This is an audio transcript of the Unhedged podcast episode: ‘Is the K-shaped economy real?’

Katie Martin

Markets and the US economy are brought to you today by the letter K. You may have heard people talking about this lately. Even central bankers are saying it’s a thing.

It’s this idea that one group of people — no prizes here for guessing that — rich people are holding up the economy. That’s the pointy-up bit of the K. While poorer people are scrimping and saving. That’s the downward sloping bit.

It cuts across to markets too. We have a small group of stocks in the US, unsurprisingly, tech stocks that are screaming higher and the rest of the market is a bit meh. Now, markets love this sort of thing. We have V-shaped recoveries, L-shaped recessions, and now all the cool kids are on about the K-shaped economy.

Today on the show, we are asking whether that actually makes sense or whether markets people are just really proud of how well they know the alphabet.

This is Unhedged, the markets and finance podcast from the Financial Times and Pushkin. I’m Katie Martin, a markets economist at the FT in London, back from having lots of fun and slightly too much booze at Kilkonomics in Ireland. And I’m joined down the line from New York City by His Excellency, the Very Reverend Robert Armstrong off of the Unhedged newsletter.

Robert Armstrong

Katie, I thought K-shaped stood for Katie shape to come. I don’t know what that would mean exactly.

Katie Martin

Quite sure with curly hair. Now Rob, before we get on to K-shaped, our inbox has been bulging this week, has it not? It has a lot of correspondence about two things.

Robert Armstrong

Yes.

Katie Martin

Firstly, contrary to the letter we got last week saying that I was too mean to you, we received lots and lots of emails from people saying I’m not too mean to you, and that if I am mean to you, I should carry on being mean to you.

Robert Armstrong

Then there were two explanations. One was meanness is how the British express affection as everyone knows. And the other was that I deserve mean treatment because I’m an interrupter and I’ve fact-checked both of these claims and I think they’re true.

Katie Martin

Yes. If it’s any consolation, I can tell you from a weekend in Ireland that there’s nothing that people in Ireland love doing more than being mean to the Brits. So it’s the circle of life.

Robert Armstrong

Goes, Yeah. It goes around, comes around.

Katie Martin

It goes around. The second point I’ve received a lot of correspondence on was making your own dishwasher tablets.

Robert Armstrong

Yes. What does he make them out of?

Katie Martin

Well, so I asked him, but first of all, so he …

Robert Armstrong

We can edit this out later. I just have to hear it.

Katie Martin

He doesn’t listen to this podcast though. I thought I would get away with it, but turns out his financial adviser does listen to this podcast and texted him saying: Why are you making your own dishwasher tablets? So I had to admit that I brought it up here and I got a massive eye roll from Mr Martin.

Anyway, for those asking, the recipe is: one of those stupid American cup measurements of bicarbonate of soda, one of citric acid powder, both of which are easy to buy online, and one tablespoon of washing up …

Robert Armstrong

. . . of nitroglycerine.

Katie Martin

Do not buy nitroglycerine online or anywhere else. Washing up liquid. So you mix it up, you put it in an ice cube tray. And then it will set, but, and I hate to admit it, but they do actually work. So …

Robert Armstrong

Should we talk about a serious topic now? Can we get back to the economy of America?

Katie Martin

I suppose so. Tell me Mr Armstrong about this K-shaped thing and why everyone is going on about it.

Robert Armstrong

I think context is really important here. Because with these narratives that take on a life of their own, a lot of things tend to get confused in the enthusiasm for a simple and appealing story.

So let’s start with some context. The main thing is that in terms of wealth, and I’m contrasting wealth to income here, the United States is massively unequal. So if you look, the Fed studies this stuff very carefully and has something called the distributional counts that lay out the facts, but basically 90 per cent, I don’t know, 96 per cent of the wealth — say somewhere between 96 per cent and 98 per cent of the wealth — is owned by the people on the top half of the wealth spectrum. So basically half the people have all the money and the other half have almost nothing.

That is the picture in America. Now, what’s important to remember though, is that is not new news. That is not something that just happened recently.

So we have all these corporate executives — right now I’m thinking of Procter & Gamble, Coca-Cola, Chipotle, all of these companies — have come out and said: We’re seeing a big divergence in behaviour between well-to-do consumers and not so well-to-do consumers. One spending a lot or continuing to spend at a good pace while the poor consumer spends less, is contracting. Now you can’t just put that down to vast wealth inequality in America because that was true all along.

Katie Martin

Yes.

Robert Armstrong

Something has to have changed here.

