Quick Read

-

The IRS classifies GLDM as a collectible, hitting gains with up to a 28% tax rate. A Roth IRA eliminates that surcharge entirely.

-

GLDM has surged 229% over ten years but dropped 7% in the past month, and Roth investors can rebalance freely without triggering collectibles-rate taxes.

Gold sitting in a taxable brokerage account creates a tax problem most investors miss until the sale settles. The IRS treats physical-gold exchange-traded funds (ETFs) like SPDR Gold MiniShares Trust (NYSE: GLDM) as collectibles, which means long-term gains can be taxed at rates up to 28% instead of the 15% or 20% that applies to ordinary stock funds. Holding GLDM inside a Roth IRA erases that surcharge entirely and turns qualified withdrawals into tax-free income. That single wrinkle is the strongest portfolio-construction case for putting GLDM in a Roth IRA rather than a brokerage account.

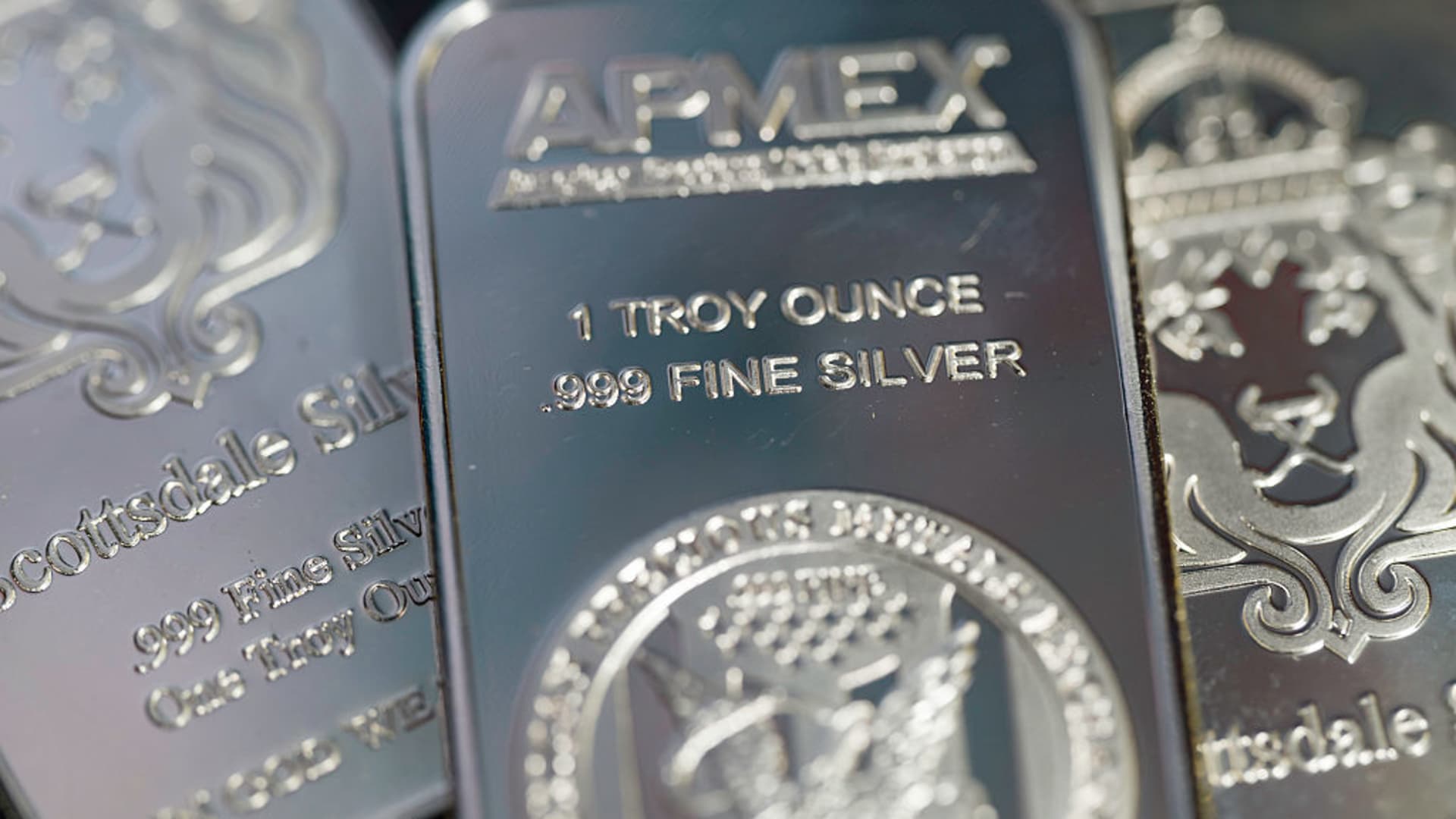

Jason York / Shutterstock.com

What GLDM Actually Does

GLDM is the low-cost MiniShares version of the original SPDR Gold Trust. It is a grantor trust that owns physical gold bullion held in vaults, and shares track the spot price of gold minus fund expenses. There is no operating business, no dividend, no option overlay, and no credit risk. The return engine is purely the price of gold.

The intended portfolio role is diversification and inflation insurance. With the consumer price index (CPI) rising from 321.56 in June 2025 to 335.12 in May 2026 and the 10-year Treasury yield sitting near 4.5%, gold competes with real yields for safe-haven dollars. Inside a Roth, that competition matters less because the appreciation compounds without tax.

Does the Strategy Deliver?

