Any adviser being met by a client asking to invest heavily in cryptos might feel their heart sink, especially when the talk turns to bitcoin and the wild swings associated with digital currencies.

But elsewhere, many fund managers are looking to the underlying technology, blockchain, to take advantage of its structure and its ability to settle transactions instantly, 24/7.

It could also open up a new market for retail investors using crypto platforms for other digital assets.

Large institutions are already developing solutions to trade digital assets, and a number of fund managers have created tokenised funds for the institutional market.

Meanwhile, the Financial Conduct Authority last year published a paper discussing the potential for tokenised funds for retail investors in the UK.

But detractors are concerned about where responsibility lies in a distributed ledger, and whether that network can provide the same robustness as traditional trading.

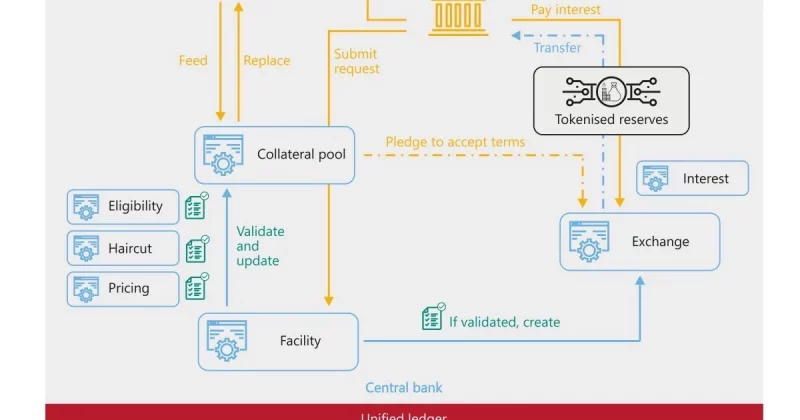

The concept of a digitised fund lies in the token: a digital representation of a unit or a share, which itself is traded, rather than the unit itself.

In future, the fund units themselves could be tokenised.

The token can be ‘minted’ onto the blockchain, which runs on a distributed ledger basis.

This can help with trading as it means that the ledger itself, which records the asset transactions, is held simultaneously at multiple points in the chain, allowing any transaction to be updated straightaway.

Kieran Mullaley, global head of the capital markets practice at Capgemini, says the system currently used to trade securities is seen by many to have inherent inefficiencies: “Lots of different people have a different version of the same information.

“[With distributed ledger technology (DLT)] the information is held on a single shared ledger, updates are simultaneously replicated across multiple nodes so authorised parties immediately see the same shared record, and everyone sees the right version of the transaction with an immutable audit trail.”

With the current system, he says, each institution involved in the trade has to maintain its own data stores with similar versions of the record, and checks are made to ensure accuracy through messaging via Swift.

Lukas Enzersdorfer-Konrad, chief executive of crypto platform Bitpanda, says that in addition, for retail, 20 per cent of the trade happens on weekends, which trading via the blockchain allows.

Tokenisation would also allow fractionalising of large illiquid assets, such as those in private markets.

The FCA, for its part, published a consultation paper in October last year, CP25/28 and is keen to progress the concept.

It said at the time: “We expect tokenised funds to drive competition, including against conventional authorised funds.

“As younger generations invest differently, it is important that regulation evolves to serve changing consumer needs.

“Tokenisation can open new routes to distribute funds, broaden access to private markets and infrastructure investment and reduce the costs of small transactions, while maintaining existing consumer protection.”

Using Web3, the new iteration of the internet that allows blockchain, the FCA generally does not see the need to introduce new regulation.

It says: “Firms can already use DLT under our technology‑neutral rules, provided they meet our requirements, including clear accountability and controls. We will continue to keep our rule book under review as tokenisation develops.”

Brian Smith, managing director and chief digital assets officer of Zilo, a financial infrastructure firm, says: “Web3 is just a technology layer. Regulated assets carry their legal and compliance obligations with them onto any chain”.

The token is created and managed by a ‘smart contract’ on the blockchain; this smart contract keeps a record of token holders and automates processes such as issuing and redeeming tokens when an investor places an order.

The rest of the trade’s processing happens through existing fund infrastructure, while retail investors can trade using digital assets such as stablecoins or via traditional fiat rails.

Catriona Kellas, international legal lead – digital projects at Franklin Templeton, which has a tokenised money market fund, says: “When we’re talking about the tokenisation process, it’s the system for record-keeping that’s used to hold the shareholder register; it’s a way of recording ownership.

“The tokens are the shareholder record, and the blockchain enables them to be transferred or held, which is more convenient and more secure.

“The shareholder register by law is the prime evidence of entitlement to the share, then you have the depositary and custody. These are coming in under the fund, and these are the entities that are holding the fund’s assets.

“With tokenisation, that process is not being touched at all, these funds assets are being held as they always were.”

Simon Barnby, chief marketing officer at Archax, which provides tokenisation infrastructure for fund management firms, says: “The underlying assets are basically locked; if someone comes and buys Aberdeen money market fund, you invest in the fund and we hold that investment in custody.”