Katie Martin

Let me tell you something that has changed. So a few days ago we got the consumer sentiment report from the University of Michigan and it said: US consumers see a 23 per cent chance of losing their job over the next five years, and that is in the 99th percentile historically, going back to when they started gathering this data in 1997. So people have an unusually high level of insecurity about their job, and yet stock markets are just like: Well, hey, party time. So it’s like something is wrong with this picture.

Robert Armstrong

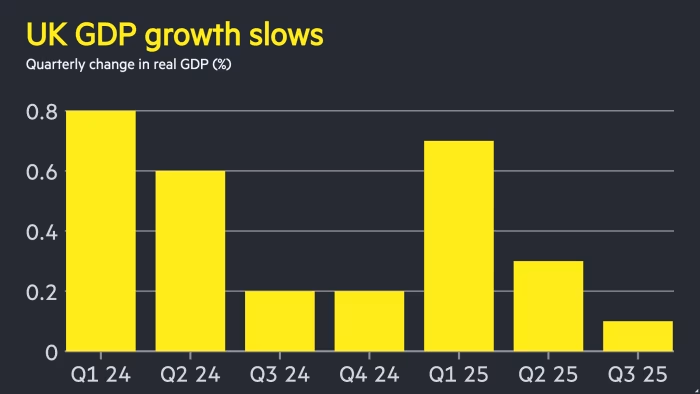

Yeah, and part of the reason that I think the K-shaped economy narrative has taken on so much momentum is that we are in an objectively confusing economy where although the unemployment rate is low, which is important to, we’re close to the level they call full employment.

You know about as many people are employed as can be employed in a modern economy right now about, but nobody’s getting hired. And there’s not a lot of new job creation, and yet GDP is growing very well. So how do you reconcile those two facts? And there’s a lot of other incongruous facts like this that need reconciling and the K-shaped economy helps pull together these incongruous facts.

That being said, I think something is going on here about people’s assessment of their prospects. My hypothesis would be that something has happened to change people’s attitude about the future because the stuff in the present hasn’t changed that much — the unemployment level, the growth of the economy, etc, etc. So what’s going on?

Katie Martin

So one thing to bear in mind there is, as you say, job openings have been falling pretty fast, while the economy seems to have been growing and while markets seem to have been going up and the charts going around sort of showing these two things diverging and saying: Oh look, it’s OK. It’s OK.

The problem is that some of that weirdness that’s going on in the jobs market is like the long tail of Covid. When people hired like mad, companies hired like mad because it was really hard to hire people and in the US but you had less immigration at the time, so it was hard to find people. So there were loads of ads out there.

And then you’re sort of seeing that unwind and you do see that in other economies as well. So there’s an effort to kind of pin some of this K-shaped phenomenon on to ChatGPT and say: Look, it looks like AI is eating away at job openings.

But I’m not sure a lot of that stacks up actually because what happened with this sort of upsy-downsy sort of phenomenon in the jobs market predates ChatGPT.

So to me, I don’t know, maybe a lot of it is just people trying to make sense of why markets are so fizzy and excited and happy about the world when there are just so many data points that tell you shouldn’t be. Maybe it’s just that.

Robert Armstrong

I think you’re on the right track in the sense that explaining what is happening here — on the assumption that what companies are telling us is true about the behaviour of lower-income consumers generally. And I think, by the way, you don’t have to take every single word a company says as gospel about this stuff.

Katie Martin

Yes.

Robert Armstrong

You know that’s the . . . and we can talk about that in a second, but taking what they say is true, you kind of have to do psychology. It can’t all be in the numbers like you are thinking about how consumers think about the future. So the numbers aren’t gonna tell you the whole story, but I will tell you some numbers that connect to the story, which is that everything we know about the kind of labour market and wages and so forth, tells us that somewhere 2022, 2023, workers really had the upper hand.

They were very much in demand. You could switch jobs and get paid more. So right after the kind of trauma of the pandemic, which we all remember, there was this moment where it really looked like the sun was coming out in an extraordinary way for working people. It’s not that things are so bad now, but that sense that the kind of deal between labour and management as it were, had changed, has faded, and we’re back to the old days and that may be weighing on people’s psychology, like, oh, I looked really good for a second there, but now we’re back to the same old stuff and that could be part of it.

Katie Martin

The thing is for markets generally, psychology’s mycology, so there are people who are calling BS on this whole K-shaped economy thing.

They include but are not limited to Dario Perkins from TS Lombard, friend of the show, friend of your newsletter. He said everyone in financial media is talking about wealth effects as a reason for the K-shaped economy. Fact-checked, true. They are.

Robert Armstrong

They’re talking about that.

Katie Martin

The more the US stock market rises, the wealthier people feel and the more they spend. At this point, this whole thesis is becoming a cliché, but not all clichés are true. His argument is there’s no evidence of this and the savings rate among wealthy people is flat. So you know, what wealth effects?