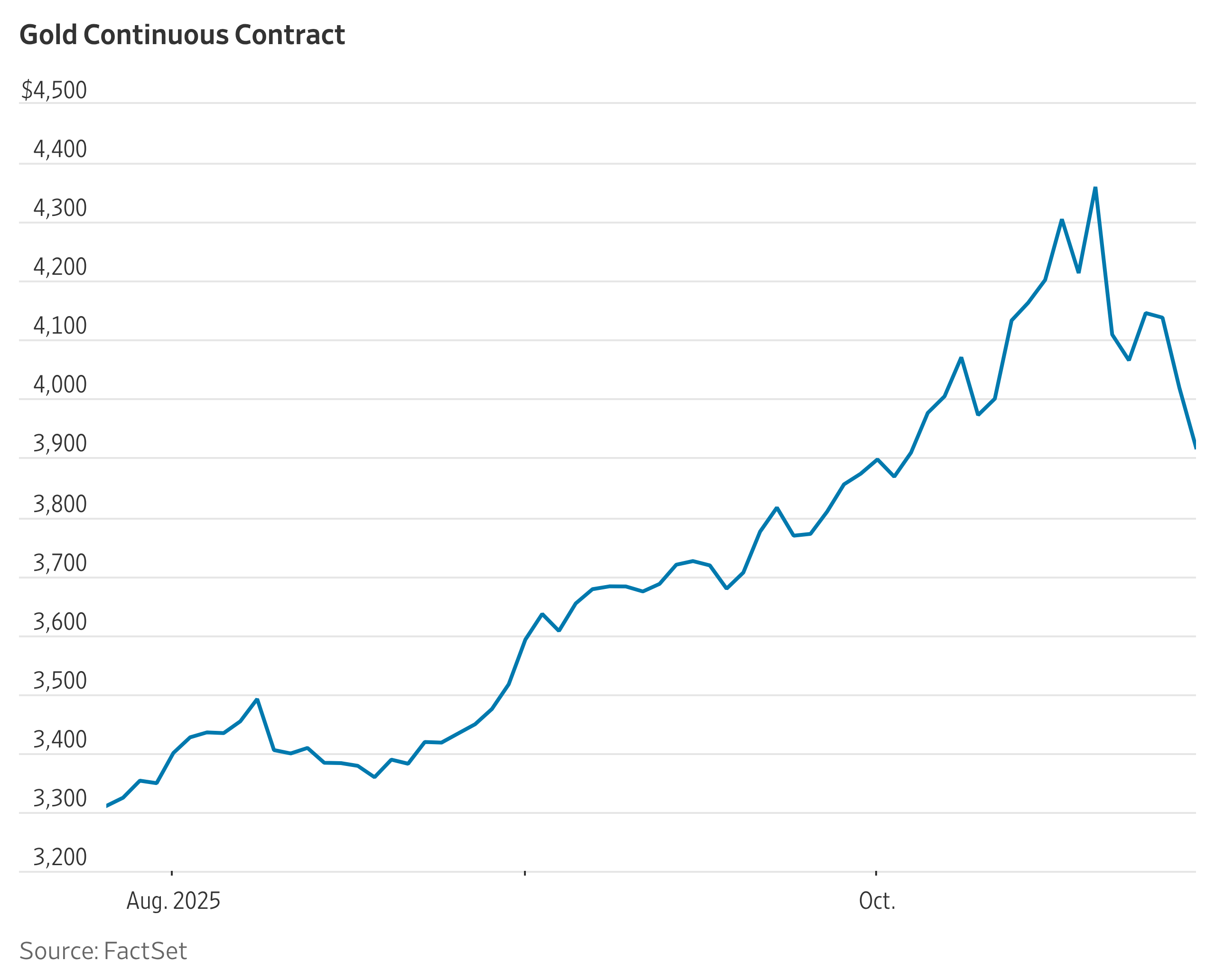

Long-term, gold has done its job. GLDM is up 22.4% over the past year, 131.7% over five years, and 223.1% over 10 years, with shares trading near $82. That 10-year run rivals broad equity indexes while providing genuinely different return drivers, which is the whole point of holding gold.

Don’t wait: the analyst who called NVIDIA in 2010 just revealed his top 10 AI stocks. See the full list FREE now.

Peer iShares Gold Trust (NYSEARCA: IAU) returned 130.2% over five years and 205.8% over 10, very similar to GLDM. Both funds hold 100% gold bullion, and IAU manages roughly $64 billion in net assets at an expense ratio of 0.25%. GLDM was built specifically to undercut IAU on cost for buy-and-hold investors, and the price-tracking math means the cheaper fund wins the compounding race over decades.

The recent picture is rougher. GLDM is down 8.3% over the past month and 4.8% year to date, partly because real yields are elevated and gold tends to lag when bondholders can lock in meaningful coupons. That volatility is exactly why the Roth wrapper helps: rebalancing a gold position in taxable triggers collectibles-rate gains, while a Roth lets you trim and add freely.

The Tax Math, Side by Side

|

Account Type |

Long-Term Gains on GLDM |

At Withdrawal |

|---|---|---|

|

Taxable brokerage |

Up to 28% collectibles rate |

Already taxed |

|

Traditional IRA |

