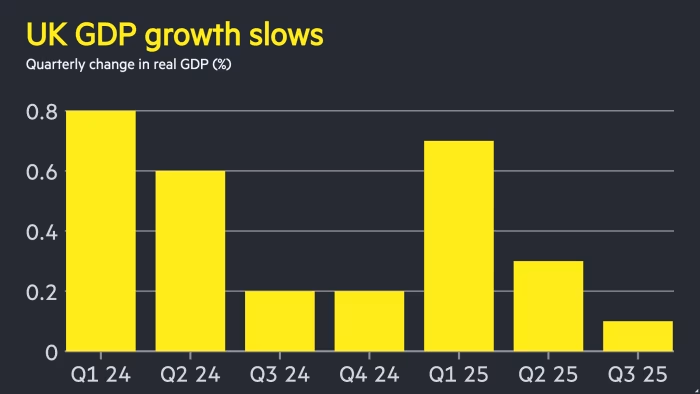

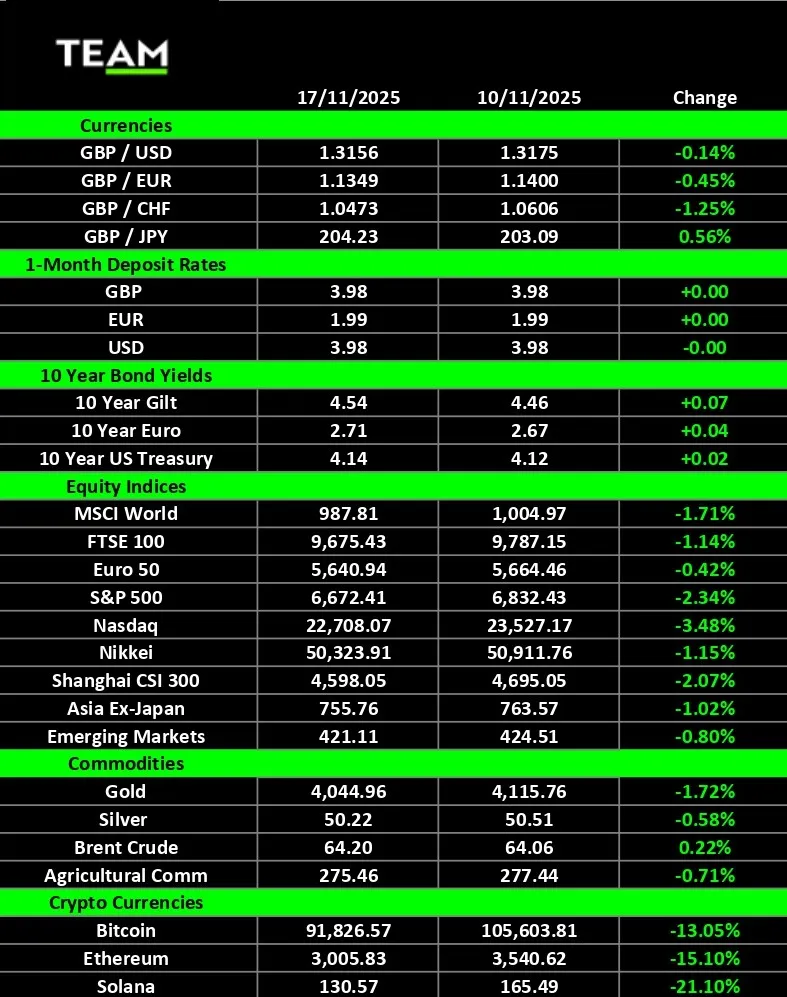

European markets are showing their relative resilience today, with the moderate losses seen this morning standing in stark contrast to the 2% declines seen for tech heavy indices such as the Nasdaq, Nikkei 225, and Hang Seng. On the data-front, this morning has seen concerning UK figures on both the PMI and retail sales front. Retail sales figures slumped by -1.1% for the month of October, marking the worst consumer activity since May. Meanwhile, a decline in the services PMI meant we saw the composite figure drop back from 52.2 to 50.5. That PMI report made for concerning reading, with job losses on the rise and business confidence waning. This is a release consistent with a 0% November GDP figure, highlighting the impact being felt be pre-budget chatter that has essentially seen the UK economy grind to a halt. In a week that has seen UK inflation fall back down to 3.6%, the weakness evident today will likely put further pressure on the BoE to act next month.

Yesterday’s Nvidia bounce appears to have been short-lived, with the concerns evident around valuations coming back to haunt big tech once again. Central to the wider market decline was the Nvidia swing from +5% at the open, to a 3% decline. There had been a hope that Wednesday’s earnings will have drawn a line under the recent selling pressure, building a narrative that the dip buyers were set to step in. However, one key element that has been central to the recent declines have been around Michael Burry’s short positions and promise to shed further light on Tuesday (or before). That provides a major hurdle that lies ahead, with traders likely to remain cautious until we see all the details he says will shed light on the so-called “fraud” within accounting in the tech space. Nonetheless, for the optimists, it is worth noting that the past two Friday sessions have seen a strong close to the week. Will we see the same today?

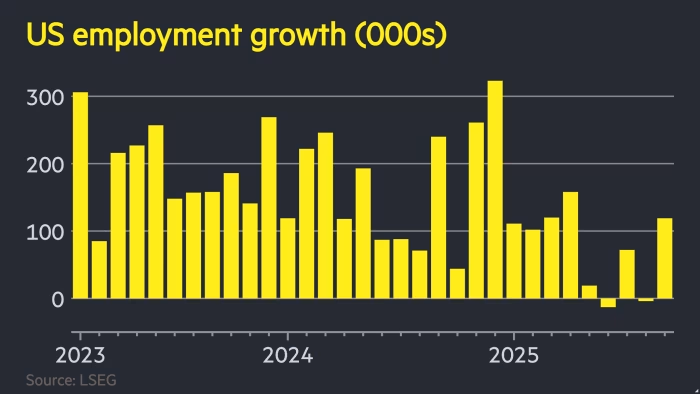

Today brings fresh PMI data, coming hot off the heels of yesterday’s jobs report that brought a little for everyone. The payrolls beat of 119k was accompanied by a mark-down for the August figure which has dropped into -4k. Unfortunately, the pattern seen over the past eight months does highlight the fact that this 119k figure will more than likely get revised lower in the future. Meanwhile, the rise in unemployment can be partly explained away by a rise in the participation rate, which actually is a signal of relative health if people are returning to the workforce. After-all, the U6 total unemployment rate did decline in September. Markets are now pricing a 65% base case scenario that the Fed keep rates steady next month, with the hawkish FOMC minutes signalling that inflation remains a key concern despite recent weakness within the jobs market. Whether today’s PMI report will shift that narrative remains to be seen, although those hoping for a rebound for equity markets can at least look back to the past two Friday’s price action.