This article first appeared on GuruFocus.

Stablecoins have evolved from an experimental asset to a key component of the global payment system at an unprecedented pace. According to data, the annual transaction volume of stablecoins has surged from $3.3 billion in 2018 to $18.4 trillion in 2024, surpassing the transaction volumes of traditional payment giants Visa ($15.7 trillion) and Mastercard ($9.8 trillion). As Visual Capitalist points out, this milestone not only signifies the transformation of stablecoins from niche experiments into mainstream payment infrastructure but also highlights their central role in the future financial ecosystem.

From 2023 to 2024, several landmark events have acted as catalysts for the rise of stablecoins. Citigroup partnered with Coinbase to extend digital asset payment solutions for institutional clients, opening a new chapter in digital asset adoption; nine major European banks formed a consortium to issue a Euro-backed stablecoin, with plans to launch in 2026; Western Union announced plans to issue USD-backed stablecoin USDPT on the Solana blockchain, with Anchorage Digital Bank overseeing issuance and custodial services; and Visa revealed it would support settlements on four new blockchains and four stablecoins, further consolidating its leadership in global payments.

On the capital front, Mastercard is also making significant moves, with plans to acquire stablecoin and crypto infrastructure provider Zero Hash for $1.5 to $2 billion, alongside ongoing talks to acquire BVNK, a UK-based fintech platform, from Coinbase.

As traditional financial institutions embrace digital assets, they are faced with two distinct pathways: stablecoins and tokenized deposits.

Tokenized deposits, as an internal digital solution, allow banks to convert customer deposits into digital tokens, operating within existing regulatory frameworks while seamlessly integrating with traditional clearing systems. Citigroup’s CEO, Jane Fraser, emphasized that tokenized deposits represent a safer and more compliant choice for banks.

However, with the rapid growth of the global crypto market, banks recognize the need to connect with public blockchains and crypto ecosystems, making stablecoins an inevitable option. Citigroup’s partnership with Coinbase highlights this dual approachleveraging tokenized deposits for compliance while also integrating stablecoins to connect with the broader crypto ecosystem.

In Europe, nine major banks have teamed up to advance the Euro-backed stablecoin project, with a design emphasizing “1:1 reserves” and public blockchain interoperability to counter the dominance of USD-backed stablecoins in the European market.

While banks focus on core payment infrastructure, cross-border payments giant Western Union sees stablecoins as a way to upgrade its retail remittance network. Western Union has integrated USD-backed stablecoin USDPT with the Solana blockchain, leveraging its high throughput and low transaction fees to optimize high-frequency, low-value cross-border remittances.

For users in developing countries without bank accounts, Western Union offers a seamless solution for converting digital funds into local cash, improving user experience and reducing transaction costs. Western Unions strategic core lies in combining blockchains efficiency with its vast network of physical locations, providing fast, low-cost remittance services to users globally.

Visa has transformed into a “multi-chain settlement router,” supporting settlements on multiple blockchains and with various stablecoins. Its latest earnings report highlights a surge in card transactions linked to stablecoins, underscoring its role in connecting traditional bank accounts with blockchain-based funds across different networks.

Mastercard, on the other hand, is accelerating its stablecoin strategy through acquisitions. By acquiring Zero Hash, Mastercard will quickly enhance its capabilities in crypto settlement, custodial services, and clearing. The company is also in discussions to acquire BVNK, aiming to integrate these technologies into its global payment network at an accelerated pace.

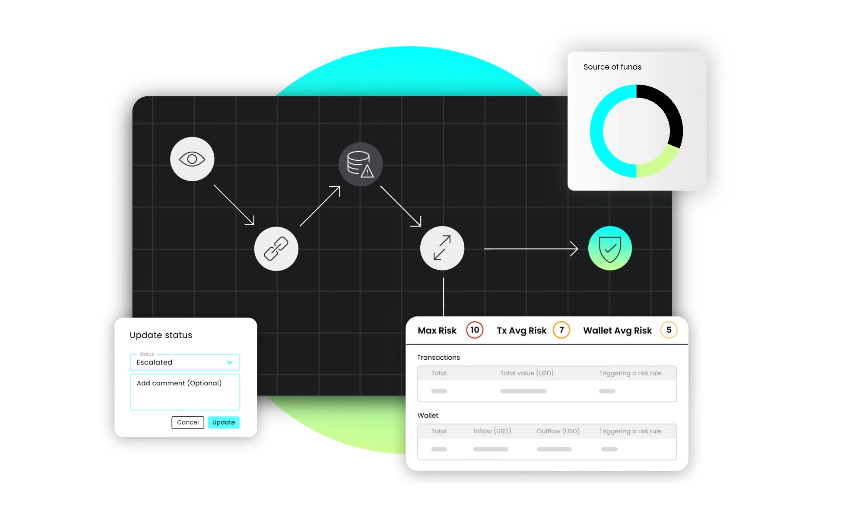

As a key provider of stablecoin and crypto settlement infrastructure, NB HASH is emerging as a crucial player in the future of payment networks. NB HASH focuses on solving the technical challenges of on-chain payments, offering a comprehensive range of solutions, including stablecoin custody, clearing, and compliance services. Through continuous innovation and strategic partnerships, NB HASH is playing a pivotal role in driving the transformation of global financial infrastructure.

Despite the rapid adoption of stablecoins by global payment giants, significant challenges remain:

-

The “Digital Dollarization” of Stablecoins: Governments around the world are concerned about the regulatory implications and loss of monetary sovereignty if USD-backed stablecoins dominate payment systems. This concern has led to the development of regional stablecoins, with Europe, in particular, pushing for local solutions to maintain control over their currencies.

-

On-Chain Stability and Trust Issues: Ensuring that stablecoins remain resilient during a “bank run,” liquidity crises, and technological failures is a core challenge for the industry. The stability of reserve assets, network congestion, and vulnerabilities to cyberattacks must be addressed.

-

Compliance and Legal Risks: For companies like Western Union, which bridge the gap between digital assets and physical cash, complying with complex anti-money laundering (AML) regulations and securing multi-jurisdictional operating licenses are significant barriers. These non-technical challenges make it difficult for traditional financial institutions to integrate stablecoins and blockchain technology.

The rise of stablecoins is not merely a triumph for the crypto industry but represents a silent revolution in global financial infrastructure. As banks, payment giants, and cross-border remittance companies increasingly integrate stablecoins into their offerings, the future payment system will become more decentralized, efficient, and seamless, with the lines between on-chain and off-chain transactions blurring. Innovations from infrastructure providers like NB HASH will play a critical role in supporting this transformation, propelling the financial services industry into a new, digital-first, globalized era.