The Economic Survey 2026, released on Thursday, flags a growing vulnerability in the global economic system amid rising geopolitical risks and economic turmoil.

While global growth and trade have held up better than expected so far, the annual survey, presented ahead of the Union budget, cautions that resilience may be deceptive, with negative effects expected to play out with a lag.

The survey warns of three possible scenarios in the financial markets, including a low-probability crisis that could lead to macroeconomic outcomes worse than those of the 2008 global financial crisis (GFC).

It noted that geopolitical competition has intensified, the security environment in Europe has become increasingly complex, financial vulnerabilities associated with leveraged technology investments are looming, and trade policies are being driven by political considerations rather than efficiency.

It warns that these developments suggest a world that is less coordinated, more risk-averse and exposed to a narrower safety margin.

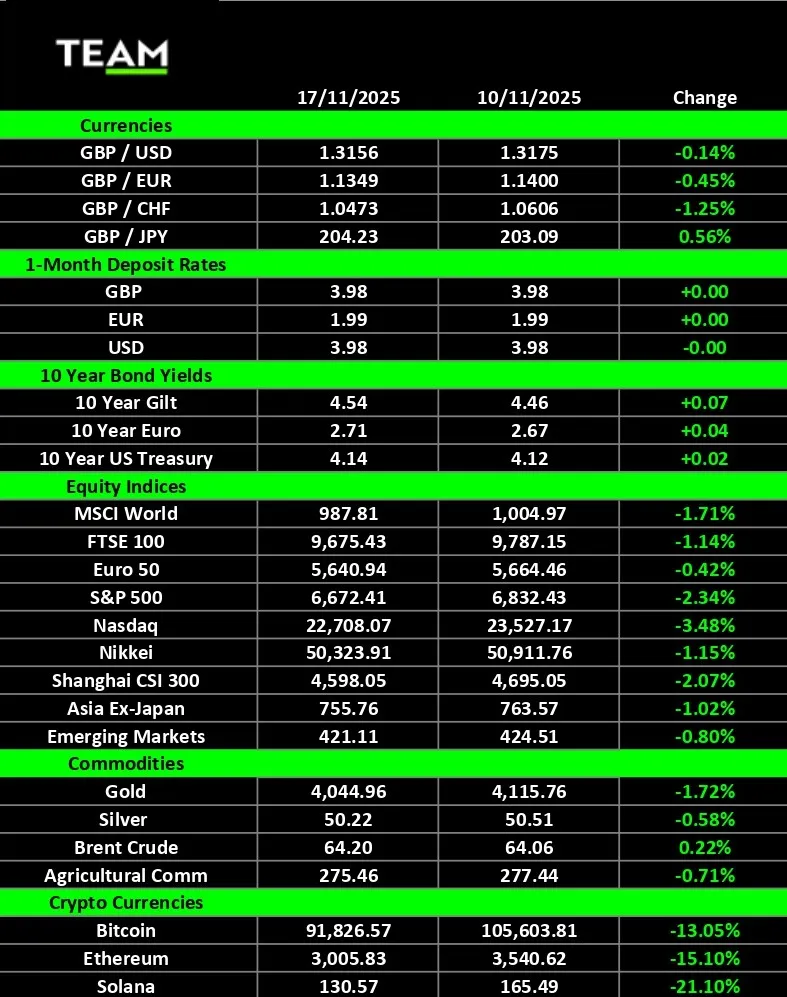

Financial markets appear to be pricing in this fragility. A sharp rise in gold prices from $2,607 to $4,315 per ounce in 2025 reflects a weakening US dollar, expectations of persistently negative real interest rates, and rising concerns over geopolitical and financial tail risks.

This rally in gold prices has extended into 2026 as well, with the yellow metal up 30% at $5,600 in the international markets.

The Global Economic Policy Uncertainty Index is also hovering near its worst levels since 2020, underscoring persistent investor anxiety.

Three scenarios for global financial markets

The survey outlined three broad global scenarios for 2026. The “best-case scenario”, assigned a probability of 40-45%, forecasts 2025-like economic conditions, with a thinner margin of safety and minor shocks escalating into larger reverberations.

In this scenario of “managed disorder”, financial stress episodes, trade frictions, and geopolitical tensions do not lead to systemic collapse but create volatility and require governments to intervene more actively to stabilize expectations.

A second scenario, also carrying a 40-45% probability, involves a disorderly multipolar breakdown, which cannot be treated as a tail risk. According to the Economic Survey 2025-26, under this outcome, geopolitical rivalries could intensify, the Russia-Ukraine conflict remains unresolved in a destabiliszing form, and global trade becomes increasingly coercive, wherein sanctions and measures proliferate, supply chains are realigned under political pressure, and financial stress events are transmitted across borders with fewer buffers and weaker institutional shock absorbers.

In this world, policies are expected to be more nationalized, and countries are expected to see sharper trade-offs between autonomy, growth, and stability.

Most concerning, however, is a third, lower-probability scenario, estimated at 10-20%, that the Economic Survey 2025-26 warns could have consequences worse than the 2008 GFC.

This scenario involves a systemic shock cascade in which financial, technological, and geopolitical stresses amplify one another rather than unfolding independently, the survey stated.

Central to this risk is the rapid build-up of leverage in technology and artificial intelligence (AI) investments. The survey noted that highly leveraged AI infrastructure investments rely on optimistic execution timelines, narrower customer concentration, and long-duration capital commitments.

The survey warned that a correction in this segment could tighten global financial conditions, trigger widespread risk aversion, and spill over into broader credit and capital markets.

If AI and tech correction coincide with geopolitical escalation or trade disruption, the resulting interaction could produce a sharper contraction in liquidity, a sudden weakening of capital flows, and a shift towards defensive economic responses across regions, it stated.

Warning signs are already emerging, including concerns over off-balance-sheet financing of data centres and rising government bond yields in key markets such as Japan.

What could probably make this risk potentially more damaging than 2008 is the lack of global coordination. Unlike during the GFC, when policy responses were swift and relatively unified, today’s world is more fragmented and distrustful.

How will it impact India?

However, the Economic Survey 2025-26 believes that in all three scenarios, India is relatively better off than most other countries. Its strong macroeconomic fundamentals, large domestic market, a less financialized growth model, and strong foreign exchange reserves provide it with a buffer. However, it does not mean India’s markets are entirely insulated from global shocks.

All these three scenarios pose a common risk for India—disruption of capital flows and its impact on the rupee—just with a variation in degree and duration likely. Indian markets are grappling with persistent selling by foreign investors.

According to National Securities Depository Ltd (NSDL) data, foreign portfolio investors (FPIs) have net sold Indian stocks worth ₹41,280 crore this year as of 28 January, the highest in the last 12 months.

This has pushed the Indian rupee almost 6% lower in a year, with the domestic unit breaching the 92 level against the US dollar earlier today.

“The appropriate stance for 2026 is therefore one of strategic sobriety rather than defensive pessimism. The external environment will require India to prioritise both domestic growth maximisation and shock absorption, with a greater emphasis on buffers, redundancy, and liquidity,” the Survey stated.

Disclaimer: This story is for educational purposes only. We advise investors to consult with certified experts before making any investment decisions.