Making moves

The big institutions are already working to develop their own tokenisation solution.

BlackRock launched its tokenised money market fund in 2024, BlackRock USD Institutional Digital Liquidity fund, and it now has $2.47bn in assets.

Chair and chief executive Larry Fink said in his March shareholders’ letter that the concept had huge potential for the retail market: “Today, there’s very little access to traditional investment products in digital wallets. We plan to lead the charge in changing that.”

There are currently 244mn stablecoin holders and 170 tokenisation platforms globally, according to RWA.xyz, the tokenisation data analytics firm.

Funds providing this solution might, for example, offer a tokenised share class of an existing fund, or be a tokenised version of other funds.

The tokens go up and down in value, like a conventional unit.

No tokenised funds yet exist for the retail market in the UK, but in the institutional space, a popular option is a tokenised money market fund, which many institutional fund managers are trying.

One of the reasons is that the token generated from the fund has developed an additional function of serving as collateral by anyone needing a fast asset when borrowing shares, for example, and it can also pay a yield.

Barnby at Archax says: “You can use your token as collateral for margin or for Forex trading; you can use this tokenised money market fund as payment for 24/7.

“You’re not restricted by banking hours; it enhances capabilities because you have a token that can do stuff.” Managers set compliance and KYC so investors are verified.

The Franklin Templeton On Chain US Government Money Fund, for example, has been around since 2021, and has $843.74mn AUM; and its tokenised shares can be used as collateral.

Who’s responsible?

One question relating to tokenised versions of funds is the specific relationship between the asset and the investor.

Matt Ong, chief executive and founder of Ctrl Alt, which also provides tokenisation infrastructure, says: “If you were to buy this token, you would be recorded as one of the owners of this fund.

“Your transfer agent is responsible for the register for the ownership of this fund. If you were to sell that token to me, and do that through a regulated platform, the blockchain would update. The transfer agent would know that you’re the owner of that.

“The computers that are part of the blockchain are validating these transactions. You should think about the blockchain as a network of computers that talk to each other; that’s how the blocks get validated. That’s why it remains functional if one computer goes down.”

Despite the blockchain’s robustness, if one computer in the network goes down, it is the ‘distributed’ nature of distributed ledger technology that some feel is a flaw in the tokenisation model.

Jamie Alcock, professor of mathematics and finance at the University of Birmingham, says: “With a centralised model, with each party having specific responsibilities, it is easy to see who to complain to if something goes wrong.

“In the decentralised model, the transactions are effectively stored somewhere on the internet.

“The decentralised framing can obscure where responsibility actually lies. In traditional fund structures, there are clearly defined parties responsible for custody, administration, and investor protection.

“In tokenised systems, those responsibilities can become fragmented not only across functions but also across jurisdictions. Issuance, custody, and trading may each sit in different legal regimes, making it unclear which framework governs ownership rights or dispute resolution.

“When something goes wrong, whether that is a pricing issue, a failed redemption, or a technical fault, it is not always obvious who bears responsibility or how recourse is achieved.”

Barnby says: “That’s one of the challenges of the blockchain. The way blockchains are engineered is that shouldn’t happen, but there isn’t anyone to go to if something goes wrong.” If clients use his company’s platform, then they can go to Archax.

Enzersdorfer-Konrad of Bitpanda says: “From a regulatory perspective a government and a state need to define who ensures the protection for the consumer. In the UK there are regulators to ensure what gets offered to the retail or institutional client is in line with regulatory capabilities with local standards.”

The FCA expects that firms using DLT would remain responsible for their products, and if using DLT to support tokenised fund registers would still retain authority over the register, including to resolve consumer issues.

Another issue is whether the blockchain would be of sufficient robustness to cater for a mass transition to digital assets.

Professor Muttukrishnan Rajarajan, professor of security engineering and director of Institute for Cyber Security at City St Georges, who is working with institutions and high street banks, says: “Banks are talking about how scaleable the systems are when the number of transactions go up. This is what most of the digital banks are grappling with.”

The other issue is the rest of the digital infrastructure. Ong of Ctrl Alt says: “You can pay for a tokenised unit, and the most optimistic way is through some on-chain payment like stablecoin. The reason is that you buy a tokenised fund unit and it can settle instantly but take five days for the bank [to register], but if the cash ledger is in the blockchain as well, you can settle straight away.”

There has been some exploratory work done on developing central bank digital currencies, not least the consultation by the Bank of England on the digital pound, which could help that.

Rajarajan says: “The BoE wants to have a digital pound, but the BoE still has not decided on the infrastructure for the UK — tokens can be one solution. However, most of the central bank digital currency implementations across the globe are records on DLTs so far.”

Nonetheless, as more people create digital wallets, and the FCA paves the way for regulation of crypto assets, more investors might start to see digital funds from mainstream providers on their platforms, and find another purpose for their digital wallets.

Melanie Tringham is features editor at FT Adviser