The past week epitomises the kaleidoscopic state of the global economy in 2025. It began with renewed fears of trade tensions between the US and China. Then, on Tuesday, light relief came from the IMF, which raised its growth estimates for most major advanced economies in 2025. In financial markets, solid US bank earnings reports highlighted booming conditions for dealmaking and trading. The financiers’ updates were, however, tempered by warnings of a potential investor bubble in artificial intelligence, loose lending standards and unrealistically tight spreads in credit markets. By Friday, global equity markets were selling off once again, this time over concerns about the health of regional US lenders.

Anyone searching for a simple, overarching narrative to net out all the contradictions will be disappointed. And, if they find one, they ought to be sceptical. Forecasting is hard enough in periods of stability, let alone when the leader of the world’s largest economy wields unpredictability as a policy tool and when faith in the transformative power of a new technology drives trillions of dollars of investment. In such times, it is perhaps best to accept ambiguity and view the global economy and markets as they truly are — resilient, lucky and fragile all at once.

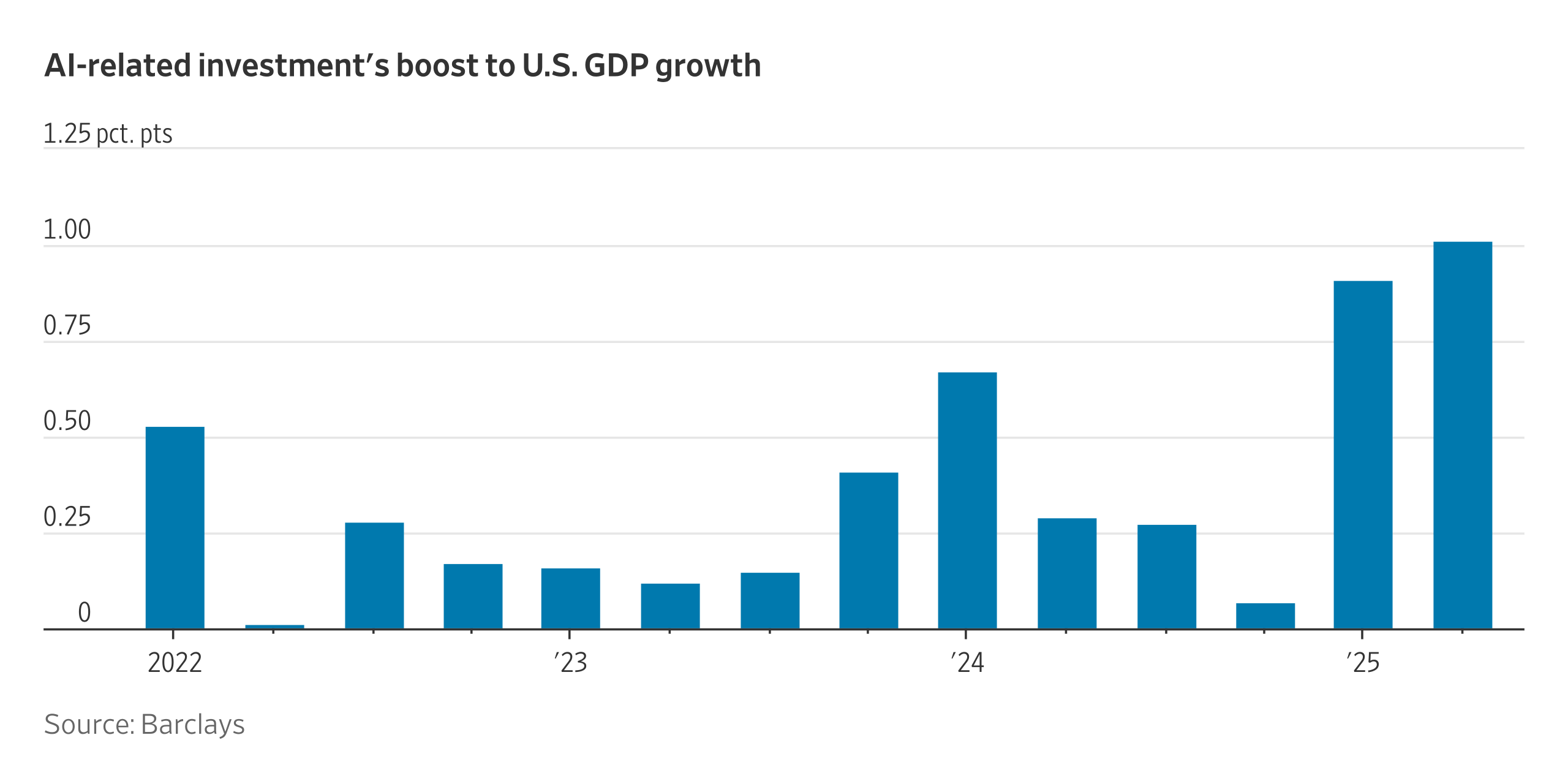

Beginning with the strengths, gloomy forecasts earlier this year underestimated the agility of the private sector. In response to US President Donald Trump’s import duties, American firms have frontloaded imports, absorbed costs and found workarounds, including sourcing from less tariffed suppliers. Foreign companies have rewired supply chains, and some have even resorted to relabelling products to skirt duties. At the same time, the promise of AI has propped up trade, capital expenditure and stock markets. Indeed, investment in data centres, chips and cloud infrastructure has offset a broad weakening in the US economy.

