They may not be Central Park-sized data centres issuing enormous wads of investment-grade paper under pastry-themed code names, but the world’s frontier sovereigns have also issued a lot of dollar bonds this year.

Just in Africa in recent weeks, that has included Angola, Kenya and Nigeria and Republic of Congo. (A eurobond from the latter was last seen in 2007.).

Some of these countries didn’t have market access until recently. Some, really, only just still have it, having sold their bonds with coupons in the region of 9 to 10 per cent, the danger zone where interest bills over the life of a longer bond start to outweigh the principal. Still. The market is seeing bonds from countries it doesn’t see very often.

So, when the Lao People’s Democratic Republic came to market last week to sell a bond with a mere 11.25 per cent coupon atop a CCC+ credit rating, it wasn’t a surprise.

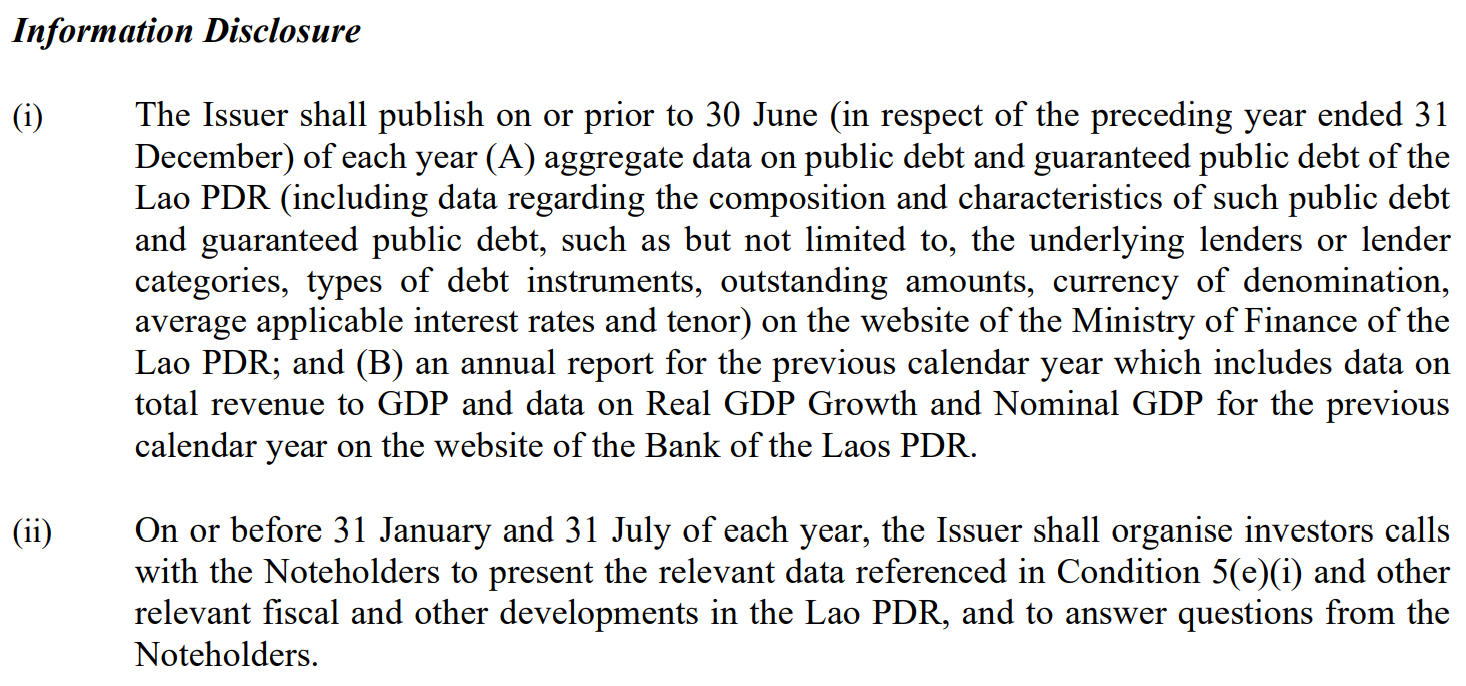

What was a surprise was the presence of a shiny new debt-disclosure clause in the prospectus (high-res):

The Laos finance ministry didn’t respond to a request for comment.

It may not sound like much — a requirement to disclose figures and get bondholders on a call every now and then. But these so-called reporting covenants are taking hold in frontier sovereign debt.

They started to appear in the restructured bonds of countries that had drawn-out defaults and/or fights over disclosure among Chinese, private, and other creditors earlier this decade, such as Ghana and Sri Lanka.

