Gilt yields have fallen as a result of the early release of the Office for Budget Responsibility’s (OBRs) fiscal forecasts.

The organisation now expects the UK economy to grow by 1.4 per cent next year, compared with the previous estimate of 1.9 per cent.

But a higher tax take means total borrowing as a percentage of GDP falls from 4.5 per cent of GDP this year to 1.9 per cent by 2029/30, which is the last financial year covered by this set of forecasts.

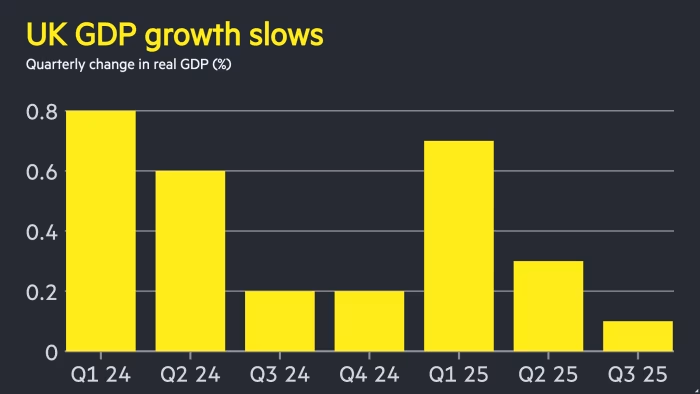

The OBR expects GDP growth to average 1.5 per cent each year from next year to 2029/30, which is 0.3 per cent per year lower than previously forecast.

Growth for this year has been revised sharply upwards, to 1.5 per cent, from the previous 1 per cent expected.

The combination of those measures has led to gilt yields falling, yields falling mean the price is rising.

Gilt prices are influenced by three factors: the inflation outlook, the level of new gilt issuance and the growth outlook.

If growth is 0.5 per cent weaker next year than had been forecast, the expectation is this would reduce the level of demand in the economy, which would in normal circumstances reduce the level of inflation.

Lower inflation is typical viewed as positive for gilts as it increases the spending power of the income investors receive.

In terms of the issuance of new gilts, the tax increases announced in the Budget, which amount to £26bn in total, mean the chancellor is expected to meet her fiscal rules in 2029/30 with a margin of safety of £22bn.

The OBR report stated they believe this is within the long-term average level of margin of error as set out in previous budgets and by previous chancellors.

The margin of error being sufficiently large may mean that gilt issuance can stay within the present parameters, reducing market fears about a torrent of new issuance in future.

In terms of the growth rate this year, and the reason for it being revised upwards, the OBR report stated: “This is because output growth was revised up in the second half of 2024 and growth was stronger than expected in the first quarter of 2025, at 0.7 per cent.

“The latter was partly due to the temporary frontloading of property transactions and exports, as households sought to avoid stamp duty threshold changes and businesses tried to get ahead of tariff increases, both of which came in from April.

“Growth then fell to 0.3 per cent in the second quarter, as these temporary factors unwound, and to 0.1 per cent in the third quarter, when the Jaguar Land Rover shutdown temporarily weighed on growth both below our March forecast.

“We expect quarterly growth to pick up only gradually in the near term as geopolitical uncertainty persists and domestic business and consumer confidence remains subdued, including in anticipation of further tax rises.”

The primary reason given for the 0.3 per cent downgrade to future growth forecasts is the reduction in the OBR’s estimate for productivity growth.

The organisation stated that it had previously expected productivity growth to rebound after several negative years in the wake of the pandemic, but this has not happened.

The OBR now expects inflation for the whole of 2025 to be 3.5 per cent, which is 0.2 per cent higher than it forecast in March, and for inflation to be 2.5 per cent next year, around 0.4 per cent higher than previously forecast.

Grant Slade, UK economist at Morningstar said: “Hikes to the headline income tax rates would have been a preferred outcome for gilt markets since they are frontloaded and signalled a more aggressive approach to debt consolidation.”

david.thorpe@ft.com