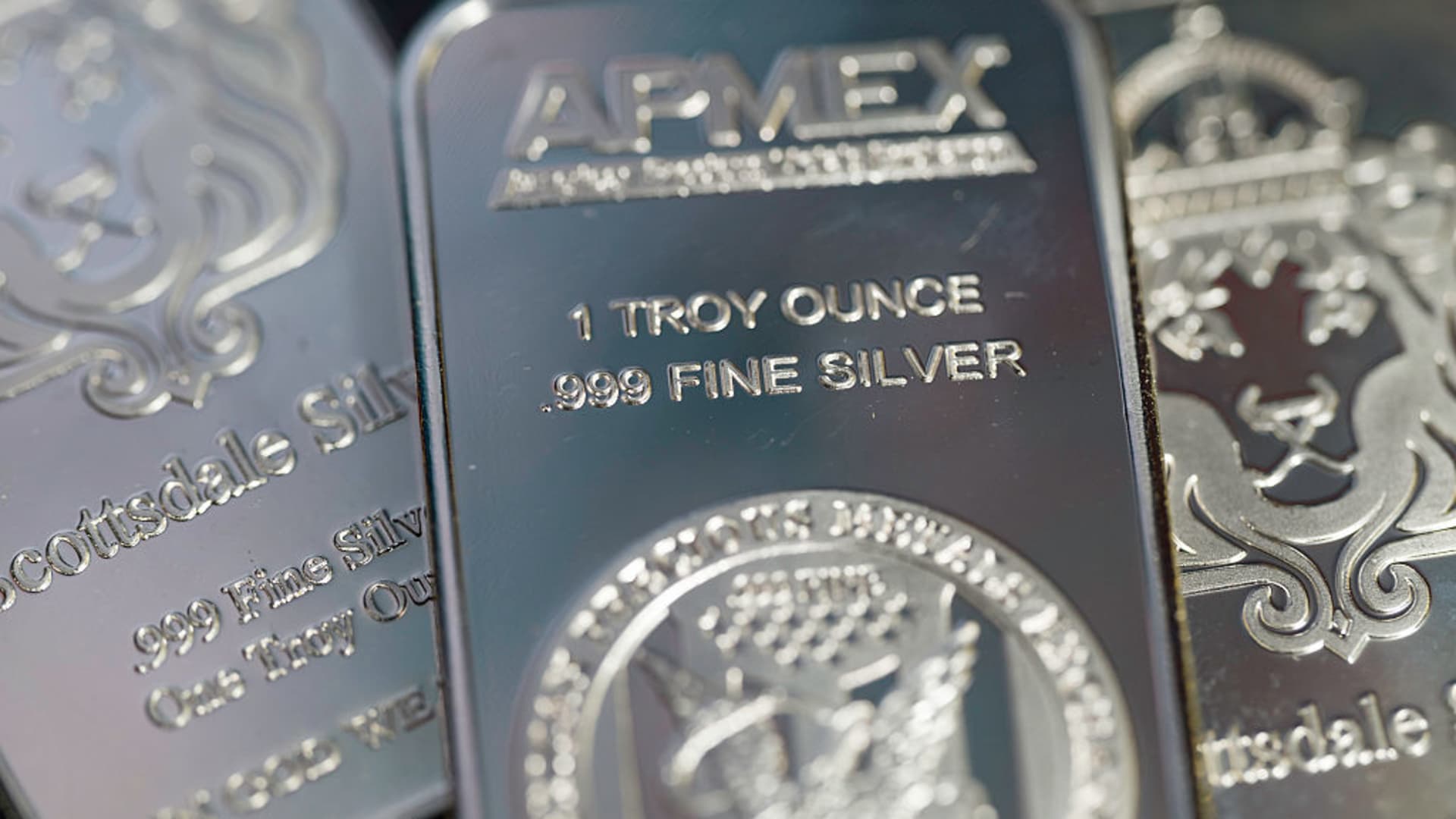

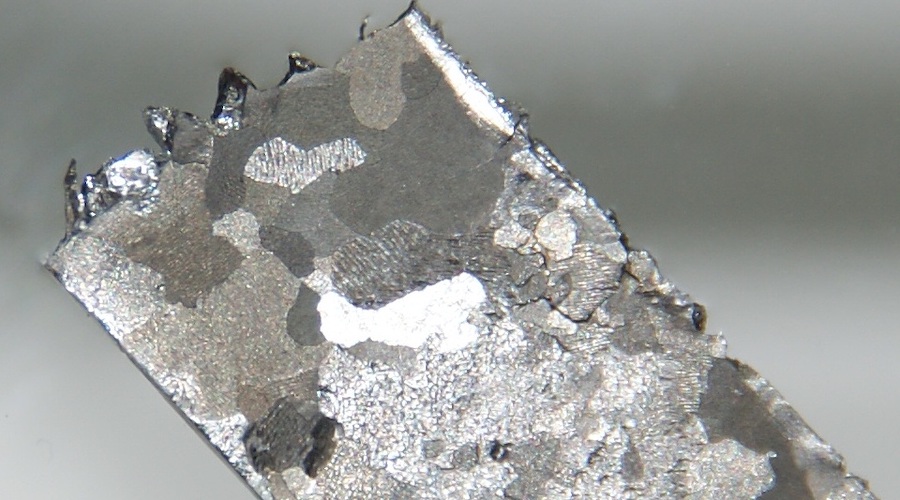

Australian shares are poised to open sharply higher after a three-day break, bolstered by surging precious metals prices. Gold briefly broke through $US5100 an ounce for the first time, while silver topped $US114 an ounce.

Goldman Sachs said “risk appetite is now very elevated”. At midday, the S&P 500 was within 30 points of resetting its record high with communication services and information technology pacing gains.

The Dow Jones was being led higher by Cisco, Apple and Microsoft. Microsoft will report quarterly results on Thursday AEDT, with Apple on Friday AEDT. Wedbush Securities Dan Ives said he’s expecting Wall Street analysts continue “to way underestimate” Microsoft’s cloud computing platform, Azure.

“Silver’s price action is nothing less than historic,” TD Securities’ commodities strategists said in a note. “The surge in investment demand, mostly led by retail, but clearly amplified by levered speculators, is overwhelming all other forces. This dynamic has persisted for longer than anticipated, potentially attracting even more inflows amid parabolic trading, and resulting in historic price action and extreme momentum.”

In an update of its commodity price forecasts, TD said it sees transitory trading highs of $US5400/oz for gold in the first half of 2026, $US118/oz for silver, $US3000/oz for platinum, $US2250/oz for palladium, nearly $US15,000 for copper. US crude is expected to peak at just over $US65 a barrel in the latter part of the year, while NYMEX natural gas could continue surging amid winter weather, it also said.

Market highlights

ASX 200 futures are pointing up 67 points or 0.8 per cent to 8895.

All US prices near 12.15pm New York time.

- AUD +0.6% to US69.35¢

