Wall Street rose at the opening bell on Thursday, after strong earnings from AI chipmaker TSMC (TSM) and banks Goldman Sachs (GS) and Morgan Stanley (MS) signalled a recovery from back-to-back losses, while the FTSE 100 (^FTSE) hit a new all-time high, adding to its gains since it broke through the 10,000-point mark at the start of this year.

The mood marks a reversal after tech led stocks lower on Wednesday, which dragged on indexes and promised to revive a weeks-long rotation out of megacaps into value names.

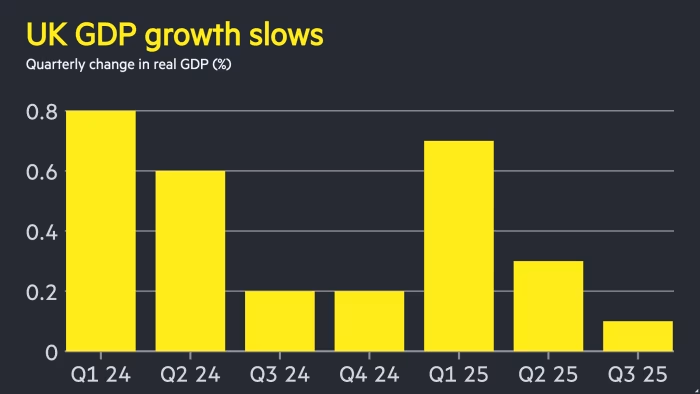

However, European stocks were mixed as the UK economy beat forecasts and grew by 0.3% in November thanks to car production rebounding and a boost from the services sector.

According to the Office For National Statistics (ONS), the figures were helped by the return to production at Jaguar Land Rover’s facilities after a cyber-attack at the carmaker.

Read more: UK economy grew by more than expected in November despite budget uncertainty

November’s growth figure was stronger than analysts’ expectations of a 0.1% increase, and in another boost, September’s growth figures were revised higher, showing that the economy did not shrink that month after all.

The UK’s services sector, which makes up around three-quarters of the economy, expanded by 0.3% during the month, while production also grew, with output rising by 1.1%. However, construction shrank by 1.3%, with builders reporting a drop in new work, and repair and maintenance.

Yael Selfin, chief economist at KPMG UK, said the figures showed economic activity had accelerated despite uncertainty in the lead up to the budget.

“Despite the relatively mooted consumer sentiment so far and consumer-facing services output declining in November, there are some tentative signs of a pick-up in household spending,” she said.

“With the worst of the uncertainty behind businesses, we expect growth momentum to continue over the coming months.”

The news means an interest rate cut from the Bank of England next month is less likely. Traders are betting there is a 6% chance of a reduction in borrowing costs in February, down from 7% on Wednesday.

Money market pricing indicates policymakers are expected to cut rates in April, although the chances of this were reduced from 93% yesterday to 91% today.

Joshua Mahony, chief market analyst at Scope Markets, said: “The FTSE 100 once again remains a leader in Europe, although the pullback in oil and precious metals has meant that commodity stocks are lagging behind as financials take the lead. Strong gains for the likes of HSBC, Barclays, and NatWest bring a recovery from a sector that has been hit by Trump’s recent move to limit credit card interest rates to 10%.”