The IMF’s headline writers were clearly in a glum mood when they named the fund’s latest World Economic Outlook. “Global economy in flux, prospects remain dim” is hardly cheery. In a year when the US raised tariff levels to the highest in a century and adds new threats whenever something displeases President Donald Trump, you would not expect the IMF to be upbeat. But it is exaggerating.

A more accurate summary is that the world economy is simultaneously resilient and fragile. It is this paradox that central bankers and other economic policymakers need to address.

Resilience

The most notable feature of the global economy in 2025 has been its ability to withstand trade shocks. Although rich-world households are pretty gloomy, the composite Brookings-FT Tiger indices show that most real and financial indicators across advanced and emerging economies are faring better than usual.

As Eswar Prasad, senior fellow at the Brookings Institution, said: “Economic growth has been surprisingly stable in most corners of the world, despite enormous uncertainty in global trade and geopolitics, as well as various short-term and looming long-term pressures that each economy faces.”

This unexpected strength is reflected in the IMF’s latest forecasts. Compared with the last full outlook in April, global economic growth in 2025 has been revised 0.4 percentage points higher to 3.2 per cent, exactly the level the IMF was forecasting both a year ago and a year before that.

Nearly every country has seen growth forecast upgrades for this year, many of them sizeable. Part of the improved outlook has been the result of less retaliation against Trump’s tariffs than feared, meaning their effect has mainly amounted to a tax on US imports. The remainder of the upgrade has resulted from strong financial markets, adaptation in the private sector and stronger economic policies.

The IMF is so encouraged by economic policymaking in emerging markets that it devoted a chapter to its success. It concludes that better policies have “played a critical role in bolstering the capacity of emerging markets to withstand risk-off shocks”, adding that they demonstrated “remarkable resilience” during the Covid-19 pandemic and subsequent inflation shock.

This celebration needs some context, however. As recently as two years ago, the IMF highlighted that economic activity in emerging markets was falling far short of pre-pandemic expectations, and that they faced much larger scars from Covid-19 than advanced economies.

When it comes to the IMF, storytelling trumps consistency.

The IMF exaggerates global weakness

The story the IMF wants you to believe in 2025 is this: before the pandemic, the global economy was going gangbusters with average annual growth of 3.7 per cent. Now, economic activity is forecast to rise at an annual rate of only 3 per cent over the medium term, which is “decisively” lower and will usher in “persistently lacklustre” output growth for the rest of this decade.

Alas, this new narrative relies on some selected statistics. The numbers are true, but not fair.

The reality is that the pre-pandemic average growth rate was 3.4 per cent when using the full set of data in the IMF database, not 3.7 per cent. The higher figure relies on giving much more weight to the boom years before the global financial crisis and limiting the sample to 2000-2019. The 3 per cent medium-term future growth rate relates to the average over six quarters, starting in the second half of 2025 to the end of 2026. After that it climbs back to an average of 3.2 per cent a year, which is hardly lower than the long-term average.

Disappointment, not fragility

It is hard to fathom why the IMF keeps underplaying the strength of global economic activity, because the full truth is easy to explain. Growth rates are holding up because emerging economies account for an ever-increasing share of global output, and they have been growing faster than advanced economies for decades.

But while this feature of the global economy maintains the overall rate of expansion, it also allows for all regions to be disappointed with their performance.

As the chart below of successive IMF forecasts shows, advanced economy medium-term growth predictions have declined from around 3 per cent in the 1990s to less than 2 per cent. Emerging economy annual growth rate forecasts rose in the 1990s and 2000s. But since the global financial crisis, they have declined from over 6 per cent to 4 per cent.

The paradox here is that everyone is disappointed. But because the centre of global economic gravity has moved so decisively towards faster-growing emerging economies, the global growth rate remains roughly constant.

Genuine fragility

To give a rounded view of the global economic backdrop, analysis of countries’ growth rates since the global financial crisis should be combined with evidence of genuine economic fragility.

