For resident shareholders, dividends are added to their total income and taxed according to their applicable income tax slab rates. This means that individuals in the lower income brackets pay less tax on dividends, while those in the higher brackets pay more.

Dividends are taxed under the head ‘Income from other sources’. A specific deduction is permitted: shareholders may claim interest expenses incurred on borrowed funds used to purchase such shares, but only up to 20% of the total dividend income. Other expenses such as brokerage, commissions, or service charges are not deductible.

Suppose a resident shareholder receives Rs.1 lakh as dividend income and pays Rs.35,000 as interest on a loan taken to buy the shares, the maximum deduction allowed is Rs.20,000 (20% of Rs.1 lakh). Therefore, the taxable dividend income will be Rs.80,000 (Rs.1,00,000-Rs.20,000). Even though the actual interest paid is Rs.35,000, the deduction is capped at 20% of the dividend received.

Taxation of capital gains

Gains from the sale of listed shares are taxed under the head ‘Capital gains’. For computing such gains, capital assets such as shares and equity mutual funds are categorised as either short-term or long-term, depending on the holding period before transfer.

Shares of XYZ

Shares listed on the recognised stock exchanges in India are treated as short-term capital assets if they are held for not more than 12 months preceding the date of transfer. In other cases, they are treated as longterm capital assets.

Long-term capital gains (LTCG): When equity shares are held for more than 12 months and then sold, the gains are classified as LTCG. Under current rules, any LTCG exceeding Rs.1.25 lakh is taxable at 12.5%, if the Securities Transaction Tax (STT) has been paid both at the time of acquisition and at the time of sale. STT is a levy imposed on the purchase and sale of stocks, mutual funds, and derivatives traded on Indian stock exchanges.

If, for example, on 1 October 2024, an investor purchases 1,000 shares of ABC through a recognised stock exchange at Rs.1,500 per share, that makes the total cost of acquisition Rs.15 lakh. On 1 November 2025, the shares are sold at Rs.2,000 per share, generating a sale consideration of Rs.20 lakh. The holding period exceeds 12 months, so the profit of Rs.5 lakh qualifies as LTCG. Out of this, `1.25 lakh is exempt. The remaining Rs.3.75 lakh is taxable at 12.5%, which is Rs.46,875.

Short-term capital gains (STCG): When shares are held for less than 12 months, the gains are classified as STCG. It is taxed at a concessional rate of 20% if the transaction is chargeable for STT paid both on the acquisition and the sale.

If 1,000 shares of ABC were sold on 1 March 2025 for Rs.1,700 per share, the gain of Rs.2 lakh (Rs.17 lakh minus Rs.15 lakh) will be STCG as the shares were held for less than 12 months. The tax will be 20% of Rs.2 lakh, that is Rs.40,000.

Capital gains and FIFO

Investors periodically acquire shares of a specific company at various times, guided by factors such as their income, available savings, and expectations of the firm’s future growth. Many choose systematic investment plans (SIPs) offered through mutual funds. When it comes to computing capital gains in these situations, the First-In, First-Out (FIFO) method is applied as a key principle.

Under the FIFO method, the securities credited first to a demat account are considered the first to be sold. As Harsh Bhuta, Managing Partner at Bhuta Shah & Co LLP, explains, “Indian tax regulations mandate that the cost of acquisition and the holding period for the dematerialised shares and mutual fund units be calculated on a FIFO basis. This approach promotes uniformity and prevents investors from selectively liquidating the most advantageous lots within a single account.”

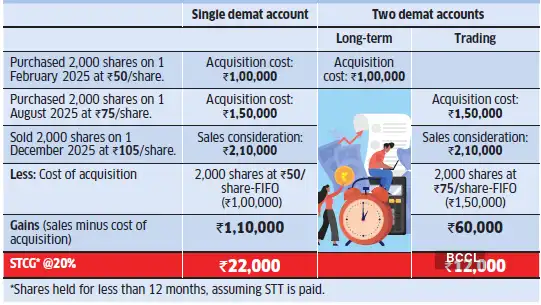

The taxability through FIFO is explained thus: an investor purchased shares of XYZ across different time periods (1 February and 1 August 2025) through a stock exchange and paid STT (see graphic). It is assumed that the shares are in a single demat account. On 1 December 2025, the investor sold 2,000 shares at Rs.105 per share. As the first 2,000 shares were acquired at Rs.50 per share on 1 February 2025, therefore, the cost of acquisition of Rs.50 per share will be considered for the computation of capital gains. In other words, shares that entered first will be considered exiting first, or FIFO.

STCG will be applicable as the shares were held for less than 12 months. The tax payable will be 20% of Rs.1.1 lakh, which is Rs.22,000.

Keep two demat accounts

Maintaining two separate demat accounts — one dedicated to long-term investments and another for trading — can help optimise tax liabilities. “Investors can hold multiple demat accounts with the same broker /depository participant and each account will have the FIFO methodology applied to it,” says Vivek Rajaraman, Managing Director, Head of Domestic Investment Advisory, Waterfield Advisors.

When transactions are routed through a single demat account, investors may unintentionally liquidate their low-cost, long-term holdings, thereby incurring higher STCG tax. By contrast, using multiple accounts allows for more efficient tax management. As Mihir Tanna, Associate Director at S K Patodia & Associates LLP, explains, the FIFO principle is applied on an account-by-account basis. This means that when securities are sold from one account, only the holdings in that specific account are considered, while securities in other accounts remain unaffected.

In the hypothetical example of XYZ, if the second lot of 2,000 shares were acquired through a separate demat account, the sale of those 2,000 shares would have resulted in a STCG tax of Rs.12,000 (20% of Rs.60,000) . By contrast, executing the same transaction through a single demat account would have led to a higher STCG tax liability of Rs.22,000.

Legitimate strategy

Maintaining multiple demat accounts is a fully legitimate practice, explicitly recognised by regulators and the tax administration. There is no loophole involved because the ultimate tax liability is determined at the PAN level, and all trades across all accounts must be disclosed in the return.

Bhuta says that when used correctly, the structure offers clarity between long-term investments and short-term or speculative trading and avoidance of unintended liquidation of long-term positions due to FIFO.