Money creation follows the same basic logic in every modern economy, including Nigeria.

It is carried out by two types of institutions: commercial banks and the central bank.

Commercial banks create the lion’s share.

When a bank extends a loan, it credits the borrower’s account with a deposit that did not previously exist. At that moment, both a new loan asset and a new deposit liability appear on the bank’s balance sheet.

The central bank acts as banker to the banks. Each commercial bank holds a deposit account at the central bank, which appears as reserves on the central bank’s balance sheet.

Banks use these reserves to settle payments among themselves within the banking system. Crucially, banks do not need to have reserves in hand before making a loan.

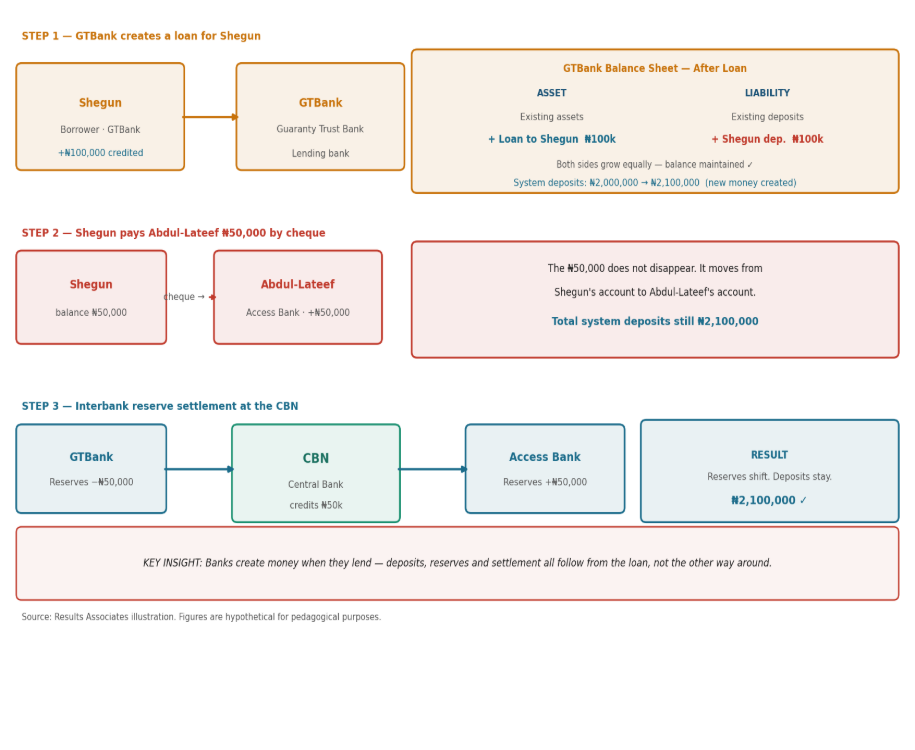

For example, if customer Shegun borrows 100,000 naira from Guaranty Trust Bank (GTBank), the bank will record a loan of 100,000 naira as an asset and credit Shegun’s deposit account with 100,000 naira as a liability.

If Shegun then writes a cheque for 50,000 naira in favour of Abdul-Lateef, who has an account with Access Bank, and the cheque is presented for payment, GTBank will transfer 50,000 naira from its reserve account at the central bank to Access Bank’s reserve account.

If GTBank does not have sufficient reserves to honour the payment, it can borrow reserves from another bank, sell assets, or borrow from the central bank against collateral. In short, banks create the loan first and fund it afterward.

Suppose that before the loan to Shegun, total deposits in the banking system were 2,000,000 naira. The loan from GTBank increases deposits in the system by 100,000 naira, from 2,000,000 to 2,100,000 naira.

Not all bank lending works this way, however. If the loan to Shegun were extended by Coronation Merchant Bank Limited (CMB), which does not take retail deposits, the mechanics would be different. CMB would debit its own account by 100,000 naira and transfer that amount in reserves to GTBank’s reserve account at the central bank; GTBank would then credit Shegun’s deposit account with 100,000 naira.

In this case, total deposits in the banking system remain 2,000,000 naira. CMB has intermediated existing deposits rather than created new ones. The distinction matters: deposit-taking commercial banks expand the money supply, while non-deposit-taking institutions merely recycle existing money.

The amount of money that banks can create is not unlimited. It is constrained by two main factors. First, capital adequacy: the amount of capital that the CBN requires banks to maintain so that, if loans go bad, shareholders rather than depositors bear the losses. Second, banks are constrained by their ability to find profitable, creditworthy borrowers.

The other money creator is the central bank. It creates new money through several mechanisms: purchasing foreign exchange, buying bonds or other assets from commercial banks, providing collateral-backed loans to banks, or directly financing government expenditure where permitted by law (see Figure 2). In each case, the central bank expands its balance sheet and credits the reserve account of a commercial bank, which in turn credits the deposit account of the final recipient.