Policymakers have played a role. In some advanced economies, turmoil has sparked momentum on reforms. Canada is liberalising its internal market. The usually frugal Germany has raised its fiscal firepower. Developing economies have demonstrated stability — this week the IMF lauded their prudent monetary and exchange rate policies. Beyond the US, the logic of open trade also appears intact. Countries and blocs are diversifying their trade relations.

Perhaps there was also luck involved. The worst-case scenarios that kept economists and investors awake in the spring have not come to pass. Trump’s protectionist agenda has been diluted by delays, carve-outs and negotiations with trade partners. This means the US average effective tariff rate is now around 17.9 per cent, and not the 28 per cent estimated following the April 2 “liberation day” announcements. Interest rate cuts have provided some reprieve too, while weakness in the dollar, unusual in times of high uncertainty, has been a tailwind for emerging economies.

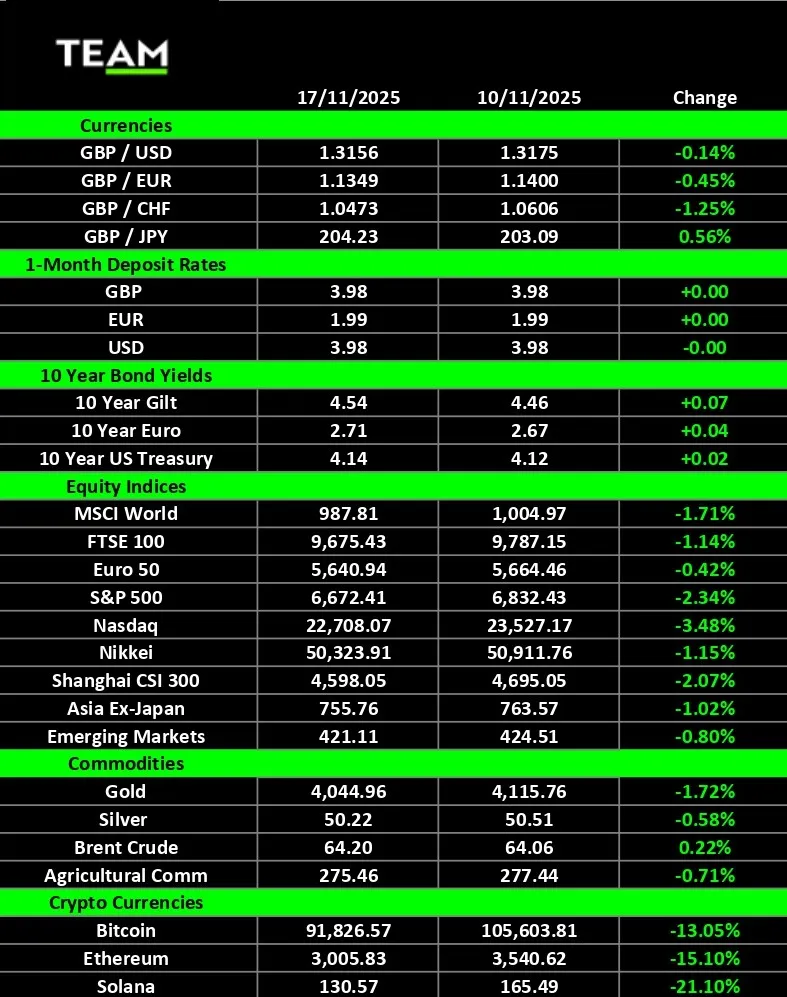

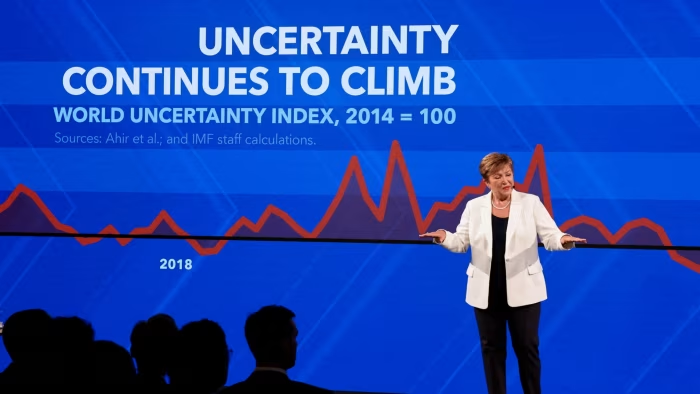

Good fortune, however, only underscores the perils ahead. US tariff rates, particularly with China, remain in flux. Existing duties rates and ongoing uncertainty will sap economic activity. Expensive stock valuations and high exposures to Big Tech risk a significant wipeout of wealth if AI optimism falters. The US would lose an economic crutch too. Elsewhere in financial markets, there is rising anxiety around the potential for defaults amid complacently priced corporate debt and leverage in private markets. For governments, shaky public finances leave little space for any fiscal support and add volatility to bond markets.

The full spectrum of economic signals reveals important lessons for policymakers and investors. Resilience needs to be built upon, luck and hope cannot be relied on, and fragility should not go unheeded. In a world that refuses to sit still, simplistic answers can obscure. Embracing the noise, rather than trying to filter it, is the surest bet.