japan is still leading the way.

Next we’d include a price prediction, such as this one published yesterday by Goldman Sachs:

We raise our Dec2026 gold price forecast to $4,900/toz (vs. $4,300 prior) because the inflows driving the 17 per cent rally since August 26 — Western ETF inflows and likely central bank buying — are sticky in our pricing framework, effectively lifting the starting point of our price forecast.

[ . . . ]

We still expect:

Central bank buying to average 80/70 tonnes in 2025/2026 as EM central banks are likely to continue the structural diversification of their reserves into gold (contributing 19pp to the 23% price increase we expect by Dec26) following the freezing of Russian reserves in 2022. In particular, our base case assumes that the current trend in official sector accumulation continues for another three years.

Western ETF holdings to rise as the Fed cuts the funds rate by 100bp mid-2026 (contributing 5pp by Dec26).

Speculative positioning to gradually normalise (contributing -1pp by Dec26)

Then we’d try to add some edge by finding a correlated prediction, such as this one from UBS:

Silver prices are being driven by concerns over elevated global debt and large fiscal deficits—especially in the US—and the risk of further USD weakness on the back of Federal Reserve rate cuts. While these factors are well known, silver’s sensitivity to them is not constant and requires ongoing reassessment. Meanwhile, silver continues to benefit from industrial application demand, driven by electronics and photovoltaic applications.

In this context, we now expect the gold-silver ratio to move toward 76x (from above 80x at the time of writing), reflecting a reassessment of investment demand strength and the sensitivity of silver prices to ETF inflows. In short, we expect silver ETF holdings to climb to previous highs of 1,021 million ounces (moz), up from the current level of around 822 moz. Previously, we thought the ratio would remain at around 85x, given a softer growth outlook into year-end and less investment demand than is the case. With a more constructive macro view for 2026, investors appear to be looking through the potential for soft growth in the near term.

For many investors, silver remains cheap relative to gold—a view supported by historical comparisons. While there are valid reasons for a high goldsilver ratio, most notably the absence of central bank purchases and its reduced quality as a “safe haven,” the potential for a relative revaluation is increasingly attractive. This is particularly relevant as gold trades at all-time highs in both real and nominal terms, making it harder for the market to find tangible reference points — a challenge that does not apply to silver. As a reference, the gold-silver ratio fell below 70x in 2021 as markets recovered from the initial COVID-19 shock, supported by zero interest rates, ballooning deficits, and a weaker US dollar.

The back half of the post could be filled with cut-and-paste inbox commentary from the likes of Rabobank:

By implication, [gold’s break above $4k] questions the USD’s function as a safe haven asset. [ . . . ]

Since the GFC, not only has portfolio investment by non-USD based investors surged, but a significant share has been directed into US assets. As figure 2 illustrates, US equities and long-term debt instruments have been significant beneficiaries of these flows. The rotation trade that characterised the first five months of this year saw investors questioning the size of their holdings of US assets and triggered a spate of diversification. This appeared to run out of steam in June as the S&P 500 embarked on a series of fresh highs. However, the surge in the S&P has been linked essentially to the AI boom. Beneath the surface, it would appear that diversification is still a priority for many investors. [ . . . ]

While the outlook for the USD faces risks into 2026, not least in the shape of the potential threat to Fed independence, in our view the sheer depth of US capital markets means that investors will not be able to turn their back on the USD if geopolitical risks intensify.

The further down the inbox we go, the more outlandish the commentary would become. Eventually, we’d get to this kind of thing, from Deutsche:

As the dollar weakens, central banks face a defining question: can Bitcoin serve as a credible reserve asset alongside – or even in place of – gold? A strategic Bitcoin allocation could emerge as a modern cornerstone of financial security, echoing gold’s role in the 20th century.

[O]ur recent research paper (here), compar[es] Bitcoin and gold across adoption trends, asset characteristics and macroeconomic performance. Assessing volatility, liquidity, strategic value and trust, we find that both assets will likely feature on central bank balance sheets by 2030.

But reader, here’s the quandary. A thing we’ve learned in nearly 20 years of doing this is that you don’t much like to read about gold. What you like most is to write about gold.

A comment box is below. Please fill it with your perspectives on debasement, transferability, the physical/paper mismatch, Bretton Woods, Basel III, Gordon Brown, Incas, bimetallism, crypto maximalism, and whatever else is exercising your humors. Just be aware that very few people will be reading below the line either.

{kind=link}