Money creation, if not managed with care, can contribute powerfully to serious economic crises. That raises five questions: who created money in Nigeria between 2015 and 2024, what happened when that money was spent, what lessons should be drawn, what the CBN is trying to do now, and what broader reforms are needed to deliver durable price stability.

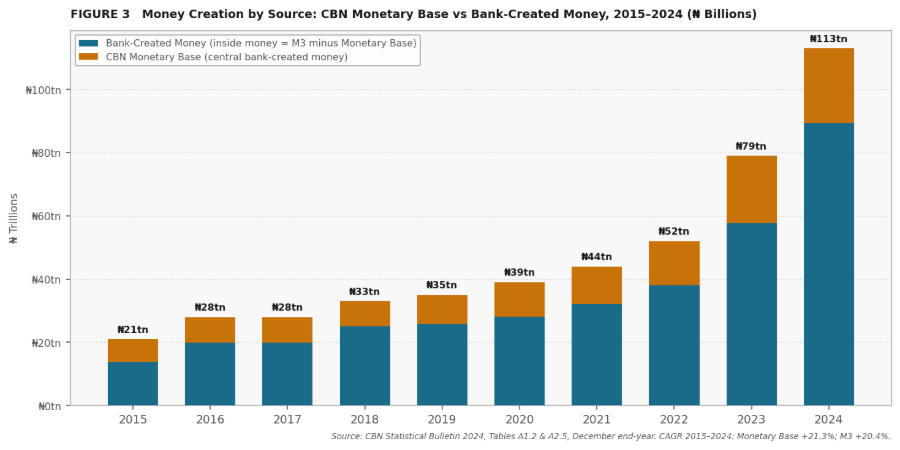

Who created money between 2015 and 2024?

As shown in Figure 3, the Central Bank of Nigeria originated between 21 and 34 percent of total purchasing power, while commercial banks created between 66 and 79 percent. Combined, total money grew at a compounded annual rate of 20 percent over the period.

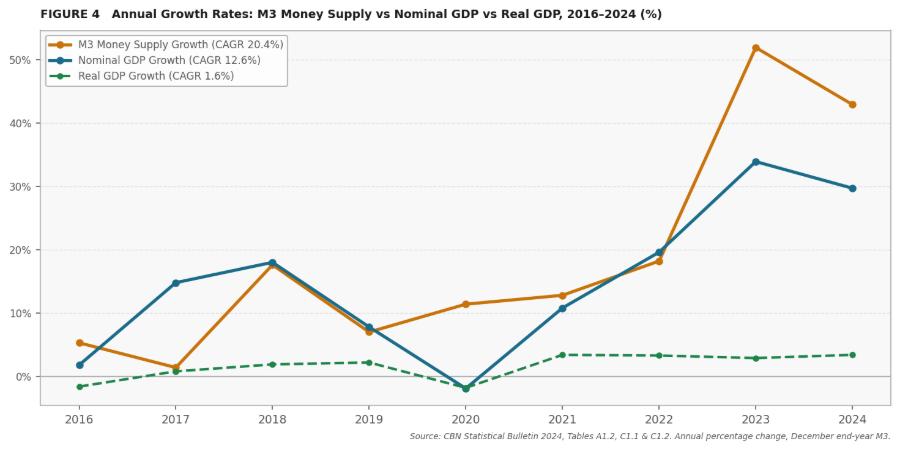

What happened when the money was spent?

Nominal GDP — the total income generated in the economy before adjusting for inflation — grew at a compounded annual rate of 12.6 percent. Real GDP, which removes the effect of price increases and reflects actual gains in goods and services produced, grew at only 1.6 percent per year.

