For 50 years, defined benefit pension plans in the U.S. have been dying a slow death — and along with it, many workers’ dreams of adequate guaranteed retirement income for life.

The good news is that, for the first time in decades, due to the passage of the SECURE Act, institutions have the product solutions in place to bring back that dream for more Americans.

How we got here

The Employee Retirement Income Security Act of 1974, better known as ERISA, was designed to safeguard America’s retirement system. But ERISA’s biggest legacy may be incentivizing companies to abandon their defined benefit plans — also known as pensions — in favor of defined contribution plans such as 401(k)s, which were established in 1978.

As a result, today’s private-sector workers are largely on their own when it comes to figuring out how much to save each year and how much they can spend in retirement. These are complicated decisions, and the average person may be ill-equipped to make them. The TIAA Institute’s surveys of Americans’ knowledge about financial matters show that only a third of people have basic comprehension of financial risk or appreciate that once they hit retirement age, they’ll likely need money for another two full decades or more.

This lack of financial know-how is a vulnerability that is heightened in a DC system that relies on a do-it-yourself approach. As traditional DB pension plans disappear, personal savings through DC plans take on more importance as a supplement to governmental programs, mainly Social Security. Even if workers become diligent savers, DC plans still can’t solve the puzzle of how much income they will need and how much money they can spend postretirement. LIMRA reports that 9 in 10 DC plans have no option for generating guaranteed lifetime income for retiring workers.

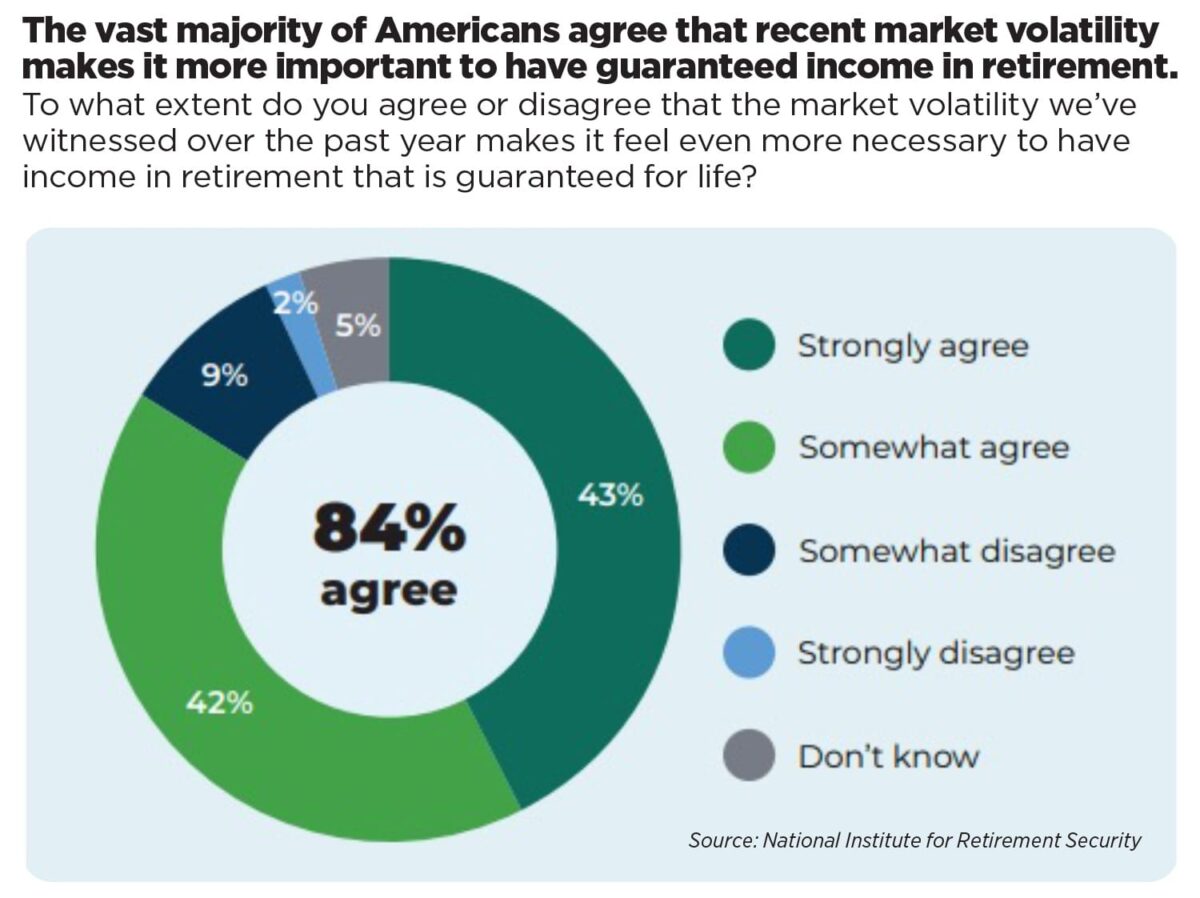

Is it any wonder then that AARP found 61% of Americans aged 50 or older are stressed about their retirement savings? Or that the National Institute on Retirement Security found three-quarters of that age group would welcome a return to bygone days when most private-sector workers still had pensions? A lifetime income stream from an annuity can restore this lost peace of mind — especially for our oldest retirees. As more people live into their 90s, they are more likely to grapple with cognitive decline. They become more prone to financial mistakes and thus more likely to benefit from a set-it-and-forget-it income strategy.

A ‘new’ old approach

Millions of TIAA retirement plan participants, most of whom built careers in service of others — plan their lives around dependable annuity income. For others, fixed annuities are a retirement solution hiding in plain sight. One reason is that annuities are relatively new to 401(k)s. Another may be that people don’t understand that annuities can provide the lifetime income they’re looking for.

Annuities can offer more income — not just income for life

TIAA has analyzed how blending annuity income with systematic withdrawals can impact retirement income. According to the company’s internal metric, the Annuity Payout Advantage, a 67-year-old retiree who annuitizes one-third of their savings with a fixed annuity in 2025 and withdraws 4% annually from the remaining balance could see 33% more income in their first year of retirement than someone who follows the 4% rule alone. For someone with $1 million in savings, that translates to about $1,100 more per month — or more than $13,000 per year ($53,154 compared with $40,000).

Our metric shows that in every month over the past 30 years, income provided from blending a fixed annuity with systematic withdrawals has given retirees more to spend in their first year than had they relied on conventional systematic withdrawals alone — between 16% and 44% more, depending on the prevailing payout rate.

Although these figures reflect outcomes specific to TIAA’s offerings, the broader insight remains: Annuitizing a portion of retirement savings may enhance income in retirement. For many, this kind of hybrid approach can offer more predictable spending power alongside long-term peace of mind.

Those are real dollars — real meals clients wouldn’t have eaten, real tickets clients wouldn’t have purchased, real trips clients might not have taken.

We can’t bring back the private pension. But for many Americans, converting a portion of their savings into annuity income is a sensible alternative to only pulling money out of savings. Importantly, sponsors of retirement plans are now able to offer their employees target date glidepaths that include a fixed retirement annuity that can be turned into lifetime income at retirement. And these products can be used as the all-important qualified default investment option, which most employees use to make their contributions.

In conjunction with Social Security and other savings, annuity income can be the difference between a frugal retirement marked by financial stress or one that provides our retired workers with the happiness and dignity they deserve.