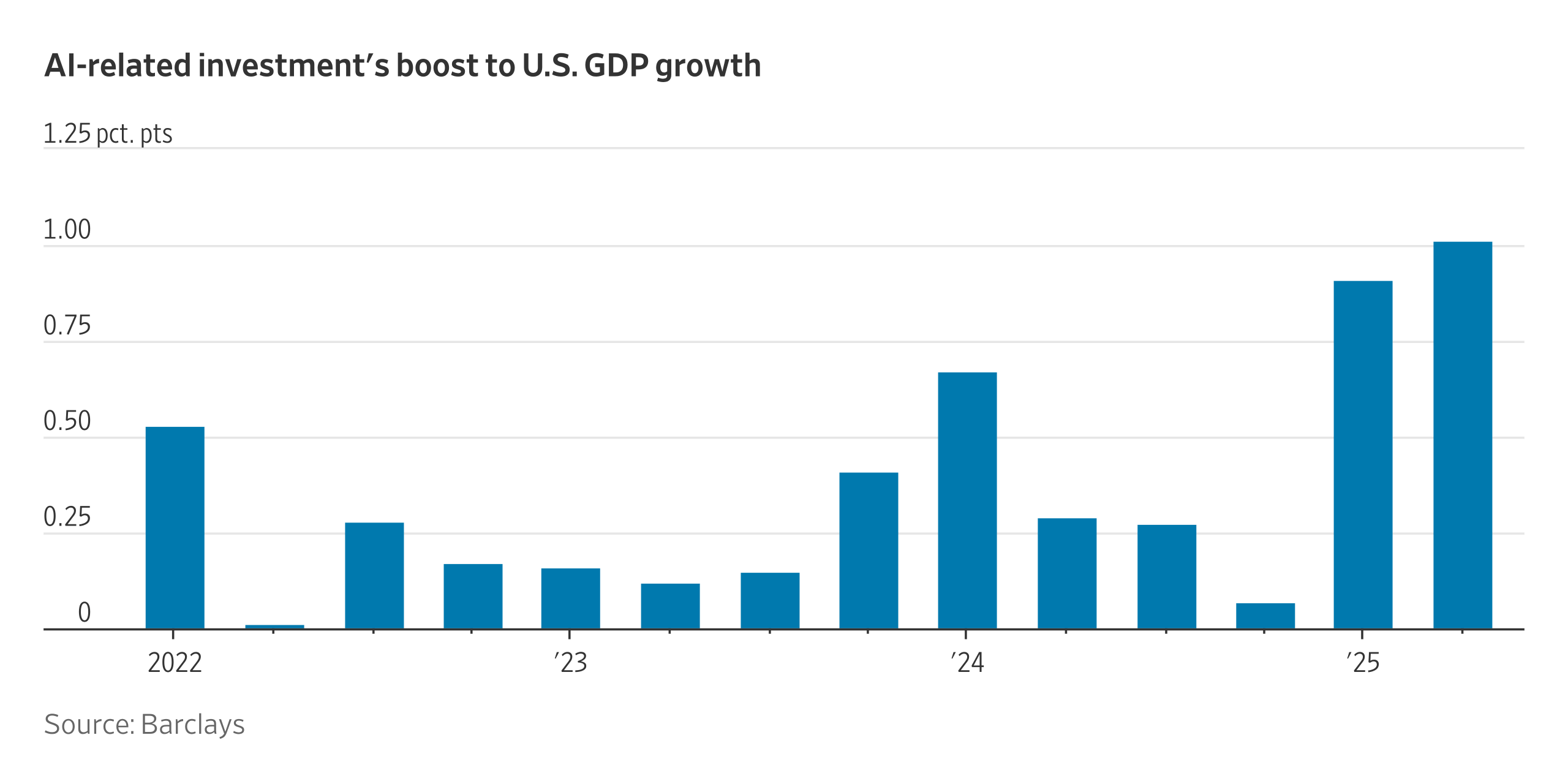

Trade policy is in flux, as demonstrated by China’s announcement of rare earths export controls last week and Trump’s furious reaction. Like everyone else, the IMF is worried the artificial intelligence investment boom and associated financial market equity surge might be a bubble. Fiscal policy is loose globally and financing strains are emerging, even if they have been quelled by higher yields. Japan and the US in particular have very high funding needs, given the size of their public debt and its short average maturity.

As IMF managing director Kristalina Georgieva said, given these problems, it is time for policymakers to “get the house in order”. On this, the IMF is entirely right.

What I’ve been reading and watching

-

Former senior European Central Bank official Natacha Valla worries that France’s fiscal and political woes will soon test the central bank.

-

In the past it has been difficult to stop UK consumers splashing their cash. Now they have become prudent savers, confusing everyone.

-

The economics Nobel goes to Joel Mokyr, Philippe Aghion and Peter Howitt for explaining innovation-driven growth.

-

Meanwhile, US Treasury secretary Scott Bessent has been grilling Federal Reserve chair candidates about quantitative easing. He wants less of it.

One last chart

A few days before the IMF’s worrying about fiscal fragility, the US Congressional Budget Office published the first budgetary outcome for the 2025 fiscal year, which ends in September.

The chart below shows US fiscal fragility in gory detail. Net debt interest accounts for more than 15 per cent of tax revenues, back to the level of the 1980s and 1990s. Back then, however, debt was much lower as a share of GDP. The risk is that market interest rates rise further, which would make servicing the US’s debt even more expensive.

Central Banks is edited by Harvey Nriapia