Deferred |

Ordinary income rates |

|

Roth IRA |

None |

Tax-free if qualified |

The Tradeoffs

-

Zero income. GLDM pays no dividend and no interest. In a Roth, the tax-free compounding advantage is most valuable on assets producing cash flow, so allocating space to a non-yielding asset has an opportunity cost relative to dividend ETFs or real estate investment trusts (REITs).

-

Long flat stretches. Gold can go nowhere for years. The 2011 to 2019 period saw essentially zero price progress. Investors expecting steady appreciation will be tested.

-

Tracking only the metal. GLDM gives you gold exposure, nothing else. There is no leverage to mining productivity or operational upside. If gold sits, your position sits.

Who Benefits Most

A 5% to 10% GLDM sleeve makes sense inside a Roth IRA for investors who want a genuine diversifier against equity drawdowns and currency debasement, and who would otherwise face the collectibles tax in a brokerage account. The Roth structure neutralizes the worst tax feature of gold ownership and lets the position compound untouched. Investors prioritizing current income, or who need the asset to throw off cash for living expenses, should put dividend equities or TIPS in the Roth instead and hold gold, if at all, somewhere the tax wrinkle stings less.

Don’t wait: the analyst who called NVIDIA in 2010 just revealed his top 10 AI stocks. See the full list FREE now.