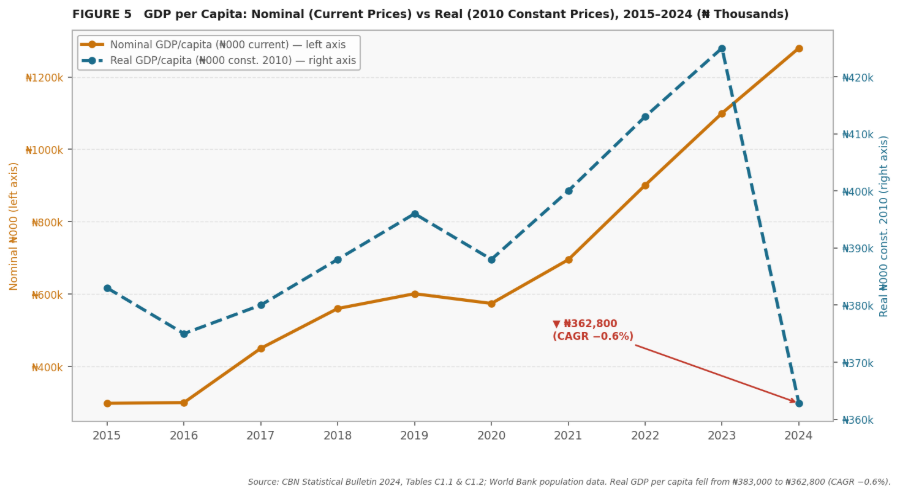

Because money supply expanded at 20 percent annually while the real economy grew at just 1.6 percent, excess purchasing power helped fuel inflation. Measured by the GDP deflator, the overall price level increased by 152 percent over the period. Real GDP per capita — the clearest broad indicator of living standards — fell by 0.6 percent, from ₦383,000 in 2015 to ₦362,800 in 2024 (in constant 2010 naira).

In plain terms, more naira circulated through the economy, but the economy did not produce enough additional goods and services to absorb that increase without a major rise in prices.

What lessons follow?

Nigeria’s experience shows how excessive money creation by both the central bank and commercial banks can produce a damaging deterioration in economic conditions when purchasing power far outpaces the real supply of goods and services.

The consequences are predictable: high inflation, currency depreciation, rising debt, economic contraction, and weaker living standards.

Two lessons follow. First, money creation must be regulated in order to achieve and maintain price stability. Second, once created, money must be deployed into productive activities that enhance the economy’s capacity to produce sustainable growth.

When these conditions are absent, the economy does not merely become more expensive. It becomes less capable of generating durable growth. Reining in inflation therefore requires action on both the demand side — through monetary policy — and the supply side, through fiscal discipline and institutional reform.

What is the CBN trying to do now?

The CBN has launched several important reforms: unification of the exchange rate, a formal commitment to stop monetizing government debt, and a sharp increase in interest rates to curb inflation. Most importantly, it has committed to building the institutional capacity to conduct inflation-targeting monetary policy and to deliver price stability over time.

These are welcome steps, but they face a fundamental limitation. Central banks can influence only the demand side of inflation. As Ben Bernanke, former Chair of the Federal Reserve, has observed, central bankers have “lending power, not spending power.” That requires action on three fronts that lie beyond the CBN’s direct control.

Fiscal discipline and institutional guardrails. The first step toward price stability is controlling government spending. This requires institutional mechanisms that incentivize all levels of government to live within their means. If this does not happen, the central bank faces three options, each of which undermines price stability: monetizing the deficit through the “ways and means” account; lowering interest rates to reduce the government’s debt burden; or forcing banks to hold government paper through financial repression.