Robert Armstrong

Yes. And look, everybody knows that the very rich, when you give them more money, they just invest it. Like they’re consuming as hard as they can always.

Katie Martin

Yeah.

Robert Armstrong

You know, you know what I mean. I mean they’re, as they say, their marginal propensity to consume is very low. That’s part of the problem, and I, and several people have made this point too: If the issue was that all the money was going to the wealthy right now, then growth would be worse because when you give very rich people more money, they don’t tend to spend it. They don’t tend to spend more of it. In other words, they don’t spend more than they were spending already. So I think there has been, you’re quite right, there’s been exaggerated claims on the consumption side about how much of consumption is now down to rich people.

And the idea that has radically changed that now, like suddenly nobody buys dish detergent anymore, but like for diamonds and cocaine, things are going brilliantly. I just think that’s not true and I don’t think there’s any evidence for it. You know what I mean?

Katie Martin

Can you make cocaine at home? I don’t know. Listeners, please don’t tell us. So also calling like low-key calling BS on this is Dom White from Absolute Strategy Research, another friend of the show. And he’s saying that this idea that consumption is so concentrated among the very, very wealthy is just like a little bit off and that there’s not much evidence. And he doesn’t have a good sense that it’s like changing particularly over time.

So I do kind of wonder where this K-shaped thing kind of really got its claws into the narrative. I think it’s partly around, if I remember rightly, someone asked Jay Powell, chair of the Federal Reserve, the US central bank about it not so long ago, and he didn’t sort of bat it away, he accepted it as a premise to take seriously.

So his kind of acknowledgment or semi-acknowledgment that this is a thing has just kind of let it run away with itself. And now everything’s just like K-shaped, K-shaped.

Robert Armstrong

I think we need to make a distinction between two forms of the K-shaped economy thesis. One is a claim about the rich and the claim that all the spending that is going on in America, all the consuming, all the economic growth is down to rich people getting richer and spending more of their wealth.

I think we have very good reason to believe that this version of the thesis is false. Then there’s a second form of the K-shaped thesis that poor consumers are behaving differently now because they have a different view of their prospects than they might have had a year or two ago, and I think we have some reason to believe that that version of it is true.

Which brings us back to when Coca-Cola, Procter & Gamble, Chipotle, Dollar Store CEO, whoever, one of these people says our lower-income consumer is struggling and sort of working pay cheque to pay cheque. You know how, I mean, as one correspondent wrote into me after I wrote about this and said: How do they know who their rich and their poor customers are?

Katie Martin

That’s a good question.

Robert Armstrong

Do they, like, did they ask them at the door? But you know, that’s a story that a corporation can tell about why they didn’t have a great quarter that is not self-incriminating.

Katie Martin

Yes.

Robert Armstrong

In other words, it’s a lot easier story to tell than, “Well actually we’ve been kind of letting things slip generally around here, and we had a bad quarter and we screwed up in various ways.”

It’s more palatable to say: Well, it’s a harsh world out there, and our customers are under pressure. Yeah. I don’t, I’m not saying these guys are making this story up. No. All I’m saying is you can see why an executive might lean into the K-shaped narrative rather than leaning into “Our product is not very popular.”

Katie Martin

People are not listening to this podcast because of the K-shaped economy. That’s what you’re saying?

Robert Armstrong

Yeah, exactly. And there are companies that are reporting pretty well.

Katie Martin

Yeah.

Robert Armstrong

Do you know what I mean? So, it’s like not every company is complaining about this. So there’s other factors playing in as well.

Katie Martin

I guess where I land on this is like job insecurity and poor confidence among lower-income households and families like matters and is something to take seriously. But again, it’s not clear to me that this is new. Like America is pretty famous for this. All kind of rich economies are pretty famous for this.

So ultimately, who cares? As humans, we care that these people are having a tough time. Life’s tough on a low income with high prices. But ultimately what difference that make to markets or to monetary policy? Because again, like people who set interest rates for a living have always been incredibly mindful of income disparities and wealth inequality. So what?

Robert Armstrong

OK, so for companies, if it is true that people on lower incomes are being more cautious about their consumption because the future doesn’t look as bright to them, that’s gonna matter to certain companies.

Right? So you have to think about the companies who serve those populations and that’s a kind of stock by stock decision you have to make. The question of what a central banker should do in the face of this is very interesting because their mandate makes them ignore certain pieces of information. Like ultimately, what they’re supposed to look at is employment and the rate of inflation, right? And if the rate of inflation is above target, like it is now, and the rate of unemployment is still reasonably low. Then if they were to say: Look, poor people are suffering, we have to change our policy package here. They would be sort of exceeding their mandate.