Laos, Republic of Congo and one or two other countries seem to be among the first to include these clauses in bonds outside a restructuring.

That’s good, isn’t it? In a world of #PublicDebtIsPublic and the fallout of hidden loan scandals from Mozambique to Senegal, who doesn’t like more transparency?

The recently launched London Coalition on sustainable sovereign debt has also focused on transparency clauses. Not every emerging-market government will be interested in using them because many already hold regular updates and roadshows with investors. But for smaller or less familiar countries it is on paper an important obligation.

But is there a risk these clauses might become boilerplate that leaves other context on a country’s debt position a mystery?

The Laos bond has some warnings, particularly because it is a country that is highly reliant on debt relief from China, which rarely volunteers details on how this works for sovereign borrowers.

We should firstly note that the Laos bond sale apparently didn’t go very well. The coupon priced at the initial 11.25 per cent, indicating there was not much demand.

Laos also just scraped into ‘benchmark size’ that qualifies it for access to indices and the big pools of capital that follow them. Issuance totalled $300mn, which is just big enough for inclusion in a JPMorgan index of Asian dollar bonds outside Japan, but not the bank’s much larger index for sovereign debt across emerging markets, which needs $500mn.

There are reasons investors might have been cautious. The so-called ‘battery of south-east Asia’ owes around $14bn in debt, or nearly the size of its economy, as it has built Mekong river basin hydropower projects to reinvent the most bombed country per capita in history into Asean’s biggest exporter of electricity.

That means the country is due to repay $1.2bn a year on average for the rest of this decade. Although Fitch estimates that within this, China could defer about $500mn a year in payments, you can probably expect a lot more Laos paper in the years ahead to refinance this debt.

And in that context, the transparency has limits. When it comes to Chinese loans in future, investors are told that they “may have limited visibility into agreements reached between the Lao PDR and other sovereign lenders concerning debt refinancing or restructuring.”

