Market intelligence is key as energy traders focus on short-term trading amid uncertainty, writes Stella Farrington

It has been a dizzying few months across financial and commodities markets, as traders try to navigate an ever-changing policy landscape. A darkening macroeconomic picture is putting pressure on energy prices, while looming trade wars and geopolitical unrest threaten to send shockwaves through every commodity that moves over international borders – and many that do not.

All of this is injecting volatility and unpredictability into day-to-day trading, putting a premium on the role played by commodity brokers – vital intermediaries who do much more than simply access liquidity. In uncertain markets, a good broker will provide insights into wider market sentiment and offer advice and support that goes beyond matching a bid with an offer.

Over recent decades, ICAP has been a fixture within physical and derivative commodities markets. The company was named Commodity broker of the year in Energy Risk’s 2025 awards and, with its sister firm Tullett Prebon, took a raft of first and second placings across this year’s Energy Risk Commodity Rankings.

The two firms – ranked numbers 1 and 2, respectively, in the overall Commodities broker leaderboard – made particularly strong showings in the natural gas and power categories.

Energy Risk spoke to TP ICAP’s co-CEOs of energy and commodities, David Silbert and Joachim Emanuelsson, to uncover how the firm and its clients are approaching a rapidly changing marketplace.

How are your clients in the energy markets coping with current market conditions, and how is it changing how you are working with them?

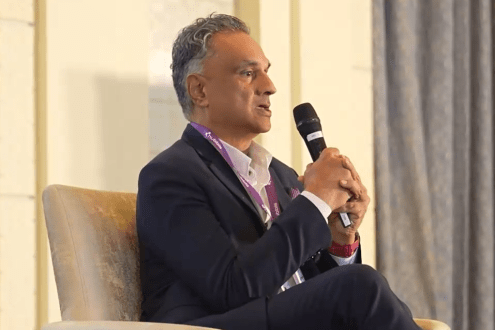

David Silbert, TP ICAP

David Silbert: The issues they are dealing with in gas and power are no different than we see across the commodities complex. We’ve gone from what are usually fundamentally driven markets to ones driven by headlines and vacillating policy. We’re seeing the same thing in oil, where the markets are choppy and deviating from the fundamentals. Our clients have gone from long-term, strategic decision-making to very short-term trading of volatility. They’ve had to adapt to a shorter-term trading horizon, and we’ve had to adapt to ensure they have the transparency and liquidity they need to trade these markets.

Has that changed your clients’ expectations, and the sort of service you need to provide as an energy broker?

David Silbert: The volatility has certainly been a factor, but it hasn’t been the sort of volatility that disrupts markets. We’re still seeing a lot of activity, and the markets are functioning very well; liquidity hasn’t dried up. People just have to change their time horizon a little bit, until things become more predictable.

Some traders are also finding that markets are more correlated than they assumed. Natural gas and, by extension, US power markets are not immune to wider fluctuations in equity and bond markets. The natural gas industry tends to assume its market is something of a closed system, particularly in the US, which reacts more to fundamentals and trade flows than to political headlines and macro factors.

But natural gas has a pretty high correlation with the S&P 500. That’s a result of flows of money. It’s risk-on and risk-off, which moves money in and out of commodities, including natural gas. If you’ve been in these markets a while, you know you need to have a macro view as well as a view on the fundamentals. If you’re fairly new to the market, you’ve probably just learned a valuable lesson.

Current policy-driven volatility notwithstanding, what is your fundamental view on the outlook in gas and power?

