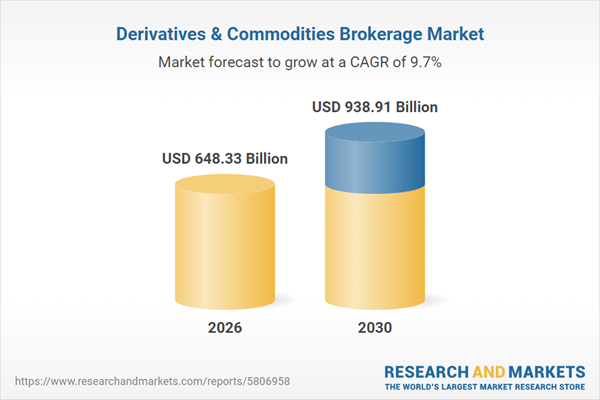

In finance, the obvious is often misleading. Headlines chase the latest macro story or inflation narratives, but real markets are shaped by liquidity, funding costs, and the behavior of those who actually move money. In this regard, 2026 will unlikely be a repeat of 2025 or a mere extension of ongoing bullish sentiment. I expect us to finally reach a structural inflection point defined by liquidity rebalancing, regulatory evolution, and the maturation of institutional multi‑asset trading.

This analysis unpacks the true undercurrents shaping FX and CFD markets over the next year. It looks beyond surface-level narratives to examine how funding costs and volatility are altering liquidity conditions, why CFD markets are gradually moving toward higher execution standards and greater transparency, how retail and institutional trading behaviour continues to diverge, and where risk and opportunity are most likely to concentrate in 2026. When it comes to general expectations, these dynamics matter far more than short-term macro headlines.

FX Markets in 2026: Liquidity Structure, Funding Costs, and Hedging Demand

The Size and Shape of Global FX Activity

The scale of foreign exchange trading is anything but a technical footnote. At the end of the day, it reflects the underlying pulse of global financial activity. The latest BIS Triennial Central Bank Survey on FX and OTC markets shows that average daily FX turnover has now climbed beyond $9.5 trillion, representing an increase of roughly 27–28% compared with 2022. This expansion is not merely cyclical; it points to a deeper structural liquidity sourcing transition, and how it is being distributed and consumed across markets. In this respect, spot FX and outright forwards have been the primary drivers of this expansion, rising materially relative to previous cycles, while traditional FX swaps — long the backbone of cross‑currency funding trades — grew more modestly.

Put differently, FX markets are bigger, more active, and structurally more diverse than a mere glance at the interbank space might suggest. The proliferation of trading between global dealers and “other financial institutions” — including asset managers, hedge funds, and non‑reporting banks — illustrates how institutional hedging behavior is no longer an alternative narrative but the core of survival.

This trend sets the stage for 2026 in two crucial ways:

- First of all, as I said, liquidity is expanding, but it is less and less evenly distributed. Sterling’s share has declined, while the Chinese renminbi and Swiss franc have made steady inroads. The remains dominant, but not to the exclusion of regional centres.

- Meanwhile, dealer internalization is rising. Faced with elevated volatility and cost of hedging, major liquidity providers increasingly match client flows internally rather than stepping into external markets — a behavior that compresses observable bid‑offer spreads but can also elevate systemic sensitivity to internal risk models.

At its core, the FX market has moved well beyond its pre-pandemic operating model. When it comes to pricing and liquidity formation, stronger hedging demand, persistently higher volatility premia, and increasingly segmented liquidity pools are defining a new market environment — one that will continue to influence funding costs and trading behaviour well into 2026.

Volatility Regimes and Funding Costs

Although liquidity is king, volatility remains the main driver of trading conditions. Data from the CME Group’s FX Volatility Index show that implied volatilities across both G10 and emerging-market currencies materially increased compared with the past decade, especially when accounting for macro risks and cross-asset correlations. Higher volatility feeds directly into increased hedging costs, which in turn shape how institutional clients approach the market.

For corporate treasurers and asset managers alike, this means a recalibration of hedging strategies: simple forward hedges give way to option overlays and structured approaches that balance cost efficiency against tail risk. Where hedging is expensive, institutions demand more granular pricing and deeper liquidity, placing pressure on brokers and LPs to offer multi‑venue access and tighter spreads.

CFD Markets: Towards Transparency, Execution Quality, and Institutional‑Grade Systems

Regulatory Imperatives and Market Evolution

Contracts for Difference (CFDs) have long endured scrutiny from regulators, particularly those focused on investor protection. The European Securities and Markets Authority’s (ESMA) product intervention measures, for instance, have restricted leverage for retail CFDs and imposed standardized risk warnings and negative balance protections. Meanwhile, the UK’s Financial Conduct Authority (FCA) has conducted multi‑firm reviews highlighting poor transparency in fee structures and unjustified overnight funding charges among CFD providers — going so far as to warn firms that fail to deliver fair value to consumers.

Indeed, in late 2025, the FCA explicitly reaffirmed its intent to take enforcement action where CFD providers fail to meet Consumer Duty standards, especially with respect to retail clients. This regulatory pressure, while painful for certain legacy providers, is inducing a tectonic shift: the CFD ecosystem is beginning to orient towards greater execution quality, clearer pricing, and more robust infrastructure.

That said, this evolution is neither linear nor uniform across jurisdictions. The legacy of product intervention measures persists in some regions, while other regulators are exploring more nuanced frameworks that encourage innovation (for example, in digital assets) without sacrificing investor protection. These dynamics will heighten segmentation in CFD offerings: truly institutional grade platforms versus riskier retail‑oriented venues.