Katie Martin

And if there’s one thing Maga don’t like, it’s the Fed exceeding its mandate. Like in a sense, no matter how hard the Fed tries not to be political, right. Just stay out of politics. Our job is monetary policy. We set interest rates. You kind of can’t help it. Like the outcomes of what monetary policy does have political implications. So it’s always political, whether it wants to be or not. I mean, who would be a central banker? Not me. Even if I were qualified.

Robert Armstrong

I don’t understand politics very well and I try not to go too far from markets land into politics land. But I will say that the stuff we’ve been talking about on this show, of course, is an incredibly live political issue that both sides of the American political spectrum care about tremendously. So remember, you can look at Trump’s policy set as an effort to speak to and help the people in that lower half of the wealth spectrum. Tariffs in theory …

Katie Martin

In theory …

Robert Armstrong

. . . are supposed to help those people get, in theory, and we can have all discussion are supposed to help those people get paid more. That’s supposed to bring high-paying jobs back to America to help those people.

Affordability is an issue for them. That he’s very, I mean, we, you, have Trump talking about sending out checks again this week. And at the same time, the Democrats who won several local and national elections last week, they’re talking about affordability too.

So the stuff we’re talking to today whether or not it’s relevant to markets and how, you can be damn sure it’s relevant to every politician. And so the fiscal policies will respond to this stuff even if monetary policy does not.

Katie Martin

Listeners, I don’t know if you agree but what I’m getting here is Rob Armstrong’s gonna run for president. Ladies and gentlemen, you heard it here first.

Robert Armstrong

Yes.

Katie Martin

He’s running.

Robert Armstrong

There is gonna be every household in America will be able to afford store-bought dishwasher tablets under the Armstrong administration. No more making your own dishwasher tablets.

Katie Martin

What a beautiful policy platform that is. Listeners, we’ll be back in just a couple of minutes for Rob to flesh out more of his policy platform with Long/Short.

[MUSIC PLAYING]

Okie doke. It is time for Long/Short, That part of the show where we go long a thing we love or short a thing we hate. Rob, what you got?

Robert Armstrong

I am long passive investing.

Katie Martin

Are you?

Robert Armstrong

And this is a very standard thing to be long among finance nerds like myself, but I’m gonna reiterate it because of this great story by our colleague Costas Mourselas. Elliott Management, which is a big hedge fund, had to explain in their letter recently why their performance, their returns, since 1994 have now fallen behind the returns of the S&P 500. And it’s a story as old as time that a big fancy hedge fund over time turns out not to outperform the index. But what is striking about this particular story is that Elliott Management is really good at this stuff.

They’re a very well run fund — activist investment fund — and even they, over a multiyear period, struggle to keep up with the old big cap US index. So once again, yay for just owning that tracker fund.

Katie Martin

I get my only counts point to that would be that like a tracker fund that tracks the US market is effectively an active fund that is leaning into Big Tech stocks. So there’s kind of no difference. They’re just …

Robert Armstrong

OK, fine, fine. Anyway, rain on my parade.

Katie Martin

I will.

Robert Armstrong

What do you have, Katie?

Katie Martin

I will. You can take your a vengeance when you’re president, although I could be like your chief of staff or something. Anyway.

I am short the story by our colleague Laith Al-Khalaf who wrote: Lloyd’s Banking Group, like a retail banking group in the UK, analyse data from the personal bank accounts of more than 30,000 employees to assess their financial resilience as part of pay negotiations. And I’m like: Am I the only person who thinks that’s a bit icky? Like …

Robert Armstrong

That just sounds like an unfair way to negotiate with your employees to me. Like you don’t tell me what my salary’s gonna be and the basis of how rich you think I am. You pay me because I’m doing work that’s worth something to you.

Katie Martin

I mean, I just find it odd that like it’s OK to aggregate and look at employees’ data in that way.

Robert Armstrong

Yeah. That story just makes me angry. I’m with you in short way.

Katie Martin

Yeah. I can’t quite articulate why I don’t like it, but I don’t like it. I find it weird.

On that note, we will wrap up there. Listeners, if you have adventures with dishwasher tablets or indeed there’s anything else we’ve mentioned in the show today, please get in touch: unhedged@ft.com. We will be right back in your actual ears on Tuesday.

[MUSIC PLAYING]

Unhedged is produced by Jake Harper and edited by Bryant Urstadt. Our executive producer is Jacob Goldstein. Topher Forhecz is the FT’s acting co-head of audio. Special thanks to Laura Clarke, Alistair Macky, Gretta Cohn and Natalie Sadler.

FT premium subscribers can get the Unhedged newsletter for free. A 30-day free trial is available to everyone else. Just go to ft.com/unhedged offer.

I am Katie Martin. Thanks for listening.