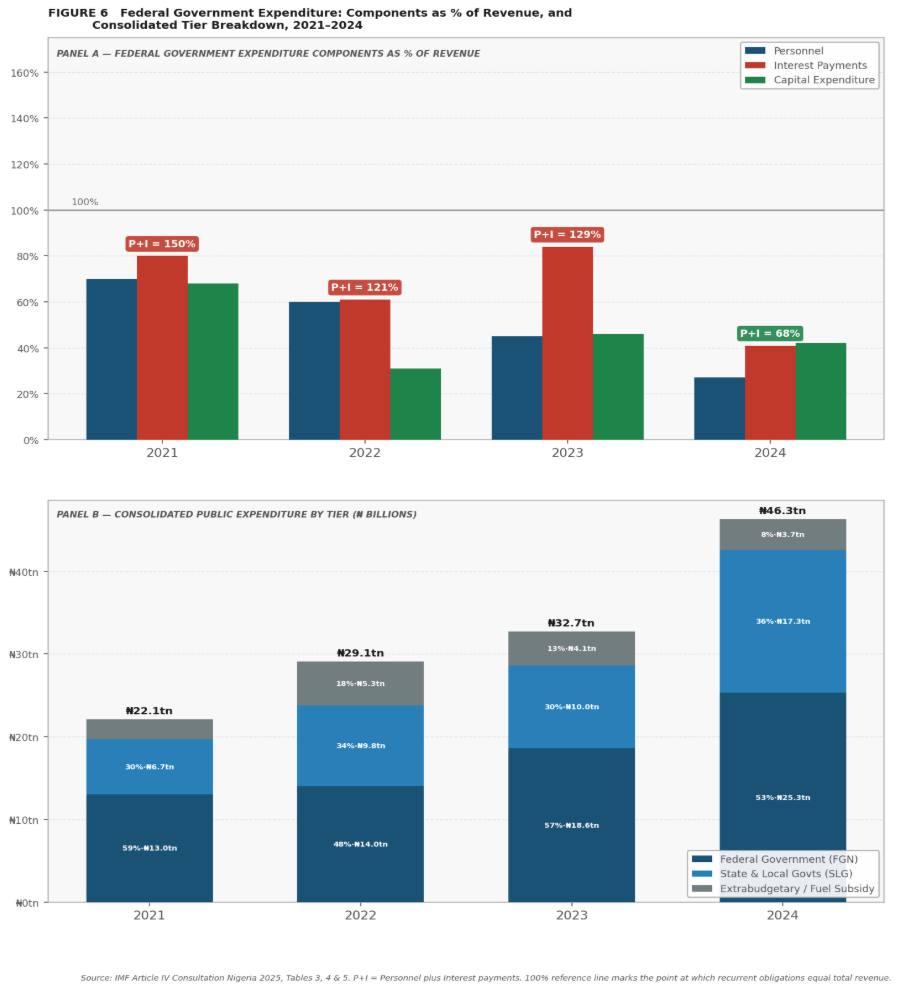

Quality of public expenditure. The second requirement is to improve the quality of public spending. Federal personnel costs and interest payments exceeded federal revenue over 2021–2023, reflecting both poor expenditure composition and inadequate revenue capacity.

Accountability at the subnational level. A significant portion of expenses, including extrabudgetary spending, occurs at the state and local government levels, where transparency and accountability are especially weak. Bringing subnational spending under stronger oversight is therefore essential to any credible fiscal reform.

What broader reforms are needed?

CBN reforms alone are not enough. Because fiscal pressures that overwhelm monetary policy, and spending on productive activities that enhance the economy’s capacity to produce sustainable growth, originate mostly in political institutions rather than financial ones, durable price stability requires a broader institutional architecture — one that constrains fiscal behavior, strengthens public financial management, and ensures that monetary policy is not perpetually overwhelmed by political pressures.

Constitutional amendments. In the next legislative term, the administration should pursue constitutional amendments that require current expenditures over a presidential term to be financed within available revenues, and that borrowing be permitted only for capital investments whose expected returns demonstrably exceed their cost. These rules should apply to the states as well.

Public financial management infrastructure. Nigeria’s 2021 Public Expenditure and Financial Accountability (PEFA) assessment reveals serious systemic deficiencies. Scores of D, meaning below basic, are recorded across asset and liability management, accounting, audit, and budget transparency. These are matters addressed in the article Nigeria’s reforms real, but without fixing the plumbing, money will keep leaking, published in The Nation. A dedicated PFM reform unit should be established within the State House, with the Ministry of Finance as secretariat and strategic oversight from the Presidency.

An independent Office of Budget Responsibility. Nigeria should establish an independent body equivalent to the United Kingdom’s Office for Budget Responsibility — staffed by independent and technically competent Nigerians and adequately resourced to provide rigorous external scrutiny of fiscal policy.

Using federal leverage to promote transparency at the state level. The federal government should use its fiscal leverage systematically. Legislation should require states to implement international public sector accounting standards, publish audited financial and performance reports, and face withholding of federal transfers for non-compliance. Transparency is not just a governance value. It is a precondition for effective economic management.

Banking regulation and capital account management. Commercial banks create the largest share of purchasing power in any modern economy. Robust prudential regulation is therefore essential. Nigeria should also consider calibrated capital account measures to manage the destabilizing effects of short-term financial flows. Ghana’s 2022–23 crisis offers a recent regional example of the dangers of sudden capital reversals without adequate buffers.

An independent commission to identify self-financing projects. Drawing on the framework advanced by renowned Japanese economist Richard Koo in his book The Pursued Economy, Nigeria should establish independent commissions at the federal and state levels to depoliticize project selection and focus public investment on initiatives that lower the transactional costs of doing business and strengthen the supply side of the economy.

Conclusion

These recommendations form a mutually reinforcing institutional framework. Constitutional fiscal rules address the political economy of indiscipline at its root. A stronger PFM system makes public resources visible and steers them toward supply-side investment.

An independent fiscal watchdog and effective federal leverage extend standards of transparency to the state level. Prudential banking regulation and calibrated capital account management protect the financial system from common sources of crisis.

Independent commissions at the federal and state levels, informed by the kind of rigorous investment analysis advocated by Richard Koo, will be essential to improving the quality of capital investment and directing public resources toward projects that can genuinely grow the economy.

Nigeria has what few countries enjoy at once: a large domestic market, a young and entrepreneurial population, and the human capital to make West Africa a significant source of global growth. Unlocking that potential requires more than a reformed central bank. It requires an institutional ecosystem in which fiscal discipline is embedded in law, public money is transparently managed, and the financial system is strong enough to support sustained, low-inflation growth.

The current crisis is painful, but it is also an opportunity that should not be wasted.

- Aboubakr Kaira Barry, CFA is the Managing Director, at Results Associates in Bethesda, Maryland, USA.