Execution Quality as a Differentiator

At the core of CFD market maturation in 2026 is execution quality. Where once execution quality was loosely defined — as long as price feeds did not blatantly lag underlying markets — now institutional clients demand measurable performance metrics, quantifiable slippage protection, and instantly verifiable fill quality across venues.

This evolution stems from simple logic: price quality matters when spreads are thin, and volatility is high. In illiquid conditions, poor execution can meaningfully alter P&L; in contrast, high‑quality execution, particularly in major FX pairs and multi‑asset CFDs, can be a competitive differentiator among brokers who accommodate institutional flows.

Brokers that invest in technology bridging disparate liquidity pools — whether it is bilateral OTC pools, central limit order books, or smart order routers — will be the ultimate winners.

Retail Versus Institutional: Diverging Behaviours and Structural Consequences

Positioning, Leverage, and Risk Appetite

Markets in 2026 will be defined not by a uniform, but vague “trader behaviour,” but rather by the juxtaposition of retail and institutional positioning trends. When it comes to retail traders, the broad patterns still look familiar. We contemplate episodic spikes in interest during and short-after selected macro or geopolitical events, followed by leverage‑induced frenzy on high‑beta instruments, and clustering around crowded trades. By contrast, institutional traders exhibit systematic hedging, tactical sensorium for volatility regimes, and a willingness to trade complex structured products.

Meanwhile, retail flows are often directionally biased and subject to herd behaviour, particularly in leveraged environments we still live in despite relatively high interest rates. Institutional flows, by contrast, are driven by balance‑sheet hedging, as well as asset allocation and risk premia shifts. The latter two are not always in sync, while retail positioning can even more amplify short‑term volatility. However, institutional positioning, as always, tends to dampen it over longer horizons.

Where this divergence converges into risk is leverage behavior. Excessive leverage at retail venues can create shallow liquidity pockets — particularly on under‑regulated platforms. Hence, in 2026, leverage risk will remain a central theme — not as a simplistic “too much debt” narrative, but as a variable contingent on instrument, counterparty, and regulatory backdrop.

CFTC Commitment of Traders Signals and Institutional Flows

In this respect, an increasingly acclaimed practice of positioning data — such as that published by the CFTC’s Commitment of Traders (COT) reports — offers glimpses into how institutional sentiment differs from retail narratives. While we do not have space here to dwell on specific weekly figures, the enduring insight is straightforward: large speculators and money managers often have longer time horizons and hedging motivations that diverge sharply from short‑term retail positioning.

Key Risk Themes for 2026

1. Leverage and Margin Fragility

Leverage will be scrutinized more intensely in 2026—not just the headline ratios offered to traders, but how leverage interacts with funding costs, market depth, and cross‑asset correlations. Excessive exposure in any segment — be it FX pairs or CFDs on equity indices—can create liquidity vacuums during stress episodes.

2. Regulatory Tightening and Fragmentation

Regulation is constantly evolving, a trend made especially evident today as new legislative initiatives emerge in response to the digitalization and decentralization of modern finance. ESMA, the FCA, and other authorities are adjusting their frameworks as I am writing this. They apparently focus on investor protection, transparent execution, and fair treatment in the markets. We should expect additional scrutiny on margin practices, as well as price execution, and leverage disclosures — especially as digital asset trading gets more and more integrated into traditional markets.

The industry’s infrastructure will be shaped by regulatory expectations, not the other way around. Brokers that anticipate these shifts by embedding compliance into their technology stacks will mitigate operational and reputational risk.

3. Operational Resilience and Infrastructure Integration

Operational resilience is no longer a back‑office concern; it is a front‑line determinant of competitive viability. Fragmented liquidity venues, inter‑dealer networks, and platform outages all introduce risks that can cascade. Brokers and liquidity providers must invest in redundancy, real‑time monitoring, and automated reconciliation to withstand shocks — and this will distinguish winners from laggards in 2026.

Where Opportunity Sits Next

Multi‑Asset and Institutional Adoption

Slowly but surely, institutional adoption of crypto and multi‑asset platforms is rising, supercharged by buoyancy of demand for integrated execution across asset classes amid vanishing single-market opportunities. Digital assets, once a fringe interest, are increasingly woven into institutional portfolios as risk overlays, hedging instruments, and non‑correlated assets.

That said, the crypto domain brings unique liquidity, alpha and regulatory dynamics requiring bespoke execution algorithms and deep counterparty analysis. I’m sure those brokers and platforms that can bridge traditional FX/CFD liquidity with digital asset markets while managing counterparty risk will find a unique opportunity.

Asia-Pacific and Regional Liquidity Hubs

While the U.K. and U.S. remain dominant FX centres, Asia‑Pacific jurisdictions — notably Singapore and Hong Kong—are gaining share. Regional liquidity pools are deepening, with local FX flows increasingly competitive on a global scale. This trend is not just anecdotal; it reflects a redistribution of market share, driven by institutional client demand for proximity and faster execution across time zones.

Product Innovation: Structured and Algorithmic Execution

Products that embed execution quality guarantees, smart order routing across liquidity layers, and structured hedging tools will gain traction. Retail‑oriented products that mimic institutional execution are emerging, but the true frontier lies in hybrid models that balance algorithmic execution with risk‑managed exposure.

Conclusion

As far as I can see at this point, 2026 is unlikely to become just another year of incremental change; it will be a year where structural liquidity dynamics and evolving institutional behaviours redefine how FX and CFD markets function. Funding costs will shape hedging strategies. Regulatory discipline will drive transparency and execution quality. And the divergence between retail and institutional behaviour will crystallize into distinct liquidity regimes.

All in all, what matters most is not the macro narrative du jour, but how markets actually clear, how liquidity is provisioned and accumulated over time, and how risk is priced across the board.