- Bitcoin -0.7% to $US87,127

- On Wall St: Dow +0.4% S&P +0.6% Nasdaq +0.7%

- VIX -0.14 to 15.95

- Gold +2.1% to $US5094.26 an ounce

- Brent oil -0.3% to $US65.73 a barrel

- Iron ore -1% to $US103.55 a tonne

- 10-year yield: US 4.21% Australia 4.81%

Today’s agenda

NAB will release its December business confidence and conditions reports at 11.30am. The US Conference Board will release its January consumer confidence report at 2am AEDT on Wednesday.

Deutsche Bank Research’s view on results this week: “An important week is ahead featuring results from four Magnificent 7 stocks – Microsoft, Meta and Tesla on Wednesday (Thursday AEDT) and Apple on Thursday. The four make up 16 per cent of the S&P 500 by market cap, with the overall list of firms reporting next week totalling 32 per cent of aggregate capitalisation.

“Other tech highlights include ASML, Samsung, IBM and SAP. The focus will also be on defence firms RTX, Northrop Grumman and Lockheed Martin. On Friday, big oil firms Exxon and Chevron will also report. In Europe, highlights also include LVMH, Roche and Sanofi.

Top stories

Labor to fast-track data centre approvals amid OECD warning | While the government is pushing for more data centres, the OECD said the cloud computing boom meant Canberra would need to make additional efforts to meet its 2050 net zero carbon emissions target.

ASIC’s Longo warns big failures inevitable in ‘permissive’ market | In an interview months before he steps down, the country’s top corporate regulator says it should be harder for investors to put money into complex products.

Cost of gun buyback could exceed $1 billion | The number of firearms in Australia has climbed since 1996, raising questions about how much the Albanese government will spend on its new gun laws.