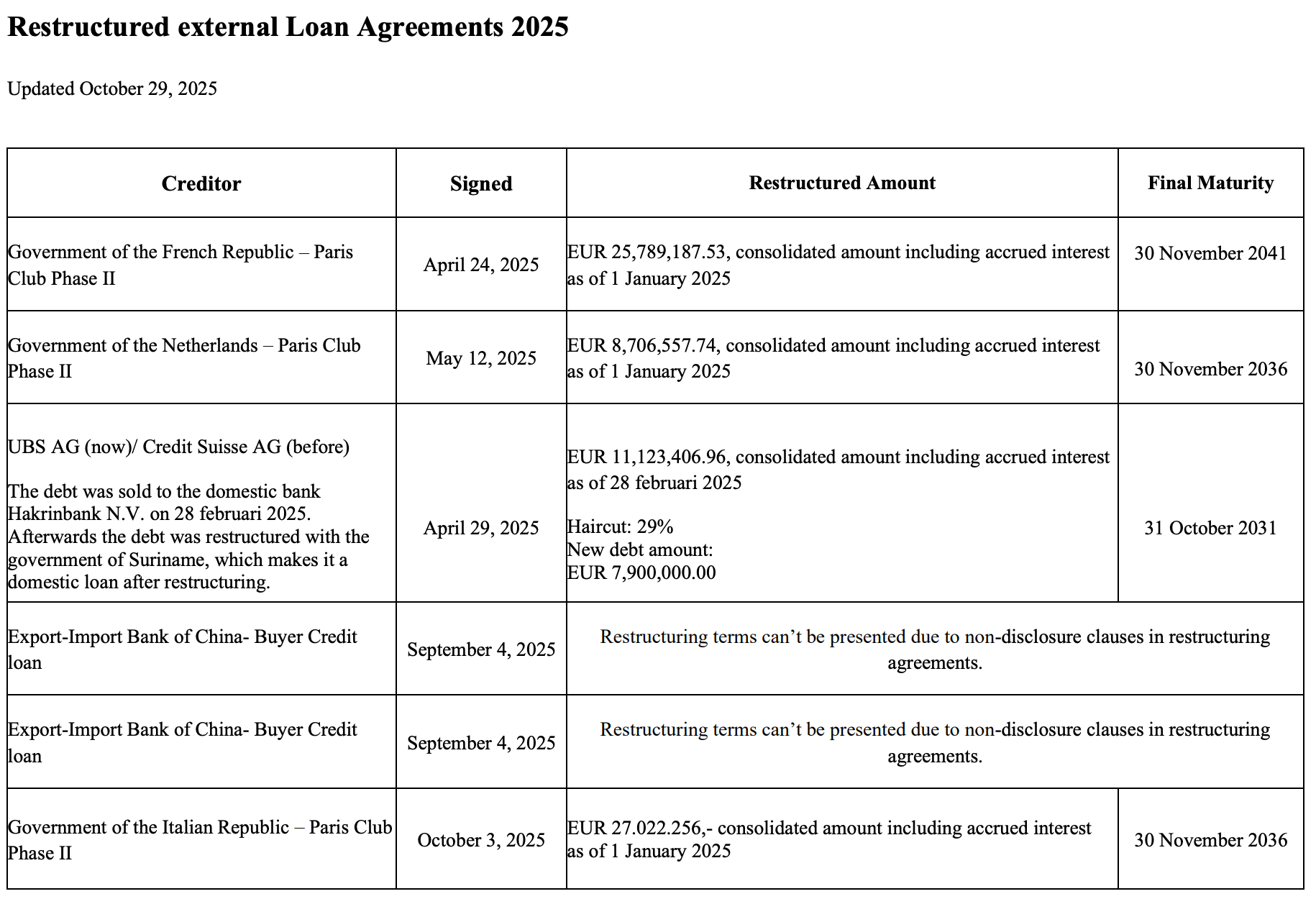

Laos isn’t alone in this. Suriname has also pioneered debt disclosures since its 2023 restructuring. But this also hits a limit with one particular creditor (high-res):

There are other debt mysteries in, or not in, the Laos prospectus. As for further spending on hydropower projects on top of Laos’ current 12GW capacity — the underlying debt driver — investors are told:

Although the authorities are taking steps to encourage a transparent public debate over such projects and the Government has also deployed a debt monitoring system, there can be no guarantee there will be sufficient capacity in debt management or suitability of debt sustainability analysis or project viability appraisal.

But isn’t the debt disclosure clause meant to be some guarantee of debt management capacity?

All that said — there is one disclosure by Laos that is comprehensive and detailed, and to be commended!

It’s about a risk to bondholders that sounds remote but is quite interesting given the big issue of official lenders who lend against opaque collateral in the developing world. Chinese policy banks are famous for having secured loans with cash escrow or commodity export revenues. Here they seem to be on the receiving end for once.

It’s worth sharing nearly in full (emphases ours):

In 2014 the Lao PDR granted security over certain of its assets in connection with a loan obtained for the financing of the Nam Ngiep 1 Hydropower Project and the Xe Pian-Xe Namnoy Hydropower Project . . . Several of the Lao PDR’s external loan agreements contain negative pledge clauses effectively prohibiting the granting of security over the Lao PDR’s assets, the lenders under which are China Exim PBC, Asian Development Bank (“ADB”), Export-Import Bank of Thailand and a syndicate of commercial banks. The Government has informed the lenders of the relevant external loans (the “Relevant Lenders”) that it has granted the aforementioned security and has undertaken attempts to remediate any potential breaches of the negative pledge clauses resulting from the granting of such securities, such as seeking waivers from the Relevant Lenders, although no explicit waivers have been received to date…

None of the Relevant Lenders has declared a default or accelerated payment under any the relevant loan agreements since the entry into by the Government of the Hydropower Project Loans in 2014, nor has any Relevant Lender given any notice or indication to the Government that it intends to do so. The Lao PDR has been timely servicing the relevant external loans, and the Government currently does not expect any such declaration. ADB and the Government engaged in dialogue to understand the nature and scope of the matter, resolving it with an agreement in 2022. China Exim PBC and Export-Import Bank of Thailand are development banks with which the Lao PDR has a long-standing relationship and which have the objective of supporting the Lao PDR’s development.

Notwithstanding the foregoing, there remains a remote possibility that Lao PDR’s non-compliance with the relevant negative pledge provisions could result in an event of default under the relevant loan agreements leading to acceleration of the relevant loans. In addition, such non-compliance could result in an event of default leading to cross acceleration under the Lao PDR’s other financing agreements. In the event that any of the Relevant Lenders initiates any remedial action for the Lao PDR’s non-compliance, the Lao PDR may be unable to repay or refinance the Notes or any other defaulted indebtedness referred to above. Furthermore, for so long as such non-compliance exists, it may be difficult for the Lao PDR to obtain further financing from other lenders…

Firstly this would be a reminder that a negative pledge in sovereign debt is itself often boilerplate which no one notices until it is breached. Laos bondholders of course do get an 11.25 per cent coupon for this disclosed risk.

Many other countries however will probably have offered security on loans on shady terms in recent years, with obscure implications for their negative pledge obligations to other lenders.

Transparency clauses or not, we wonder how much will be disclosed in the years ahead.

{kind=link}

{kind=link}