The reasons smaller companies have struggled go well beyond the rise of US mega-cap tech, according to fund managers.

Investing in mid-caps and smaller companies is supposed to mean taking on greater short-term risk for the prospects of much greater rewards over the long term. Yet over the past decade the latter half of that equation has been found wanting.

Most may be familiar with the outperformance of large-caps in the US, spearheaded by the Magnificent Seven, but America is far from the only market where the behemoths are outpacing the minnows.

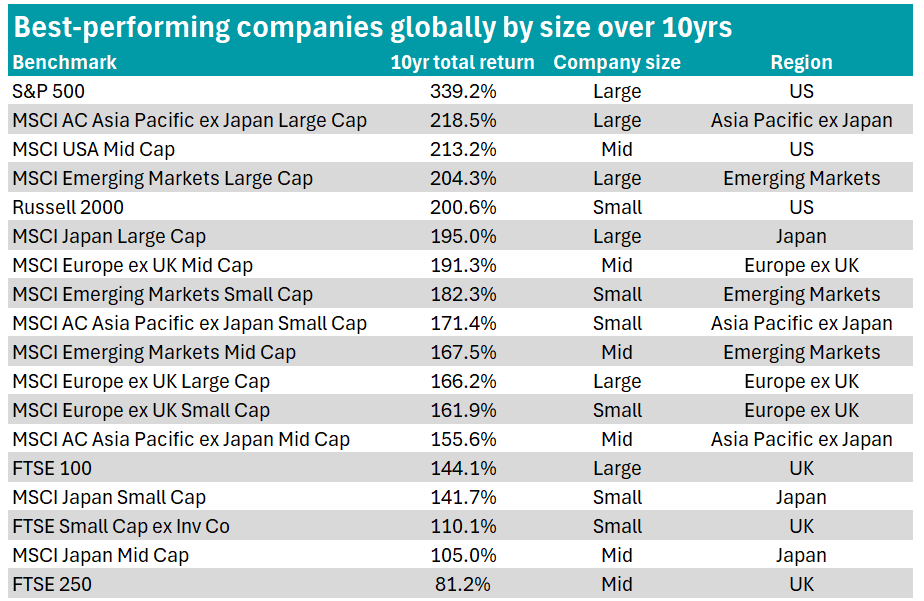

Trustnet analysed the 10-year total returns of 18 major global equity benchmarks to the end of May 2026.

As shown in the table below, in every single region bar Europe excluding UK, large-caps have outperformed their mid- and small-cap counterparts.

Source: FE Analytics

According to Richard Scope, manager of VT Tyndall Global Select, a major driver of this trend towards large-caps has been the shift towards passive investing, with US cap-weighted passive funds now accounting for 53% of all assets invested.

“The majority of assets invested in exchange-traded funds (ETFs) and passive funds are, by design, more weighted to large-caps, with many of the benchmarks that they are designed to mimic excluding small- and mid-caps, which exacerbates the issue,” he said.

In addition, Philip Matthews, manager of IFSL Wise Multi-Asset Income, said valuation expansion has been a “clear contributor to the success of large-caps, rather than fundamentally superior earnings growth”, with investors concentrating capital in a narrower group of large companies perceived to offer safety and structural growth.

Mark Ellis, chief executive officer and chief investment officer at Nutshell Asset Management, added: “The simple answer is that the past decade has disproportionately rewarded scale.

“Across most regions, the companies that have been able to compound earnings, defend margins, access capital cheaply and reinvest globally have tended to sit at the larger end of the market-capitalisation spectrum.”

He said it is less a story about size and more about quality, resilience and scalability being rewarded.

While these structural forces have supported larger companies across regions, several managers argued that the picture in the US is distorted by a narrow group of winners at the very top of the market – the mega-cap tech stocks also known as the Magnificent Seven.

