The challenges facing the Scottish economy were highlighted again last week in the latest official gross domestic product figures.

Data published by the Scottish Government’s chief economist directorate showed the nation’s onshore GDP contracted by 0.3% month-on-month in July. In the UK as a whole, GDP was flat in July.

However, before those who delight in adversity for Scotland for political reasons allow themselves a smug grin, a few points are worth noting.

Clearly, the economic fortunes of Scotland are inextricably linked to those of the rest of the UK. That should go without saying.

The UK economy has for many years now, long before Labour came to power, been struggling. And Brexit continues to compound the UK economy’s woes hugely.

It is good to see senior Scottish Government figures continuing to point out the enormous Brexit effect.

After all, while the Brexiters would like to paint a picture of the caravan having moved on, the damage from their folly remains very much an ongoing thing.

Another point to make in the context of the July GDP data for Scotland is that figures for a single month, while interesting and clearly newsworthy, are volatile.

In this context, the three-month-on-three-month growth rate comparison between Scotland and the UK as a whole paints a different picture to that formed when the July figures are looked at in isolation.

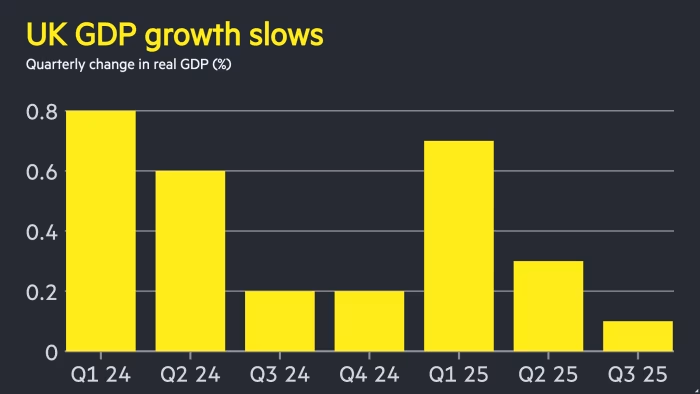

Comparing the three months to July with the February to April period, Scottish onshore GDP was up by 0.5%. This marks an acceleration of quarter-on-quarter growth from 0.2% in the three months to June.

Read more

The data published by the Office for National Statistics on September 12 for the UK as a whole showed GDP in the three months to July was up by 0.2% on the February to April period.

The latest Scottish Government figures revealed the month-on-month rise in onshore GDP north of the Border in June has been revised up from 0.6% to 0.7%.

And there were some positives in the breakdown of the month-on-month fall in Scottish GDP in July, albeit there were obviously negatives as well.

Starting with the negatives, electricity and gas supply, a volatile component, was responsible for the biggest downward effect. Overall production sector output dropped by 2.3%.

However, the services sector grew by 0.1%. And construction output rose by 0.2%.

Sadly, the outlook for the overall UK economy is weak.

Thomas Pugh, chief economist at accountancy firm RSM, said in the wake of the UK GDP figures: “The flatlining of GDP in July raises a sense of déjà vu with last year when the economy grew rapidly in the first half before stagnating through the second. Indeed, the growth outlook is more challenging for the rest of the year. Rising inflation, a weakening labour market and confidence-sapping speculation about the Budget will combine to slow growth from 0.5% q/q in the first half of the year to around 0.2% q/q in the second.”

Matt Swannell, chief economic advisor to the EY ITEM Club think-tank, said of the UK economy at that stage: “Though July’s reading was a better outcome than had appeared likely, the outlook contains few bright spots. Some of the sectors that grew strongly in June outperformed again in July, such as distribution and arts and recreation, so there’s likely to be some payback soon. GDP growth will likely be very modest in Q3 and remain sluggish in the final months of this year, which would be consistent with the seasonal pattern seen in recent years.”

He added: “The economy is expected to continue growing at sub-trend rates next year, with our pessimism largely based on the strength of domestic headwinds. Fiscal policy is already set to tighten next year, and the Government will likely need to tighten policy further in the autumn to remain compliant with its fiscal rules. Household finances are likely to be squeezed by elevated inflation and slowing pay growth, which will weigh on consumer spending power. Meanwhile, the lagged impact of past interest-rate rises is likely to impose a similar drag on the financial position of some mortgagors.”

Suren Thiru, economics director at the Institute of Chartered Accountants in England and Wales, said: “July’s slowdown is probably the start of a more restrained period for the economy with higher inflation and rising job losses likely to have stifled activity in August, despite an expected uplift from the warm weather.”

Faced with this difficult outlook, and with the UK Budget looming large and not in a good way it seems, all the Scottish Government can do is use its devolved powers to best effect in these challenging times.

It has had recent successes on this front, including its innovative multi-million-pound package aimed at preventing the closure of the Scottish manufacturing operations of bus builder Alexander Dennis, which would have triggered hundreds of job losses.

Scotland also, most encouragingly, has continued to punch well above its weight on the foreign direct investment front.

This is always particularly heartening because such investment decisions are based on a cold analysis of the merits of Scotland as a place to do business, relative to other places.

So, while it is important for households and businesses to be aware of the difficult economic outlook and what that might mean for them, it is crucial to bear in mind that the situation is far from universally bleak.