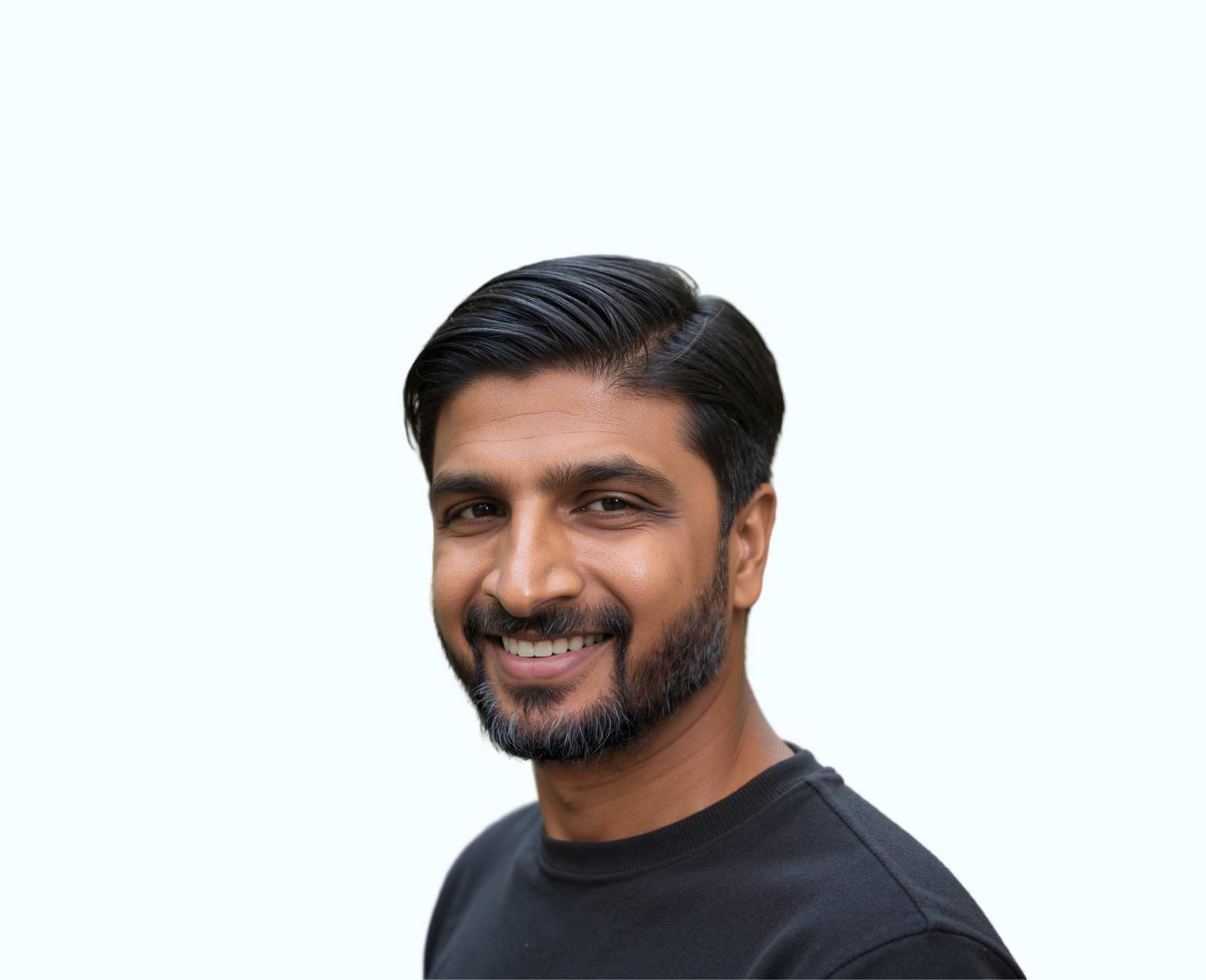

Joachim Emanuelsson, TP ICAP

Joachim Emanuelsson: In Europe, we are fundamentally very bullish on power, given what’s going on with the transition to a low-carbon economy. Not only is power fundamental to that, so too are the commodities that go into producing it: gas, steel, iron ore, copper, nickel, lithium, and so on. That whole complex is key to our power and gas business in Europe.

David Silbert: Obviously the US is in a different place to Europe, and we’re starting to see some states react to the change in the federal approach to climate. From a legislative standpoint, I think there is going to be a bit less appetite to force increasing carbon targets on corporates. It doesn’t mean we won’t see a lot of activity in the market, whether in renewable energy certificates or carbon, but it just won’t be through mandated requirements.

Frankly, if we go into an environment where renewable energy is less attractive from a regulatory or subsidy standpoint, that’s going to have an impact on increasing power prices at the back end of the curve. We’re going to have significant load growth in the US and, if that load is going to be supplied from natural gas or nuclear, it’s going to be more costly.

To what would you attribute your success in this year’s Energy Risk Commodity Rankings?

David Silbert: We’ve established ourselves in the US markets for quite a while. We have people who have been involved for 15 or 20 years. The other thing that differentiates us from some of our competitors is our options capabilities: as options markets developed, we were there helping develop them.

In options markets, there is more opportunity for a good broker to differentiate themselves. Rather than simply match the obvious trade, they might be able to identify a different trade that meets the client’s needs but with better volatility, better skew and better dynamics.

Joachim Emanuelsson: This is where a broker can add value to the relationship – by having an informed, intelligent discussion with the trader. Those are conversations we are well suited to have.

We’ve come off several years of growth, where all the trading houses have been making strong profits. But clients’ needs in commodities change with the cycle. What we do really well is make sure we’re listening and adjust our service to those needs.

ICAP took first place in weather derivatives. As a long-standing player in that market, how do you see it evolving?

Joachim Emanuelsson: A weather derivatives market has been around for a long time, but it had never really taken off. Over the past two years, that has begun to change. There are a couple of reasons for that.

First, the banks have effectively exited the market. They played a role in slowing its growth because they prevented brokers from getting involved and developing the customer base: they stood between potential buyers and sellers of weather derivatives – for example, a utility on one side and a shipowner on the other. That seems to have been upended, and we’re creating a market in which we are speaking to insurance companies and utilities and other users of weather derivatives.

Second, there are now many more measuring points for weather compared with 15 or 20 years ago. We now have the weather data and the computing power to structure more flexible contracts that accurately match the buyer’s weather exposure.

David Silbert: The other major development is the necessity of renewable energy developers to hedge their weather exposure to underpin their financing – that need to hedge wind or solar exposure is no longer a want, it’s a need. Those exposures were not easy to quantify or price until quite recently.

You note that technology has changed how the market can approach weather risk. How is this changing how you interact with your clients?

Joachim Emanuelsson: Having good technology that helps the broker do their job is key – whether that’s being able to collect all the data we need, having a strong order management system that allows our brokers to run global books, saving time with straight-through processing to exchanges, or providing our brokers with the basic analytics to price curves and instruments.

That’s something I think we’ve done a good job with, but that’s an ongoing effort. As soon as you’ve released a piece of code, it’s already old, and that’s especially true with how artificial intelligence is impacting the speed of development.

David Silbert: Technology is constantly evolving, but it’s not going to be the driver of profit and loss going forward. There was a time when information was scarce and it provided competitive advantage, certainly in commodities – the more you knew that other people didn’t, the better off you were in terms of making trading decisions and allocating capital.

Now, it’s the opposite situation. There is so much information, data and news that people are being bombarded. What we must figure out is: How do we help our clients focus on the data that is actually important? How can we refine it and funnel all that information in ways that give our clients some sort of edge? We haven’t solved that problem, but we’re listening to our clients and helping them think about that challenge.

Our added value lies in giving them information they don’t already have. What are we seeing in the market? What are the dynamics today? That sort of insight doesn’t show up in a trended dataset. We have a unique vantage point on what’s happening in the market, and that’s what people pay us for.