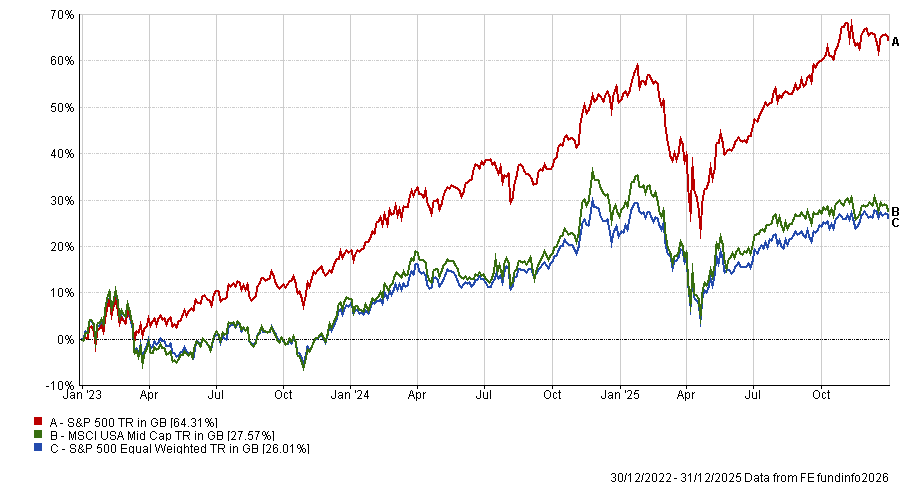

According to Sagar Thanki, co-manager of Guinness Global Quality Mid Cap, it is “not really a large-cap story at all, but a mega-cap one”, noting that the equal-weighted S&P 500 lagged the mega-cap-weighted index by almost the same margin as mid-caps between 2023 and 2025.

Performance of S&P 500 vs S&P 500 equal-weighted and MSCI USA Mid Cap, 2023 – 2025

Source: FE Analytics

Paul O’Neill, chief investment officer at Bentley Reid, said that although technology advancements propelled these seven companies higher and faster than anyone else, technology has had a farther-reaching impact on large-caps across the world as they “no longer have to adhere to physical borders, and data capture has enabled them to offer better, cheaper products and services to their client base”.

Justin Warton, portfolio manager at ECP Asset Management, agreed, noting that digital business models have increasingly “raised the upper bound of scale economies and allowed the largest companies in the world to continue to grow quickly, despite their size”.

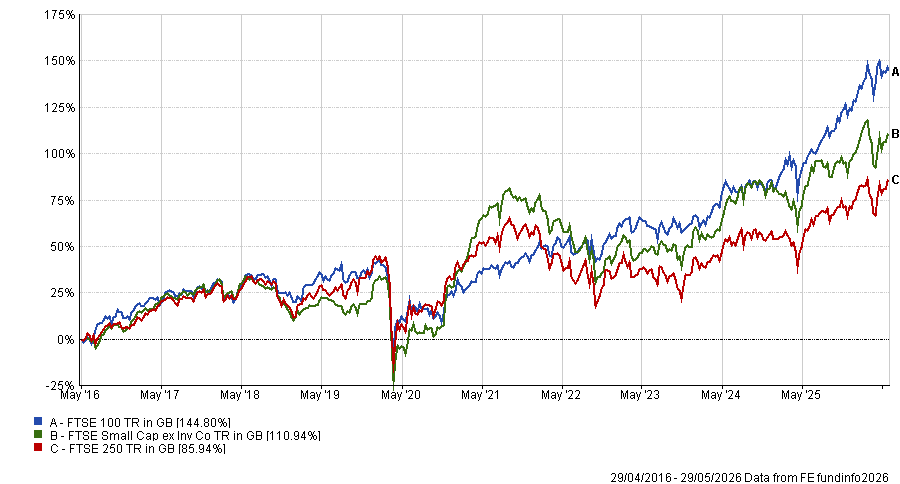

But technology is not the only driver of success, as the UK’s large-caps have also logged a similar pattern despite lacking a cohort of technology giants.

The FTSE 100 gained 144.1% over 10 years, while the FTSE Small Cap excluding Investment Companies index returned 110.1%. The FTSE 250 was the worst-performing index of all 18 assessed, gaining 81.2% over 10 years.

Performance of UK companies over 10yrs ending May 2026

Source: FE Analytics

Managers said UK large-caps have simply proven more resilient in a challenging landscape defined by Brexit uncertainty, political instability, weak capital flows into UK equities, higher interest rates, pressure on the consumer and a de-rating of UK-listed assets.

Ellis said: “Many FTSE 100 companies are global businesses earning revenues outside the UK, so they were less exposed to the domestic backdrop.”

While regional differences explain some of the dispersion, the challenges facing smaller companies themselves have also contributed to the widening gap.

Managers pointed to reduced research coverage and a tougher environment for lower-quality or more financially sensitive businesses as key headwinds for smaller companies.

O’Neill highlighted an additional structural shift for small-caps specifically, which is that many smaller companies are delaying listing.

“Smaller companies now have access to all sorts of capital outside of the equity markets,” he said. “That means they can stay private for longer and, when they do come to market, they are often mid- or even large-cap companies already – hence the reduction in the number of small-cap floated companies and therefore a reduced opportunity set.”

Even as the headline data would suggest a higher return is up for grabs when investing in large-caps, several managers argued that pressures on the small- and mid-sized market have created appealing opportunities.

Matthews said: “Historically, periods of extreme small-cap underperformance have often been followed by periods of strong relative returns.”

He added that many smaller companies now appear attractively valued in absolute terms relative to their own history.